IJM CORPORATION’S latest results highlight the mixed fortunes facing Malaysia’s infrastructure and property heavyweight.

While construction earnings gained momentum from fast-track data centre projects and a healthy order book, weaker property performance and one-off impairments weighed heavily on overall profitability.

Even so, analysts remain optimistic, pointing to IJM’s exposure to major infrastructure opportunities, strategic port assets and planned asset monetisation efforts as potential drivers of longer-term growth.

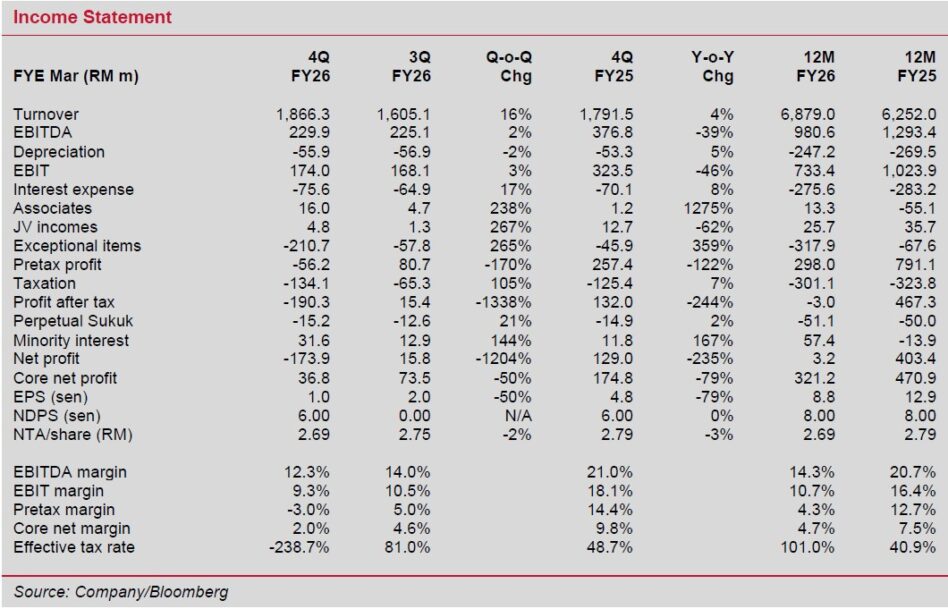

The company’s core profit of RM321.2 mil fell below RHB and consensus estimates, primarily driven by a weaker-than-expected turnaround in core property earnings during quarter four of 2026.

Note that every period mentioned is in the financial year. Construction earnings remained largely on track despite dipping quarter-on-quarter.

“IJM registered a minor headline net profit of just RM3.2 mil, severely weighed down by a RM121.6 mil impairment on unsold inventories (including Hui Hai Plaza in China) and a RM51 mil major maintenance provision for the Vijayapura Tollway in India,” said Kenanga.

Ex-EI, 2026 core profit fell 32% year-on-year (YoY) to RM321.2 mil. This was heavily dragged by lacklustre property earnings, where core profit before tax (PBT) plunged to RM108.5 mil as higher overheads were expensed to nurture long-term investment assets in Malaysia and the UK.

Conversely, Malaysia and Singapore construction earnings jumped 51% YoY to RM247.6 mil, driven by accelerated billings from the 13-month fast-track hyperscaler data centre project that commenced at the end of quarter two of 2026.

Meanwhile, port PBT slid 40% to RM75.1 mil as cargo throughput dropped to 20.6MT due to a key customer undergoing major maintenance.

IJM unveiled plans to unlock and distribute RM3 bil from three key asset monetization exercises over the next three years. This translates to a total NDPS of 83 sen, or roughly 28 sen p.a.

Management has set a new order book replenishment target of RM6b for Malaysia and RM3 bil for overseas. The domestic pipeline is strongly backed by high-margin data centre packages and two semiconductor projects.

Key near-term catalysts include the finalisation of the Penang LRT Mutiara Line (Package 2) by mid-year, alongside the potential rollout of the more than RM1 bil Nusantara civil servant housing project in Indonesia by year-end.

“Concurrently, we introduce our 2028 forecasts, projecting moderate earnings growth of 5% anchored on a steady RM5.0 bil domestic job win assumption,” said Kenanga.

Kenanga likes IJM as it is poised to garner a slice of action in the Penang LRT Mutiara Line given its involvement in the previous LRT projects.

Its strong earnings visibility is underpinned by an outstanding construction order book of RM8.4 bil for Malaysia and new property sales of RM1.2 bil in the first half of 2026.

Also note that its Kuantan Port is the largest port in the East Coast, capturing export and import activities growth, and the potential divestment of its toll road to lighten its balance sheet and recycle capital could act as a re-rating catalyst.

“Outperform maintained,” said Kenanga. —May 29, 2026

Main image: IJM Corporation