ACCORDING to Hong Leong Investment Bank (HLIB), the energy sector is poised for sustained growth over the next three to five years, supported by three major catalysts.

First was Tenaga Nasional’s higher capital expenditure. Then there was the rising private-sector demand driven by data centres, and increasing investment in solar-related infrastructure.

HLIB expects Tenaga’s continued focus on transmission network upgrades to create a steady pipeline of opportunities for 132kV to 500kV projects.

At the same time, a growing number of electricity supply agreements (ESAs) and additional main intake substation (PMU) capacity are likely to strengthen demand for data centre-related customer load substations (CLS) through 2027 and 2028.

Solar infrastructure is also set to become a significant growth contributor. Near-term construction activity will be supported by the Large-Scale Solar 5 (LSS5) and LSS5+ programmes, while the upcoming LSS6 and Corporate Renewable Energy Supply Scheme (CRESS) are expected to extend the investment cycle from 2027 onwards.

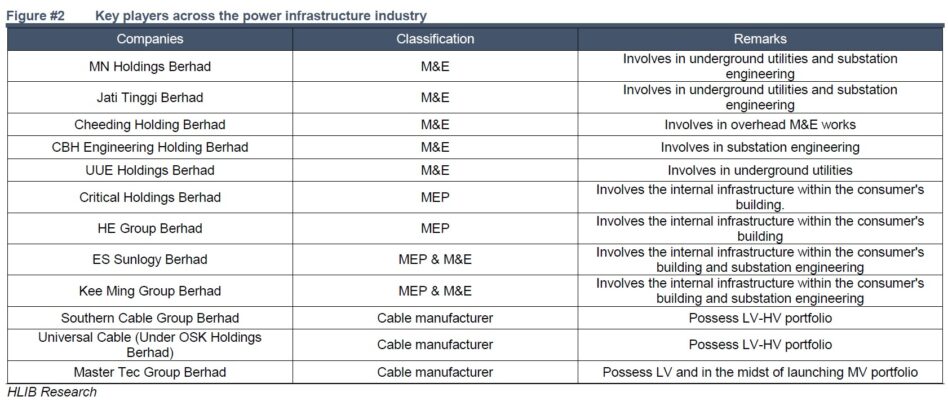

HLIB believes the current power infrastructure expansion increasingly favours mechanical and electrical (M&E) contractors as well as cable manufacturers, rather than traditional mechanical, electrical and plumbing (MEP) players.

The key reason is that the biggest investment opportunities lie within the medium- and high-voltage grid, where Tenaga’s transmission upgrades, data centre connections and renewable energy integration are generating the bulk of new project awards.

Companies with direct exposure to the grid are therefore positioned to benefit from higher-value contracts, stronger barriers to entry and a clearer earnings trajectory than firms focused mainly on last-mile electrical installations.

The combination of DC buildout and Tenaga’s transmission-focused capex is shifting the project mix towards 132kV and 275kV works.

This has been a key driver of M&E contractors’ and cable manufacturers’ orderbooks, given the larger contract sizes and better margin profiles of HV infrastructure jobs.

“We expect the HV opportunity pipeline to continue building into the second half of 2026-2027, with more than five 500kV PMU jobs expected to be rolled out,” said HLIB.

As project sizes grow larger, working capital is becoming a higher barrier to entry. Performance bonds, supplier downpayments and Tenaga’s requirement for M&E contractors to procure HV cables are raising upfront funding needs.

“We believe this should increasingly concentrate project wins among listed players with stronger balance sheets and better access to capital, while smaller unlisted contractors may face greater execution constraints,” said HLIB.

Most of the power infrastructure stocks are concentrated in the ACE market, limiting investor exposure.

The research house thinks this will gradually shift as earnings scale up and more players migrate to the Main Market. This trend is positive for the sector, in their view, as it broadens institutional investor participation and supports re-rating potential.

“We maintain our OVERWEIGHT stance on the power infrastructure sector, underpinned by a multi-year capex upcycle that structurally favours listed grid-exposed players,” said HLIB.

HLIB stays selective and prefer names with clearer order flow visibility, execution edge and funding capacity.

Maintain BUY on MNH and SCGBHD, and initiate coverage on EIPower and UUE with BUY ratings.—July 3, 2026

Main image: brimco.io