FOLLOWING two years of robust expansion, Malaysia’s construction sector is transitioning into a steadier growth phase, although the overall outlook remains encouraging.

In the first quarter of 2026, the value of construction work done rose 8.5% year-on-year to RM46.5 bil. Private sector projects continued to dominate activity, contributing RM30.5 bil or 65.5% of the total.

According to Public Investment Bank (PIB), the private sector remained the primary growth engine, expanding 13.2% from a year earlier.

This was largely supported by a 28.8% increase in special trade activities and a 13.1% rise in non-residential building construction, fuelled mainly by ongoing hyperscale data centre developments.

Meanwhile, public sector construction recorded RM16 bil in work done, representing 34.4% of the total, with modest growth of 0.5% as infrastructure projects under the 13th Malaysia Plan (13MP) continued to progress.

Looking ahead, hyperscale data centres are expected to remain a key driver of the sector.

At the same time, growth is likely to become more diversified, with increasing contributions from transport infrastructure, renewable energy projects, industrial parks and other major infrastructure developments.

Cost pressures also appear to be easing, as inflation in construction materials remains relatively contained, aided by disciplined pricing practices and effective cost management.

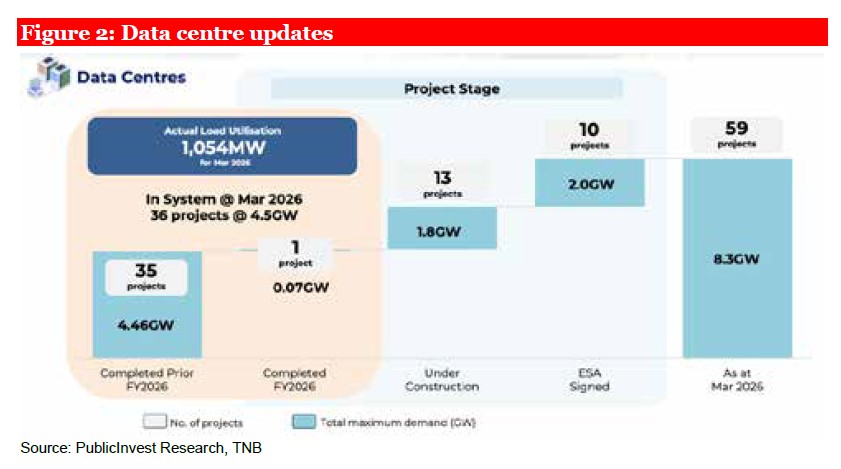

Hyperscale DC remains the sector’s core growth engine, backed by TNB’s RM43 bil grid modernisation plan and an 8.3 GW pipeline.

Ten electricity supply agreement (ESA) totalling 2.0 GW represent RM80 bil in potential construction value, offering strong medium-term visibility.

Adding to this private-sector drive, the government is pressing ahead with key digital infrastructure projects, including JENDELA phase 2, the Submarine Cable Project (SALAM), and a Sovereign AI Cloud, to strengthen digital connectivity and data sovereignty.

The project pipeline of Federal-backed infrastructure projects remains robust, underpinned by the Phase 2 of the civil works package of the Penang Light Rail Transit (LRT) project, Johor Bahru E-ART, MRT 3, the Trans-Borneo Railway, the Perak-Penang water transfer project, and the anticipated Large-Scale Solar 6 (LSS6), which targets 2GW of combined solar and battery infrastructure.

Contractors face cost volatility in 2026, with steel prices stable but cement up 9.3% year-on-year. While profitability remains manageable for now, further cost hikes could pressure earnings.

However, margins are protected by inflation-linked contract clauses, effective cost-control strategies and the ability of major contractors to pass through costs via disciplined pricing.

“Looking ahead, we expect job flow momentum to sustain a pace comparable to the past two years, driving further expansion of the sector order book,” said PIB.

Their top picks among big-cap stocks are Gamuda and IJM, given their extensive experience in public infrastructure jobs.

For small-to-mid-cap stocks, PIB prefers Kerjaya Prospek for its strong unbilled orderbook, resilient earnings, and consistent dividend yield.—July 3, 2026

Main image: turnerandtownsend.com