EL NINO conditions have now emerged. According to the US National Oceanic and Atmospheric Administration, a very strong El Niño is characterised by sea surface temperatures that are at least 2°C above the long-term average.

The agency recently increased the probability of such an event occurring in the fourth quarter of calendar year 2026 to 81%, up from 63% a month earlier.

While even moderate or strong El Niño episodes can influence crude palm oil (CPO) prices, past trends suggest that only very strong events have a meaningful impact on palm oil production.

Extended periods of dry weather can shrink fruit size within six months, while also disrupting flowering, resulting in lower yields that may persist for up to two years.

As a result, CPO prices are expected to remain supported beyond the near-term boost from stronger biodiesel demand linked to tensions in the Middle East.

Historically, El Niño has tended to strengthen CPO prices either during the second half of the year in which it develops or, more commonly, in the first half of the following year.

However, the magnitude of price movements has varied significantly, ranging from an initial quarter-on-quarter decline to gains of between 10% and 40% in subsequent quarters.

“Demand outlook for oleochemical remains uncertain. Coupled with strong palm kernel oil price outlook with competition staying intense, we remain cautious of downstream margins,” said Kenanga.

However, non-plantation earnings, especially property-related earnings, are expected to grow.

SDG’s big push into industrial property is the most notable in the sector and it expects RM500 mil-RM700 mil in related annual profit over 2026-27.

KLK and GENP are also nudging their real estate arms while IOI’s coconut, palm wood and EFB-to-pulp JV projects should start contributing from 2028 onwards.

Meanwhile, underpinned by food and fuel requirements the demand outlook for edible oil is resilient while supply risk is increasing as the likelihood of a severe El Nino grows.

“As such, we believe there is an upward bias towards firmer earnings; hence, our Overweight call is maintained,” said Kenanga.

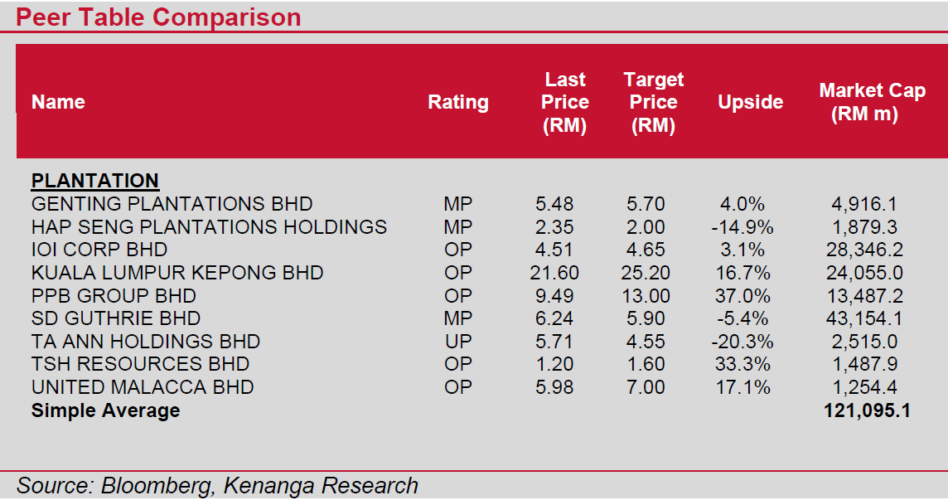

Kenanga’s sector picks are IOI for its sector-leading ROE, contributions from new ventures and strong quarter four financial year 2026, KLK for sensitivity to CPO prices and stronger push into property.

Also, Kenanga chose UMCCA for its still maturing estates and attractive ratings, and TSH for its upstream CPO price sensitivity with ongoing 40% expansion in new planting.

PPB appears oversold with decade low ratings considering the group’s strong FMCG positions in China, India and SE Asia barring some near-term uncertainties over WIL’s Indonesia operation.—July 13, 2026

Main image: ukragroconsult.com