BUOYED by high crude palm oil (CPO) prices, merger and acquisitions (M&A) activities picked up momentum in 2025 with MYR2 bil value transacted thus far.

“We believe the M&A activities will be sustained into 2026, in part fueled by monetisation of prime estates by companies such as SDG, GENP and KLK,” said Maybank Investment Bank (MIB).

“In August 2025, we witnessed the privatisation and delisting of FGV,” it added.

This follows the successful privatisation of Boustead Plantations announced in 2023 which cost LTAT MYR1.1 bil. In comparison, FGV’s privatisation may cost FELDA up to MYR600 mil, and this lifted overall M&A deals in 2025 thus far to about MYR2.06 bil, nearly doubling the transacted values of 2024.

Thus far in 2025, 45% of the M&A values were transacted for property development related purposes. The most notable transaction was SDG’s 484ha MVV 2.0 land sales into an JV entity for MYR573 mil cash or MYR1,609,472/ha.

The transacted price is 33x the average physical transacted prices of estate land at MYR49,100/ha. Across the region, a notable transaction in March 2025 was First Resources acquisition of 91.2%-equity stake in PT Austindo Nusantara for USD330 mil (or MYR1,467 mil) cash.

ANJT owns 48,353 ha of own oil palm planted area. The motivation for M&A / privatisation include:

(1) Commitments to NDPE translating into increasing interests in brownfield land as greenfield opportunity is near non-existent.

(2) Unlocking value of some prime land amassed decades ago, and reinvesting some sales proceeds on cheaper agriland.

(3) Rising cost pressures and workers shortage will likely hasten industry consolidation as smaller planters may lack economies of scale.

(4) A general under-appreciation of the value of selected planters.

MIB observed huge valuation gaps between the transacted physical prices and the equity values of selected small and medium capitalisation (SMID caps).

These selected SMID caps trade at below the industry’s present replacement costs. “Selected undervalued SMID caps will once again be potential privatisation targets, in our view,” said MIB.

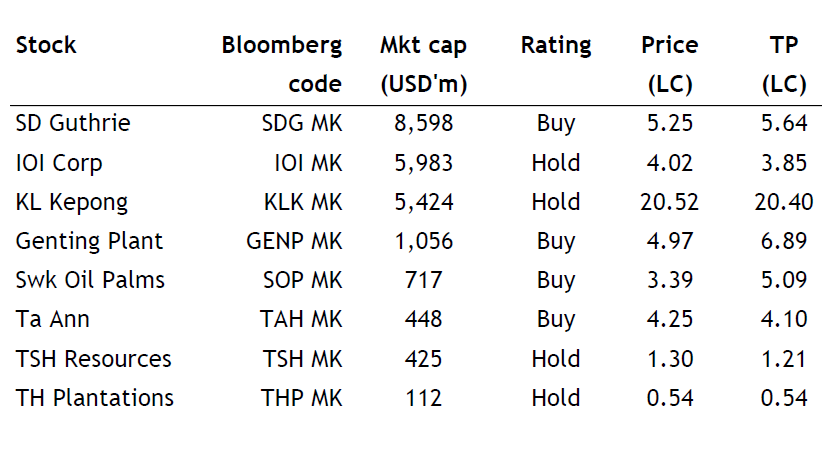

MIB opines SOP and HAPL are prime candidates as any privatisation exercises at present market caps can be self-funded by their high net cash holdings. —Oct 28, 2025

Main image: Ariyan International