The KLCON index had a turbulent start to 2026, with losses reaching 14% by the end of the first quarter.

The sharp decline was largely driven by the outbreak of the Iran conflict in March, which raised concerns that contractors’ profit margins would come under pressure as diesel prices and construction material costs surged.

However, sentiment improved during the second quarter, allowing the index to recover part of its earlier losses and reduce its year-to-date decline to 5%.

According to Hong Leong Investment Bank (HLIB), the rebound was supported by a clearer understanding of the conflict’s actual impact on costs, easing geopolitical tensions, and continued strength in contract awards.

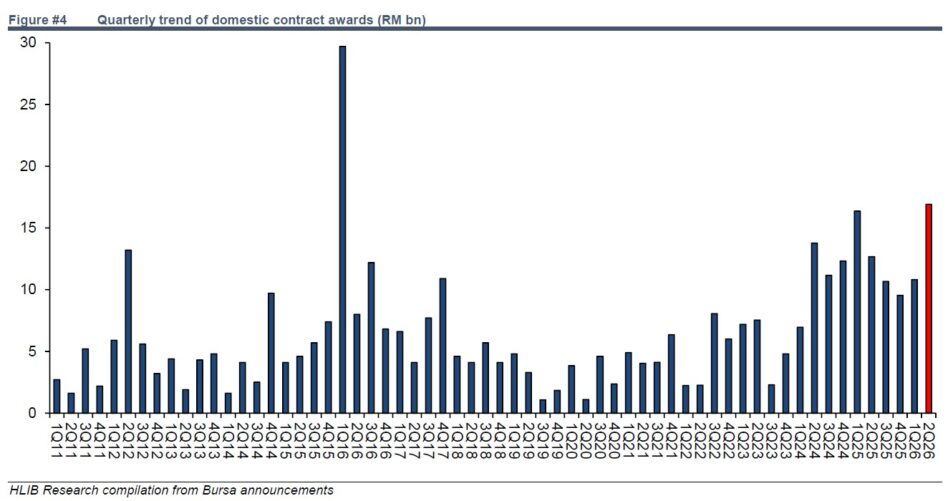

Following a decent tally of domestic contract awards in quarter one 2026 (1Q26) (RM10.8 bil), HLIB data compilation indicates total local job flows in 2Q26 has further risen to RM16.9 bil.

Despite external headwinds, award momentum remained resilient due to robust acceleration in DC main package awards, alongside the crystallisation of various subcontracting opportunities within the DC space (MEP works) as well as conversion of big-ticket infra jobs such as the Ulu Padas water supply scheme.

These more than offset the weakness in commercial & residential flows, which fell 46% quarter-on-quarter to RM2.7 bil.

“As we highlighted earlier, residential tender activity softened as developers and contractors adopted a wait-and-see approach due to renewed

cost pressures and cautious homebuyer sentiment amid the Middle East conflict,” said HLIB.

With RM27.7 bil worth of domestic contract awards recorded in the first half of 2026 (1H26), HLIB expects job flows to gain further momentum in 2H26, potentially lifting the full-year tally to surpass the RM49 bil mark recorded in 2025.

The “second wave” of DC build-outs should drive several sizable DC tenders to fruition for large-cap contractors in 2H26. Meanwhile, an expanding funnel of subcontract packages is expected to cascade down to specialised MEP contractors, evidenced by their bloating DC tenders.

The easing geopolitical uncertainties should also aid residential flows in 2H26 as developers regain confidence to launch new projects amid a more favourable cost environment and improving homebuyer sentiment, in HLIB’s view.

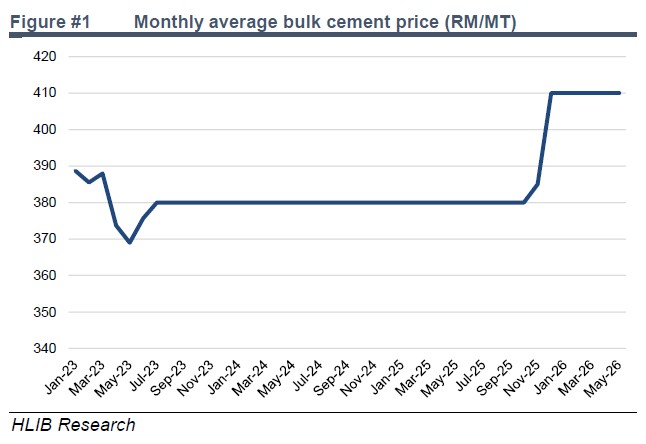

Their recent conversations with contractors suggest that overall construction costs increased 5–10% in 2Q26 versus pre-war levels, driven mainly by higher diesel and ready-mixed concrete (RMC) prices, while steel prices inched up slightly.

Although some degree of margin compression is likely in 2Q26, HLIB believes the worst of the war-related headwinds are now behind for contractors.

Their checks indicate that prices of key inputs such as steel, RMC and industrial diesel are retreating towards pre-war levels since Jun amid progress in the US-Iran peace deal.

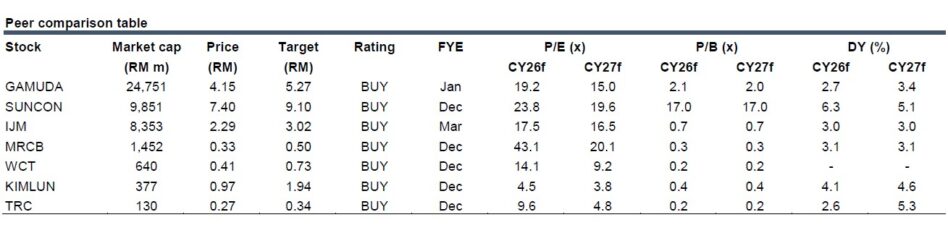

“We reiterate our OVERWEIGHT stance on the construction sector, underpinned by expectations of accelerating job flows in 2H26 following a volatile 1H26,” said HLIB.—July 6, 2026

Main image: Linkedin