AVERAGE Brent crude oil for Jul calendar year 2025 (CY25) slipped -17% year-on-year (yoy) and -0.4% month-on-month (mom) to an average of USD69.55pb.

The decline was due to:

(i) Increased global supply by non-OPEC+ countries.

(ii) OPEC+ unwinding voluntary cuts.

(iii) Slow demand growth from economic slowdown, shift towards clean energy and lacklustre consumption in US and China.

(iv) Higher oil inventory builds.

This was offset by the ongoing geopolitical tensions, with the Iran-Israel conflict temporarily spiking oil prices. However, these are quickly reversed as underlying supply-demand fundamentals were reasserted.

The KL Energy Index index’s Jul CY25 close was lower by -21.5% yoy but gained +1.8% mom. The Department of Statistics Malaysia reported that PPI for the mining sector fell significantly due to lower prices for crude petroleum and natural gas.

This sustained downturn in producer prices likely had a cumulative negative effect on the profitability and market valuation of Malaysian energy companies.

The shift towards renewable energy and energy transition policies in Malaysia created a cautious investment environment for traditional fossil fuel companies.

“However, we noted that after dipping to a two-month low in early July CY25, the index experienced a technical rebound, giving its higher monthly close than June CY25,” said MBSB Research.

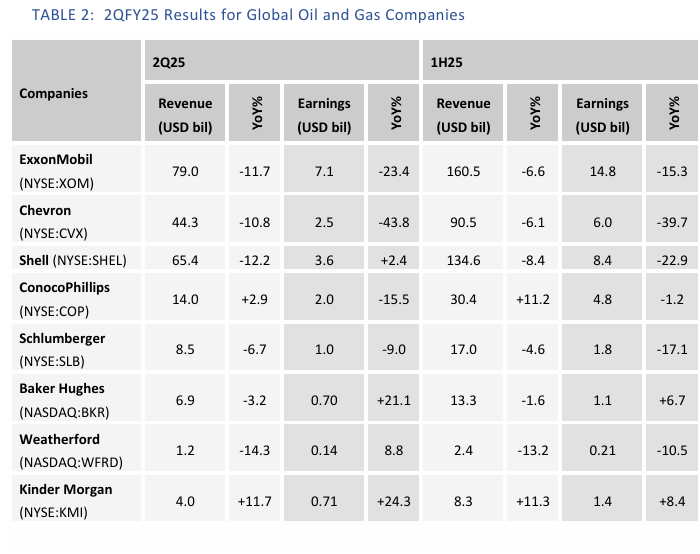

The first half of CY25 is challenging for most of the major players. Most had indicated lower revenue and net income, most notably for the integrated oil and gas companies.

ExxonMobil, Chevron and Shell saw substantial declines due to the lower oil prices and the slowdown in global economy that hampered demand for their services and products.

Meanwhile, OGSE companies which are tied closely to the upstream division, like Schlumberger, Baker Hughes and Weatherford, faced headwinds.

The drop in earnings was a direct consequence of lower upstream investment and capital discipline practiced within these OGSE companies.

All in all, we maintain our enutral stance on the sector. The Malaysian oil and gas sector is currently in a state of equilibrium. The negative factors—lower commodity prices, reduced capex, and a challenging services market—are largely counterbalanced by the positive factors—the resilience of the natural gas and LNG sector, stable midstream demand, and a strategic long-term outlook.

The sector is not expected to see a significant surge in earnings or valuations in the near term and is highly likely to be selective by divisions.

However, the sector also has strong foundational elements that prevent a major collapse, further ensuring that it will perform broadly in line with the wider market, with limited short-term catalysts, barring any events that would warrant a spike in oil and gas prices and further sustain the surge. —Aug 12, 2025

Main image: Future Bridge