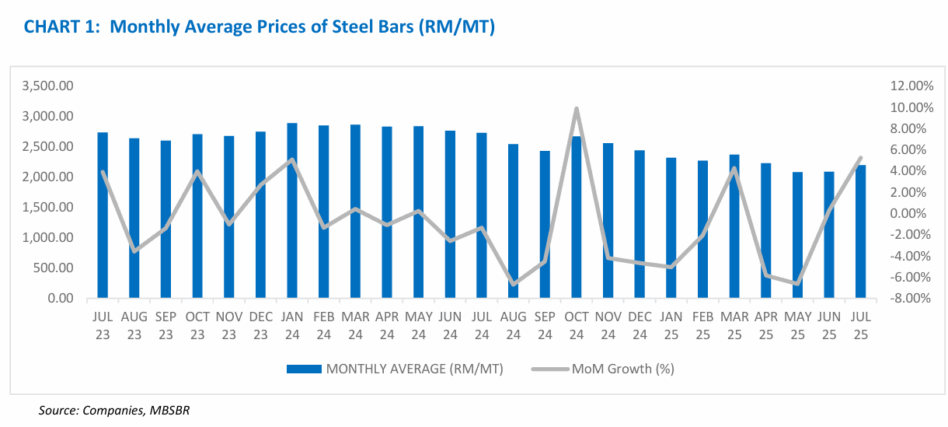

THE average prices of steel bars in Malaysia heightened for the second consecutive month as of Jul-25, following a brief softening of prices from Mar-May-25.

Average prices rose +5.26% month-on-month (mom) in Jul-25 to RM2,200.00 per metric tonne, the first consecutive month price incline since Jan-24.

“This was largely attributable to Malaysia’s imposition of provisional anti‑dumping duties, effective from 7 July 2025, on selected galvanized iron and steel imports from China, South Korea and Vietnam, ranging from 3.86% to 57.90%, which has begun to limit cheap inflows, tighten local supply and lift procurement costs,” said MBSB Research.

Rising input prices for coking coal and scrap, together with construction-related inflation and labour tightness in Malaysia, have also contributed to recent upward momentum.

As of Jul-25, the monthly average price for the binding substance has remained unchanged for the 24th consecutive month since Jul-23, holding steady at RM380 per metric tonne.

This prolonged price stability was attributed to a balanced supply-demand dynamic in the market and consistent raw material costs leading to easing cost pressures that help to sustain price.

Prices have remained consistent across all regions, including the northern, central, and eastern Peninsula, as well as Sabah and Sarawak.

The continued stability in cement pricing is mainly supported by relatively flat input costs, particularly for coal, petcoke, and clinker, which have remained relatively flat since late calendar year 2023 (CY23), reducing the pressure on producers to revise pricing.

Local producers have also benefited from optimised production scheduling and reduced reliance on spot imports, allowing for better margin control without needing to adjust selling prices.

We expect the price of bulk cement to remain relatively stable moving forward, backed by the consistent demand from key projects such as the reinstatement of five LRT stations, the MRT3, the Penang International Airport expansion, along with the sustained demand for industrial projects and property development.

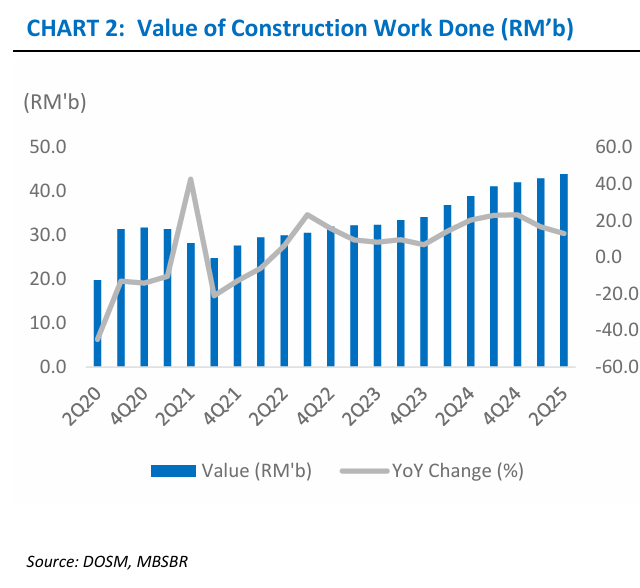

Data from the Department of Statistics Malaysia showed that for the thirteenth consecutive quarter, the construction sector remained on a positive trajectory, albeit growing at a slower pace compared to the first quarter.

Out of RM43.9 bil value of work done, 37.1% or equivalent to RM16.3 bil was in civil engineering, primarily in the construction of utility projects (RM8.1 bil) and construction of roads and railways (RM6.0 bil) activities.

We maintain our positive stance on the construction sector, backed by a combination of easing cost pressures, resilient private sector demand, and stronger public project execution.

Steel bar prices have continued to ease on a year-to-date (‑9.91%) and year-on-year (‑19.5%) basis despite recent monthly fluctuations, while cement prices remain stable due to disciplined domestic production and raw material cost control, ensuring a favourable cost environment for contractors.

These cost dynamics, paired with gradual easing of labour constraints and the ability to pass through SST and tariff-related costs, continue to support profitability in ongoing projects. Momentum is also improving on the demand side. —Aug 15, 2025

Main image: National Action Plan On Business And Human Rights