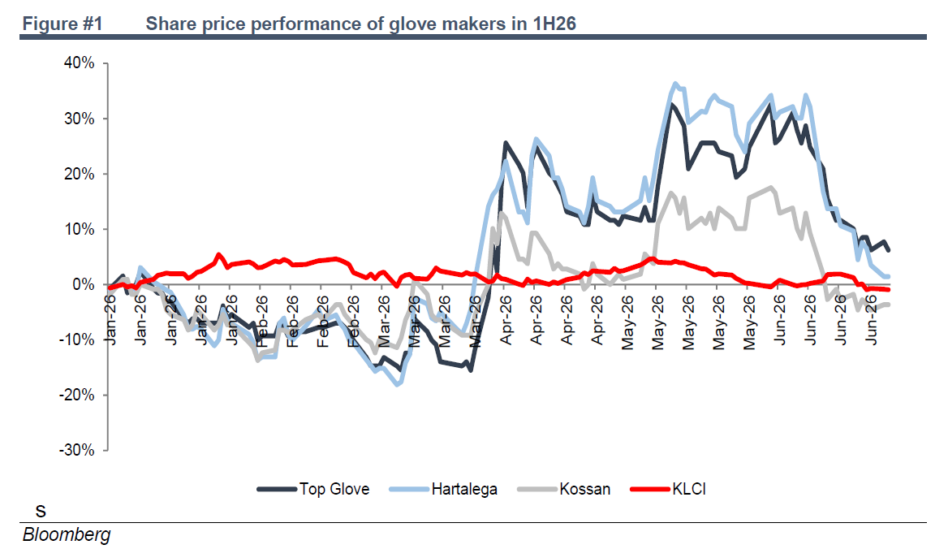

DURING the first half of 2026, glove manufacturers delivered mixed share price performances.

Top Glove gained 6.2% and Hartalega rose 1.4%, both outperforming the FBM KLCI, which slipped 1.0%. In contrast, Kossan declined 3.6%, lagging the broader market.

The sector’s outperformance was largely concentrated between May 13 and June 12, when investor optimism grew over stronger near-term earnings.

This was driven by increases in average selling prices (ASPs), which were sufficient to offset rising raw material costs.

Investor sentiment also received a boost from expectations that supply constraints for nitrile butadiene rubber, following the closure of the Strait of Hormuz during the Iran conflict, could accelerate consolidation within the glove industry.

However, confidence faded after the United States and Iran signed a 14-point peace memorandum in mid-June, which included the reopening of the Strait of Hormuz.

The development shifted market attention back to persistent concerns over structural oversupply in the glove sector.

Nevertheless, the ceasefire remains fragile, with renewed armed clashes reported within a week of the agreement.

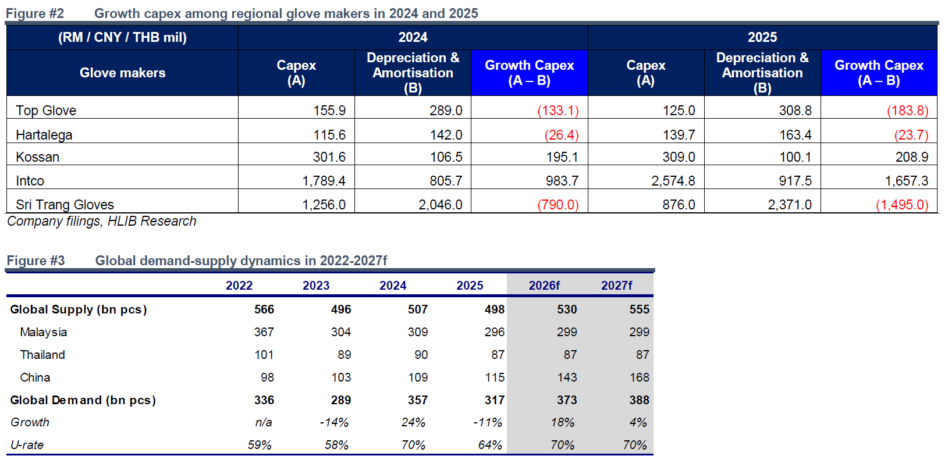

Should the Strait of Hormuz remain fully operational, oversupply is expected to remain the key overhang on the sector, particularly as China’s largest glove producer, Intco Medical Technology, continues its aggressive capacity expansion.

“We note that Intco’s capex exceeded depreciation & amortisation (D&A) by a wider margin in 2025 than in 2024, indicating continued capacity expansion,” said Hong Leong Investment Bank (HLIB).

For perspective, Intco’s annual installed capacity increased from 87bn pcs (Nitrile: 56bn pcs; PVC: 31bn pcs) in 2024 to 103bn pcs (Nitrile:70bn pcs; PVC: 33bn pcs) in 2025.

In contrast, Thailand’s largest glove manufacturer, Sri Trang Gloves, has consistently recorded capex below D&A, suggesting that most spending has been directed towards maintenance rather than capacity expansion.

Domestically, Malaysian glove manufacturers have generally reported capex below D&A over 2024–25, except for Kossan, whose higher capex was mainly allocated to land acquisition and cost optimisation initiatives.

“We believe Intco will continue to build new capacity in 2026 and beyond, with the strategy to deliberately keep industry-wide plant utilisation rate below the equilibrium threshold of 85%,” said HLIB.

This would likely cap ASP at USD15/1k pcs in non-US markets and USD16–16+/1k pcs in the US, thereby squeezing regional competitors into razor-thin or even negative margins.

Over time, this strategy could enable Intco to gradually gain market share as weaker players struggle to remain commercially viable.

Notably, Intco appears well positioned to sustain profitability under such a pricing environment.

“We retain our Neutral sector rating with all three glove makers under our coverage rated Hold,” said HLIB.

In their view, the fragility of the SoH’s reopening could once again act as a tailwind for ASP adjustments, temporarily eclipsing structural oversupply concerns.

Furthermore, share price of glove makers have also corrected since mid-Jun.—July 13, 2026

Main image: Bloomberg