ALUMINIUM prices are likely to remain range-bound in the third quarter of 2026, underpinned by easing geopolitical tensions in the Middle East and the gradual restoration of shipping traffic through the Strait of Hormuz.

The improved maritime conditions are expected to reduce supply chain disruptions and facilitate smoother deliveries of raw materials.

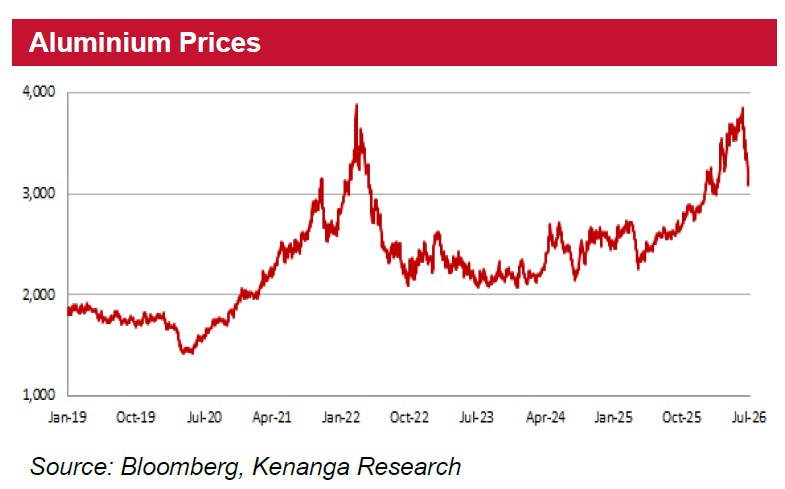

Reflecting these developments, the London Metal Exchange (LME) aluminium spot price has retreated significantly to around USD3,122 per tonne from its first-half 2026 high of USD3,850 per tonne.

Looking ahead, any further gains are expected to be limited, with prices likely to trade within the USD3,300-3,400 per tonne range.

A substantial increase in regional supply, driven by higher production in China and ongoing smelting capacity expansions in Indonesia, is expected to restore market balance.

Consequently, forward aluminium prices for the third quarter of 2026 are projected to stabilise at about USD3,300 per tonne.

The sector’s outlook is also supported by China’s efforts to curb excessive industrial competition through its anti-involution measures and tighter supply discipline.

These policies, which require the retirement of existing capacity before new production can be added, are intended to address oversupply and are expected to reduce annual crude steel production to between 930 mil and 944 mil tonnes, compared with 961 mil tonnes in 2025.

At the same time, freight costs have begun to ease as geopolitical risks in the Middle East subside and shipping routes through the Strait of Hormuz return to normal, providing additional relief to manufacturers and exporters.

While end-users may benefit from lower prices, companies with direct selling prices linked to spot benchmarks capture lower absolute revenue per tonne sold.

For ENGTEX, any downward movement in steel prices translates directly into lower absolute revenue and near-term margin compression due to its price-taker status.

“We maintain our NEUTRAL rating for the sector. Our sector pick is ENGTEX as it remains one of the few players capable of supplying large-diameter ductile iron (DI) pipes, with a historical win rate of around 60%,” said Kenanga.

With lower steel prices likely to accelerate the rollout of mega projects totalling an estimated RM1 bil in tenders, Kenanga believe the Group is well-positioned to secure a meaningful share of these upcoming contracts.—July 10, 2026

Main image: leadrp.net