UPSTREAM plantation margins turned out better than Kenanga had expected, hence their estimates for larger, more income-diversified integrated planters were fine.

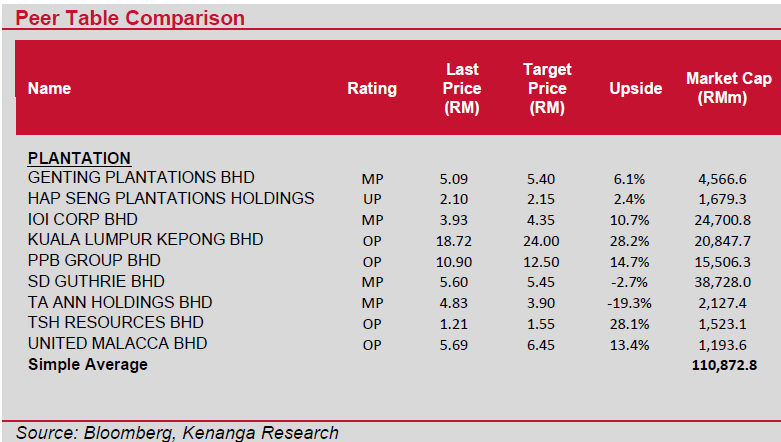

“ IOI, PPB, and SDG came within our expectations leaving only KLK which came below our forecast due to weaker crude palm oil (CPO) prices and property contributions,” said Kenanga.

However, purer planters with more sensitive upstream earnings generally beat their expectations in quarter four calendar year 2025 (4QCY25).

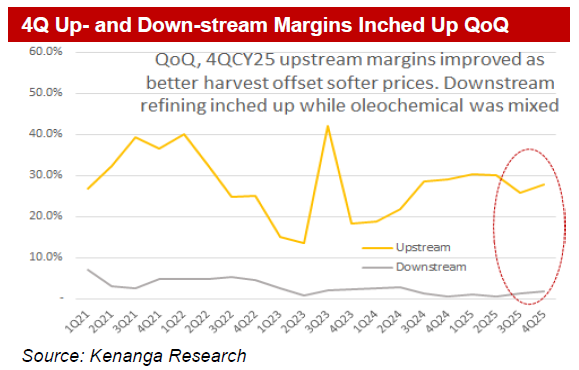

For Kenanga universe of planters, 4QCY25 upstream revenue was mixed as muted CPO prices were offset by better FFB harvest.

Rising 4% quarter-on-quarter (QoQ) and 2% year-on-year (YoY), fresh fruit bunch (FFB) production in 4QCY25 was the strongest quarterly production in five years which helped lower unit CPO cost even though CPO prices eased.

Consequently, upstream profit before tax ended up firmer QoQ but slipped YoY, reflecting the quarter’s revenue performance as well as underlying trend in margins.

“Peering into 1QCY26, we expect upstream margins to either stay flat or ease a little on flattish CPO and PK prices but on seasonally lower harvest while higher labour, fertiliser and energy costs are creeping up,” said Kenanga.

While planters generally guided for stronger FFB production (ranging between 3-16% higher) in CY26, Kenanga is more cautious as CY25 saw unusually strong harvest.

Specialty products are faring better thus far but forward specialty food product margins are set to come under pressure as well due to new capacity with Johor Plantation-Fuji Oil plant at Kota Tinggi commencing later this year while KLK-AAK joint venture Pasir Gudang plant is due later next year.

Nevertheless, downstream momentum has improved QoQ. 4QCY25 revenue rose (+1% QoQ, +7% YoY) with the strongest margins since mid-CY24, thus 4QCY25 earnings rose 36% QoQ and 191% YoY. While probably early to be bullish on downstream, the segment may be bottoming with the worst possibly behind us.

After turning positive in 3QCY25 from a lumpy land disposal gain of RM490m by SDG, 4QCY25 non-plantation segment reverted into losses again. However, more frequent positive contributions are expected as SDG, KLK, and GENP are pushing more aggressively into real estates.

Consequently, flattish CY26 inventory is likely leading to CPO prices initially softening on better-than-expected palm oil harvest in CY25 but still staying firm at RM4,100 per MT over CY26-27.

“With limited downside risk and undemanding valuations but no strong upside catalyst, we stay Neutral,” said Kenanga.

The divergence between the strong FBM KLCI/KL Plantation Index and CPO price softness also suggests limited upside, potentially some downside risk.—Mar 6, 2026

Main image: Mongabay