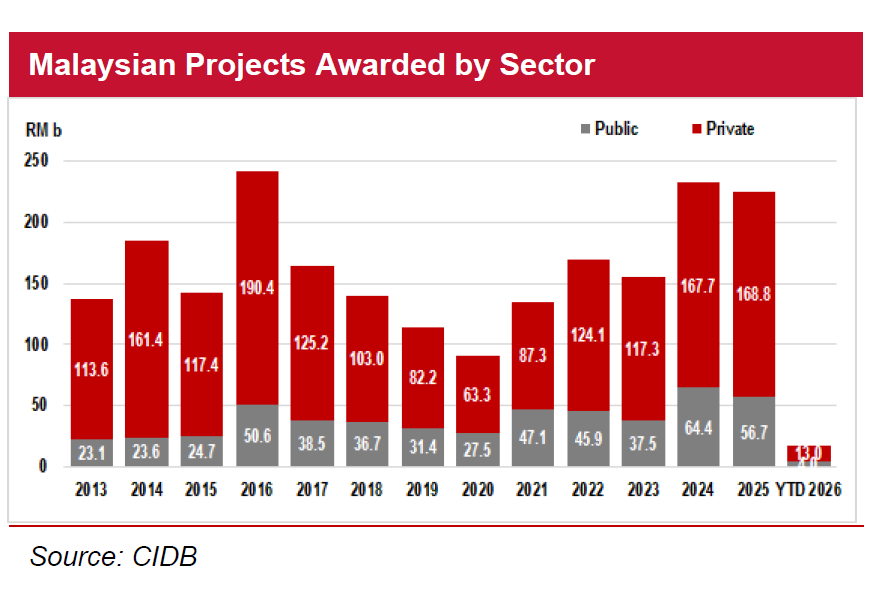

THE CONSTRUCTION Industry Development Board (CIDB) reported that contract awards surged to near-record highs, reaching RM232 bil in 2024 and RM225.5 bil in 2025—marking the strongest levels since the RM241 bil peak recorded in 2016.

Kenanga noted that these figures are well above the long-term annual average of RM140 bil to RM150 bil, and have also outperformed its earlier projection of RM180 bil per year for the 2024–2026 period.

Although the rollout of large-scale infrastructure projects has been slower than initially anticipated, the firm maintains a positive outlook for the sector in 2026.

Visibility is gradually strengthening, supported by progress in both government-led infrastructure initiatives and private sector developments.

Although the timing for MRT3, now with final approval from the Transport Ministry, remains unclear, several key projects are poised for near-term roll-out.

These include the Penang LRT Mutiara Line Packages 2 & 3, Phase 2 of the Pan Borneo Highway, the Sabah-Sarawak Link Road, Subang Airport redevelopment, and the Johor E-ART.

In addition, the KL–Singapore High Speed Rail remains a medium-term catalyst.

Meanwhile, finalization of the Upper Padas Water Dam (Sabah) and the Kerian Water EPCC (Perak) is still pending, though GAMUDA has already secured both water concessions.

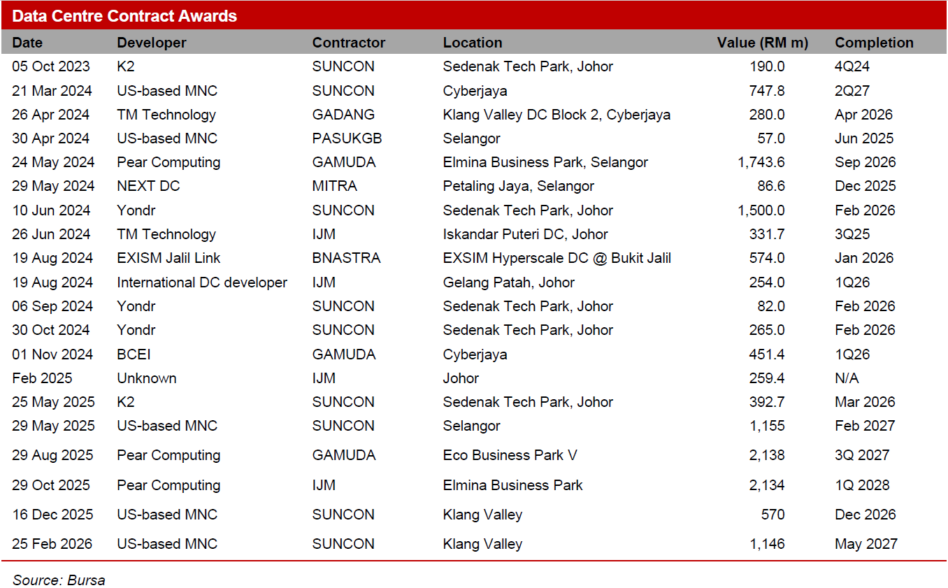

In 2025, six major land transactions involved US tech giants, with Microsoft and Pearl Computing each acquiring two parcels for data centre expansion.

Notably, GAMUDA sold a 389-acre parcel at Springhill Industrial Park, Port Dickson to Pearl Computing for RM455.2 mil, alongside RM1 bil of enabling infrastructure works.

This positions GAMUDA favourably for follow-on work at the site, which can host 800MW-1,000MW of data centre capacity, translating into RM14 bil-RM20 bil in construction value.

The recent surge in building material and transportation costs—driven largely by the Middle East crisis—has resulted in a mixed impact across the sector.

Based on Kenanga’s recent management checks, the implications vary depending on contract structures.

Rising diesel fuel costs are particularly challenging, as these are typically not pass-through expenses under existing contract agreements, leading to direct margin pressure.

Conversely, certain material costs include pass-through clauses, allowing players to mitigate some of the inflationary pressure.

“Despite near-term geopolitical headwinds and a slower-than-expected rollout of infrastructure projects, we remain bullish on the sector,” said Kenanga.

This outlook is underpinned by persistent demand for data centres and sustained capital expenditure commitments from global technology firms.

GAMUDA remains Kenanga’s Top Pick for the sector, supported by strong positioning in upcoming data centre tenders, and its proven track record in overseas markets.

Also, its earnings visibility is backed by a record RM36.6 bil order book, and consistent progress in renewable energy initiatives.

“We also continue to favour SUNCON and IJM among the large caps,” said Kenanga. —Apr 7, 2026

Main image: BizVibe