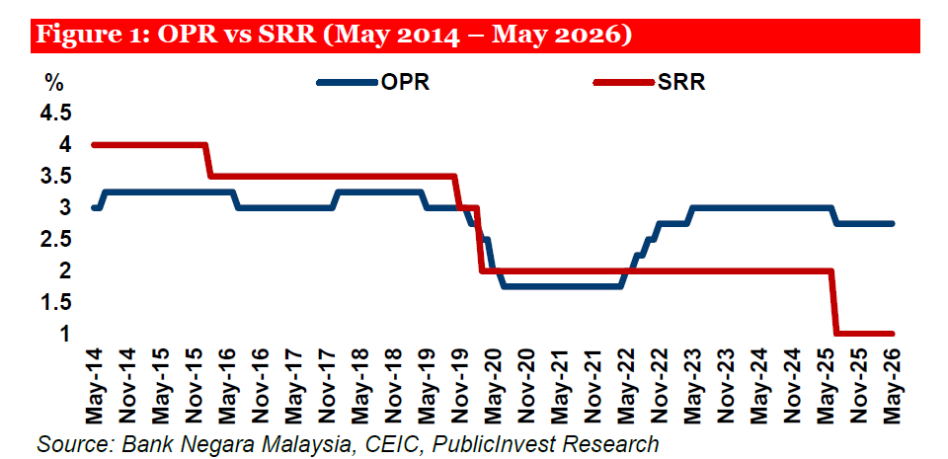

BANK NEGARA Malaysia (BNM) has maintained the Overnight Policy Rate (OPR) at 2.75% following its third Monetary Policy Committee (MPC) meeting for 2026, a decision widely anticipated by economists and aligned with market expectations.

The central bank said the current monetary policy stance remains suitable in supporting price stability while allowing for steady and sustainable economic expansion.

Meanwhile, the Statutory Reserve Requirement (SRR) was also left unchanged at 1.00%, after the cumulative 100 basis point reduction introduced in May last year.

In its latest MPC statement, BNM highlighted that Malaysia’s economy continued to record encouraging growth momentum in the first quarter of 2026.

This was largely supported by resilient domestic demand alongside healthy export activity.

Consumer spending is expected to remain supported by stable employment conditions, wage increases and ongoing policy assistance measures.

On the investment front, growth continues to be driven by the rollout of long-term infrastructure initiatives, smaller public sector projects, progress in approved investments and the implementation of various national development master plans.

However, BNM adopted a more guarded tone regarding the global environment, particularly citing the escalating conflict in the Middle East as a growing concern for both domestic growth and inflation prospects.

While exports, especially in the electrical and electronics (E&E) segment, continue to provide support, tourism-related spending is forecast to expand at a more measured pace as the post-pandemic recovery enters a more normalised phase.

At the global level, BNM noted that economic activity remains relatively resilient, underpinned by domestic demand across economies and continued expansion in the global technology sector.

Nonetheless, policymakers acknowledged that risks linked to the Middle East conflict are becoming more pronounced, particularly through rising energy and commodity prices as well as disruptions to global supply chains.

The central bank cautioned that downside risks remain elevated due to uncertainty surrounding the duration of geopolitical tensions, tighter global financial conditions and lingering concerns over asset valuations in financial markets.

On the upside, BNM said growth prospects could improve if geopolitical tensions ease, supply chains stabilise further, technology spending strengthens and governments introduce more growth-supportive policies.

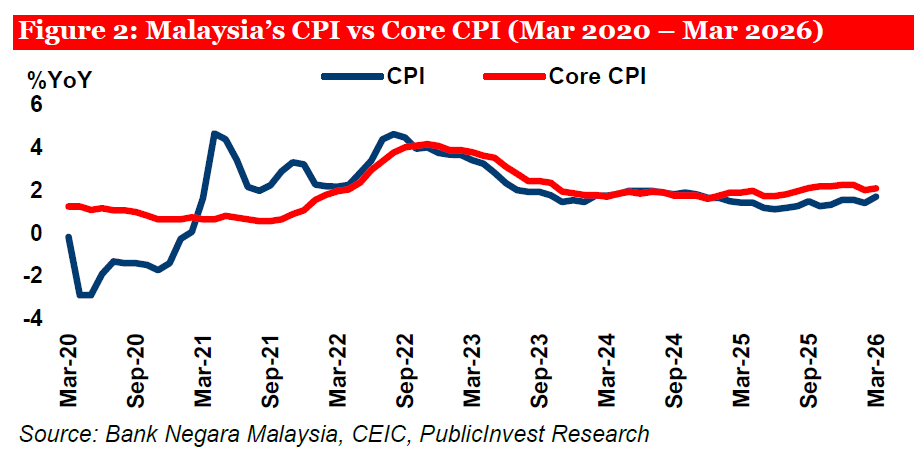

Headline and core inflation averaged +1.6% YoY and +2.1% YoY, respectively, in 1Q26, still within BNM’s 2026 forecast ranges of 1.5% to 2.5% and 1.8% to 2.3%.

BNM now expects higher global commodity prices from the Middle East conflict to raise domestic cost pressures and cause inflation to edge higher, marking a firmer inflation tone compared with March.

Nevertheless, the MPC continues to view the impact on both headline and core inflation as contained, supported by domestic policy measures and stable demand conditions.

“We think BNM still treats the shock as an external cost-push risk rather than a demand-led inflation cycle,” said Public Investment Bank (PIB).

We maintain our OPR view at 2.75% through 2026. While the inflation outlook has become less benign, we do not think the current shock is sufficient to push BNM into a tighter policy stance at this stage.

Our 2026 headline CPI forecast remains at +2.4% YoY, close to the upper end of BNM’s 1.5% to 2.5% forecast range, reflecting a higher external cost base rather than broad-based demand pressure.

BUDI95 should continue to cap the immediate household fuel shock, with RON95 maintained at RM1.99/litre, although the higher subsidy burden suggests the policy cushion is becoming more costly.

We view a 25bp hike in 4Q26 as a conditional tail risk rather than our base case. Any potential move would likely be framed as policy normalisation, possibly reversing the pre-emptive July 2025 cut, rather than the start of a tightening cycle.

The hurdle remains high and would likely require clearer evidence that elevated oil prices are broadening into core inflation, inflation expectations are becoming less anchored, or upstream cost pressures are feeding more persistently into final consumer prices.

Malaysia’s PPI rebounded to +1.1% YoY in Mar 2026 from -3.4% YoY in Feb 2026, marking the first positive reading since Mar 2025, but this remains a monitoring point rather than a policy trigger for now. —May 8, 2026

Main image: Edgeprop