RECENT ANALYSIS from RHB suggests that heightened geopolitical tensions and the ongoing energy crunch have not dampened investment momentum in Malaysia’s data centre (DC) sector.

Feedback gathered from industry participants and suppliers on the ground indicates that demand from hyperscale operators and colocation (colo) providers remains resilient, with most expansion plans proceeding largely as scheduled.

A major driver behind this continued growth is the surge in artificial intelligence (AI)-related workloads, which continues to underpin long-term demand despite lingering supply chain challenges and the prospect of higher development costs.

At the same time, growing concerns over infrastructure security, alongside persistent vulnerabilities in global supply chains, may prompt operators to rebalance their DC portfolios, shifting focus from the Middle East towards South-East Asia.

Malaysia stands to benefit from such a shift. Its emergence as a strategic DC hub — bolstered by ongoing developments from US-based hyperscalers establishing new cloud regions — positions the country favourably.

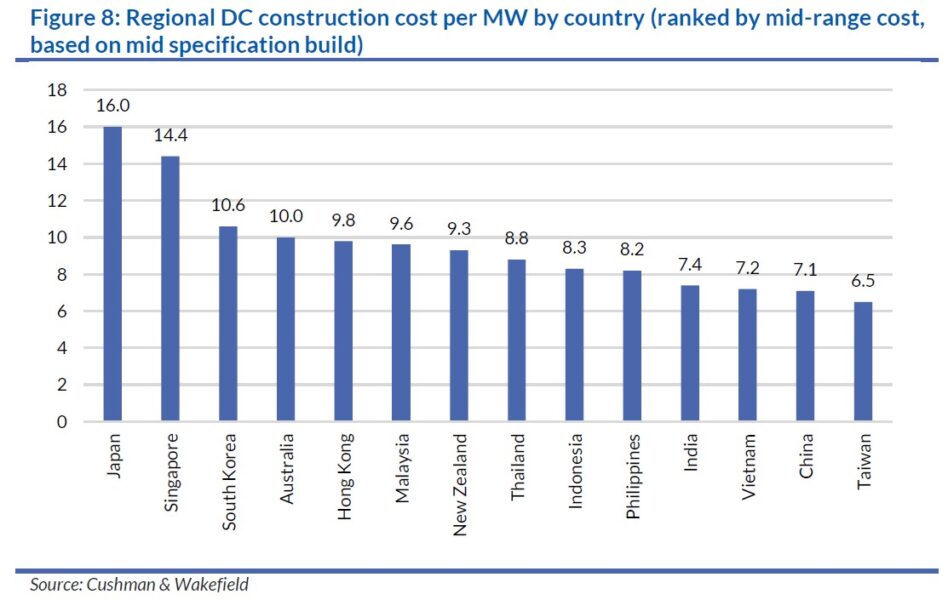

Competitive land and energy costs, coupled with political stability and supportive policy frameworks, further enhance Malaysia’s appeal as a preferred destination for data centre investments.

“Our assessment indicates that the cost of DC build-outs is still manageable despite the energy crisis due to Malaysia’s cost advantage and the use of a cost plus model,” said RHB.

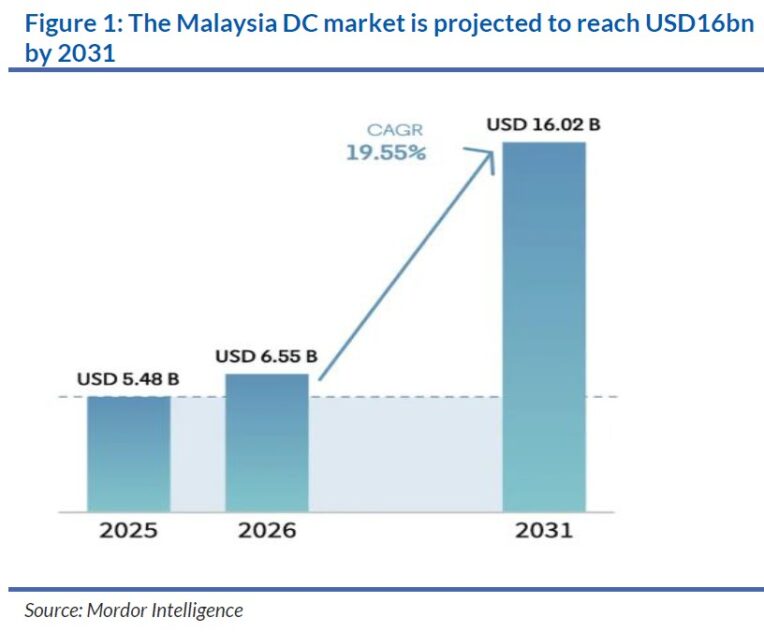

With over 3GW of DC supplies projected into 2030, a staggering MYR90 bil in construction value awaits contractors. Malaysia’s regulated electricity tariffs remain one of the most competitive in the region, with minimal exposure to fuel cost fluctuations caused by the Middle East conflict.

RHB estimates that DCs will incur an average USD0.17/kWh tariff cost, even with coal prices hitting USD220 tonne, still lower than current prices in the Philippines and Singapore.

Meanwhile, the additional water supply coming on stream is sufficient to meet DC demands, especially in key hotspots.

While the Strait of Hormuz’s closure has lengthened production lead times for graphics processing units (GPUs), AI accelerators and high bandwidth memory (HBM) modules, the use of close-loop helium recycling systems have averted production shutdowns by wafer foundries.

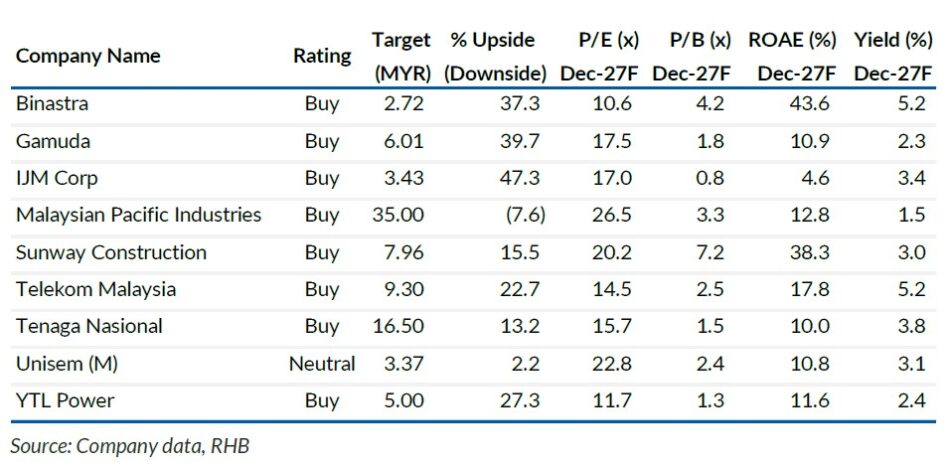

“Gamuda and Sunway Construction are our preferred DC construction picks, supported by their strong DC construction orderbook of MYR5 bil each (11% and 55% of total orderbook respectively) and execution track record,” said RHB.

For energy exposure, they like Tenaga Nasional with electricity demand growth fuelling capex investments and regulated earnings growth.

Telekom Malaysia is their preferred telco DC play, backed by its extensive fibre backhaul and submarine cable ownership, and direct exposure to increased colo demands.—Apr 28, 2026

Main image: bridgedatacentres.com