THE ONGOING conflict in the Middle East has rattled global energy markets, pushing Brent crude prices up by more than 50% and sending gasoil prices surging over 70% since late February 2026.

However, the direct impact on the palm oil supply chain appears relatively contained.

This is largely because the industry is heavily concentrated in Asia, particularly in Indonesia and Malaysia, which together account for more than 80% of global production.

Additionally, over 60% of palm oil consumption takes place within the region itself.

In fact, just four countries (Indonesia, India, China and Malaysia) accounted for roughly half of global palm oil demand last year, underscoring the sector’s strong regional base.

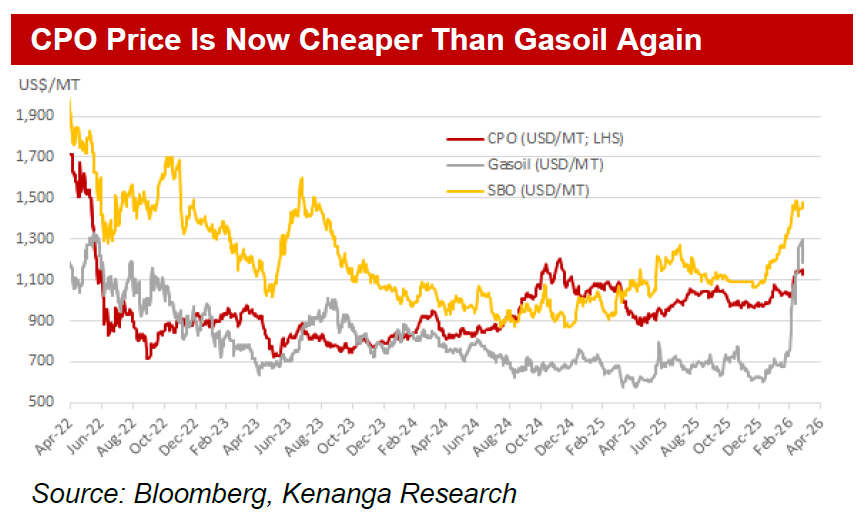

However, about 22% of edible oil goes into the production of bio-diesel, hence the recent spike in crude oil prices have led to higher edible oil prices as well, to the extent that CPO price is now cheaper than gasoil price.

The year 2025 was a good year for the plantation sector due to an unusual confluence of higher harvest and stronger prices for crude palm oil (CPO) (and PK); normally higher supply pressures prices.

Therefore, 2026 started with better-than-expected opening inventory and even so the overall outlook is still one of tightness as supply can only match the pace of demand growth in an optimistic case.

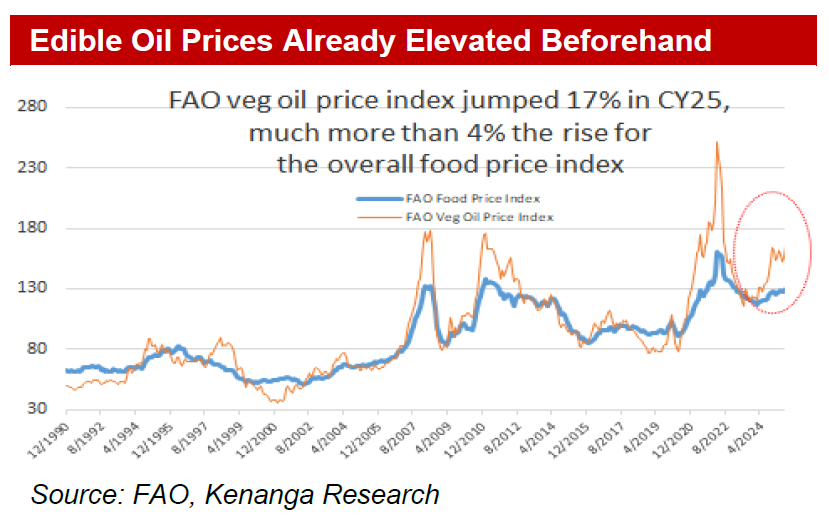

As such, edible oil prices were already elevated compared to other food prices such as meat, dairy, cereals and sugar which formed the FAO Food Price index.

While escalating energy costs is causing fertiliser and transport costs to rise for planters, on the whole the sector is set to be a net beneficiary due to higher CPO prices.

Importantly, besides shipping disruption along the Strait of Hormuz, more lasting damage on regional oil production infrastructure also suggest crude prices may stay not only elevated for several months but likely to settle at prices above the levels seen before the conflict started.

“As the bulk of palm oil is traded within Asia, more muted impact on CPO prices is expected but an upgrade is still warranted for 2026-2027 CPO prices, from RM4,100 per MT to RM4,250 for 2026 and RM4,200 in 2027 as we expect CPO prices to spike in quarter two then ease gradually to around RM4,200 come late 2026 and into 2027,” said Kenanga.

Cost wise, higher energy price is set to push up the cost of fertilizer and transport. In percentage terms, fertilisers typically make up 10-15% and transport 3-5% of total cost.

The larger cost items are labour and depreciation which make up 35-40% and 20% of overall cost respectively.

More importantly, many planters have tendered out and locked in about half their 2026 fertiliser requirements at lower prices already.

SDG has even locked both prices and volume for its entire fertiliser programme in 2026. Kenanga upgrades the plantation sector from neutral to overweight. —Mar 31, 2026

Main image: Whole Foods Magazine