JANUARY 2026 total industry volume (TIV) stood at 64,298 units. The -29.1% month-on-month (mom) decline was expected due to seasonality, while the +28.7% year-on-year (yoy) increase was mainly supported by spill-over demand from new model launches toward end of calendar year 2025 (CY25).

“Sales this month are expected to be subdued due to the shorter working month,” said MBSB Research.

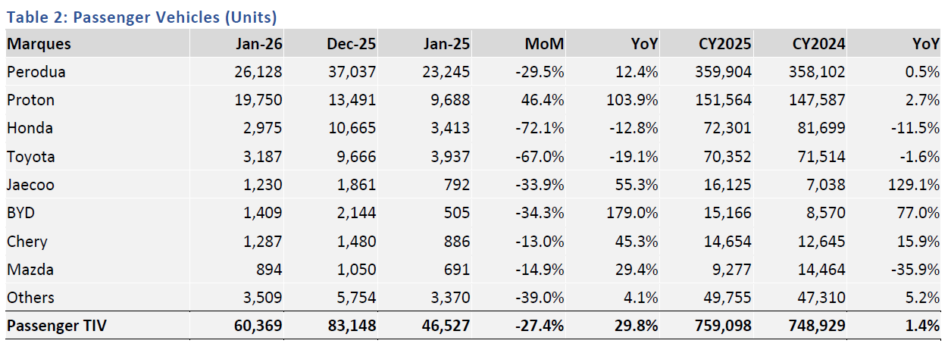

Growth in the passenger vehicle segment (+29.8% yoy) was mainly driven by national marques, particularly Proton (+103.9% yoy) and Perodua (+12.4% yoy), with the former contributing the most.

This was supported by strong demand for Proton’s newly launched Saga and e.MAS 5, both of which are the best-selling models in their respective segments.

The Saga was the top-selling model overall in Jan-26 with over 70k bookings, while the e.MAS 5 has reportedly garnered more than 14k bookings.

As a recap, battery electric vehicles (BEVs) recorded 30,848 units (+108.9% yoy) sold in CY25, accounting for 4% of TIV.

As it stands, the RM250k minimum price and 200 kW power requirement apply to new CBU BEVs regardless of brand presence.

“We are seeing a growing number of CKD BEV investments materialising this year among non-national marques, supported by the tax exemption through end-CY27, although it remains uncertain whether the relatively short window is sufficient to incentivise further long-term local assembly plans,” said MBSB.

MBSB maintains their full-year TIV forecast at 788k units this year, implying a -4.0% yoy decline from last year’s 821k units (+0.2%yoy), following four consecutive years of growth. This is broadly in line with the Malaysian Automotive Association’s (MAA) forecast of a -3.8%yoy decline to 790k units.

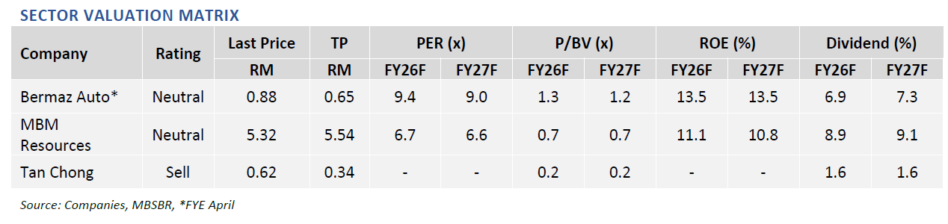

“We currently have no top pick for the sector pending next week’s results releases,” said MBSB. —Feb 20, 2025

Main image: Prodensa