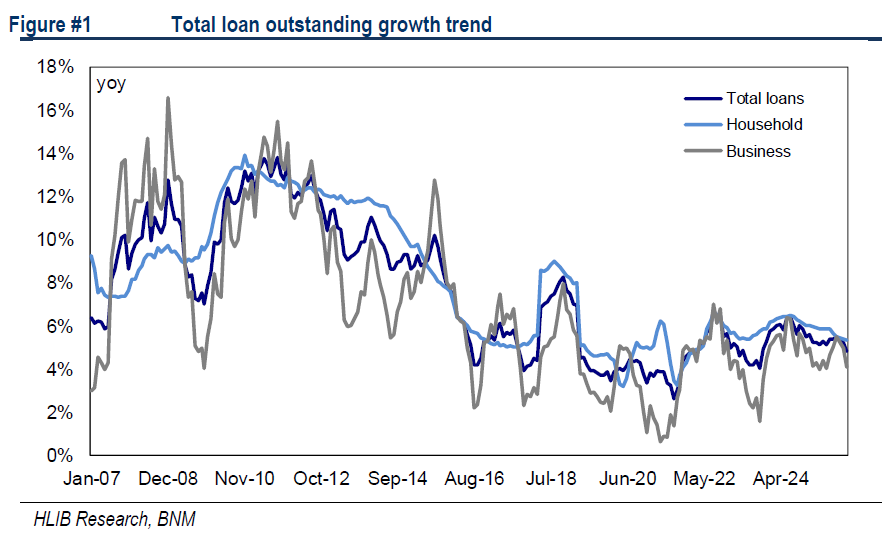

SYSTEM loan growth moderated to +4.8% year-on-year (YoY) in Dec, finishing marginally below Hong Leong Investment Bank (HLIB)’s 5.0%–5.5% forecast range.

The deceleration was primarily underpinned by the business (Biz) segment, which tapered to +3.7% YoY due to softer corporate lending.

In contrast, household (HH) credit remained resilient at +5.3% YoY, supported by steady demand for residential and auto financing.

“For 2026, we project growth to hold within a similar band of 4.8%–5.3%, underpinned by robust SME credit appetite and thematic tailwinds from Visit Malaysia 2026,” said HLIB.

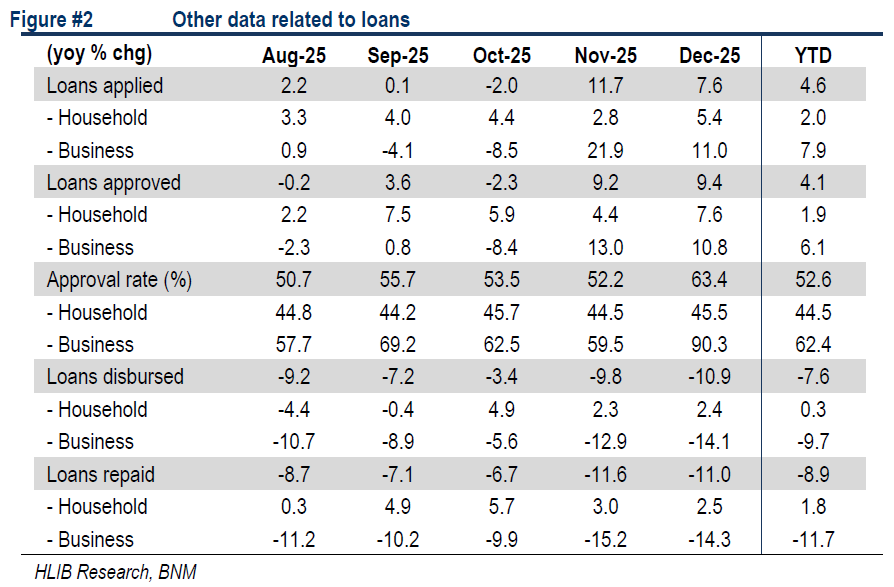

Leading indicators softened as loan application growth slowed to +7.6% YoY. This was largely due to tepid Biz segment demand, which overshadowed a pick-up in HH applications.

Despite this, loan approvals remained firm at +9.4% YoY, as banks maintained an accommodative stance toward HH borrowers, effectively offsetting the more cautious activity in the corporate space.

Deposit momentum gathered pace, logging +3.4% YoY growth on the back of higher current account savings account balances. This improved liquidity saw the system loan-to-deposit (LDR) ratio retreat by 1ppt month-on-month to 89.0%.

“Looking ahead, we anticipate net interest margin (NIM) compression to stabilise in the near term. The depletion of highcost fixed deposits should have been largely completed by Dec-25, allowing for more efficient repricing and a more favourable funding mix moving forward,” said HLIB.

Asset quality held steady as the gross impaired loans ratio improved by 3bps MoM to 1.37%. This positive movement was broad-based, with improvements across both Biz (-3bps) and HH (-4bps) categories.

“We maintain a sanguine outlook on credit risk; banks remain well-protected by substantial management overlays and provision buffers accumulated over the past five years, providing a significant cushion against any potential uptick in impairments,” said HLIB.

HLIB maintains Overweight on the sector. They believe the KLFIN has further legs, with the sector currently trading at 2SD below its pre-pandemic 5-year mean P/B.

This valuation gap is increasingly unjustified given the potential for sector-wide re-ratings, particularly as more banks could be implementing new capital management plans to drive a robust return on earnings recovery.

Furthermore, the KLFIN Index remains a prime beneficiary of foreign fund inflows amidst an emerging markets rotation, bolstered by undemanding valuations and a compelling dividend yield exceeding 4.5% amidst a strengthening ringgit landscape.

This yield spread provides an attractive alternative to the 10-year MGS, supporting a favourable risk-reward setup for broad-based accumulation. —Feb 3, 2025