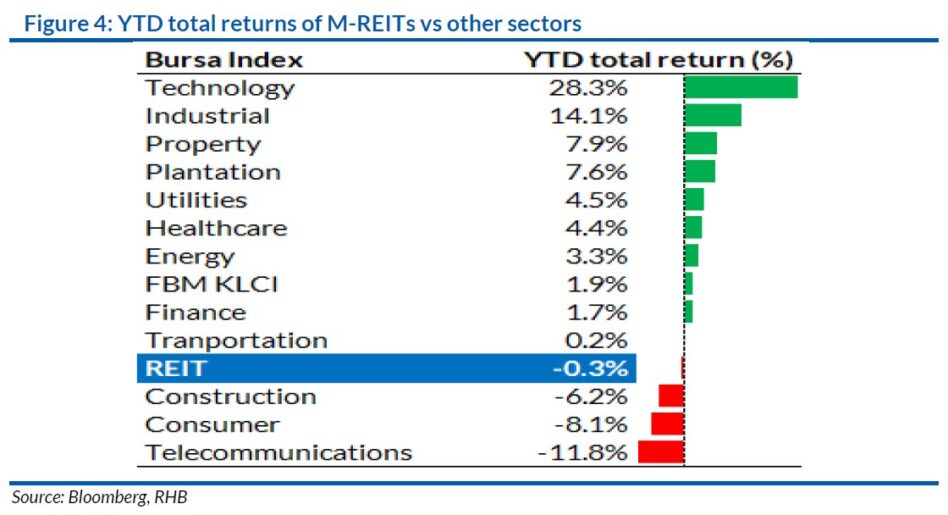

DESPITE lagging the broader market this year, Malaysia’s real estate investment trust (REIT) sector continues to offer an attractive proposition for income-seeking investors.

Backed by stable earnings, resilient occupancy rates and healthy dividend prospects, several M-REITs have delivered strong operational performances, particularly in the retail, office and industrial segments, reinforcing confidence in the sector’s long-term outlook

The Bursa Malaysia REIT Index has underperformed the broader market, declining by 0.3% year-to-date (YTD).

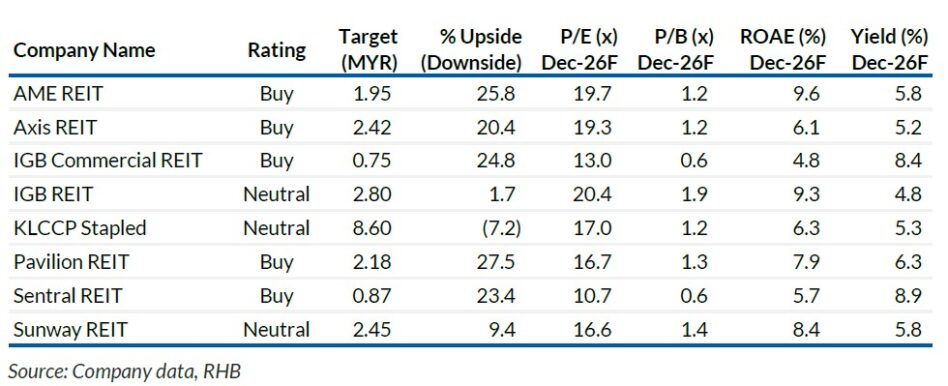

This sector remains compelling for investors looking for yield plays, given the M-REITs’ stable earnings and dividend outlook as well as undemanding valuations.

IGB REIT saw a big jump in quarterly earnings, largely due to contributions from Mid Valley Southkey. For the office REITs, IGB Commercial REIT stood out, with net profit surging by 28% year-on-year (YoY), driven by an improved occupancy rate of 93% (from 89%) and higher average rent per sqf rate of MYR6.64 (from MYR6.42).

In the industrial REIT space, AME REIT recorded 13.0% YoY earnings growth, supported by six new industrial properties, of which the acquisitions were completed over the past 12 months, on top of its assets’ full occupancy rates and positive rental reversions.

Sector fundamentals remain intact, supported by high occupancy levels and stable rental reversions.

RHB Economics expects Bank Negara Malaysia to maintain a broadly stable policy stance, with the OPR projected to remain at 2.75% in 2026.

This should help contain borrowing cost pressures and support acquisition activity. On the demand side, the latest retail sales data from the Department of Statistics Malaysia showed that consumer spending remained resilient, rising 6.3% YoY in Apr 2026.

However, consumer sentiment could soften in the coming months, while the trend of tourist footfalls could also remain uneven.

“That said, we believe prime malls with strong shopper catchments, high occupancy levels, and quality tenants should be better positioned to defend earnings,” said RHB.

Any easing of Middle East tensions could also support a stronger tourism recovery. In the office segment, sentiment remains weak, but yields of 8-9% offer some comfort for investors.

In a market where demand drivers for office space have been lacking, RHB views assets connected to major transport hubs as more resilient.

Meanwhile, industrial REITs should continue to benefit from structural demand drivers, supported by policy initiatives, long WALEs and high occupancy levels, which provide long-term income visibility.—June 23, 2026

Main image: reit.com