THE escalation of the US-Iran conflict on Feb 28, followed by the closure of the Strait of Hormuz, a critical global shipping route for crude oil and liquefied natural gas (LNG), has reshaped the global environmental, social and governance (ESG) landscape.

Although the energy disruption has encouraged greater investment in renewable energy (RE) and underscored the need for stronger energy independence, the overall impact on global sustainability has been largely negative.

Surging energy prices, higher inflation and rising financing costs have dampened the pace of green investments, while concerns over energy security have led many countries to rely more heavily on fossil fuels, temporarily shifting priorities away from long-term decarbonisation goals.

Heading into the second half of 2026, Hong Leong Investment Bank (HLIB) believes the ESG agenda is increasingly centred on resilience and energy security, rather than climate action alone.

Policymakers and investors are now placing greater emphasis on building secure and reliable energy systems alongside efforts to reduce carbon emissions.

In Malaysia, 2026 had been expected to mark the introduction of a carbon tax.

However, the research house believes its implementation could be pushed back as the government seeks to avoid imposing additional financial burdens on businesses and households amid the economic challenges stemming from the US-Iran conflict.

While a postponement would provide short-term relief for businesses by delaying another layer of cost pressure, it could also deepen long-term structural risks as the EU’s Carbon Border Adjustment Mechanism (CBAM) has already entered its operational phase, priced at EUR75.36/EUR75.28 in 1Q26/2Q26.

Given Malaysia’s position as the EU’s 16th largest source of imports, with the former’s exports to the latter valued at EUR30.35 bil in 2025 and a sizeable share of shipments exposed to CBAM covered sectors, further delays in domestic carbon pricing may have implications for Malaysia’s longer-term export competitiveness.

“Despite ongoing internal and external headwinds in the ESG space, we expect Malaysia’s ESG momentum in the second half of 2026 to be driven by localised, project-level progress, with waste management remaining one of HLIB’s preferred themes,” said HLIB.

Under Malaysia’s Plastics Sustainability Roadmap and the Circular Economy Blueprint for Solid Waste (2025–2035), the Extended Producer Responsibility (EPR) framework for packaging begins its rollout in 2026.

Producers and brand owners are financially responsible for the collection and recycling of packaging waste at the end of its lifecycle.

The initial phase commenced on a voluntary basis this year and is scheduled to become mandatory by 2030, covering six material streams, which are plastic, paper, glass, aluminium, metal, and others.

From a waste management perspective, HLIB believes EPR could improve waste segregation and collection rates, leading to higher-quality feedstock for recycling and Waste-to-Energy (WTE) facilities.

This would help address one of the key operational challenges facing WTE projects today which is inconsistent feedstock quality.

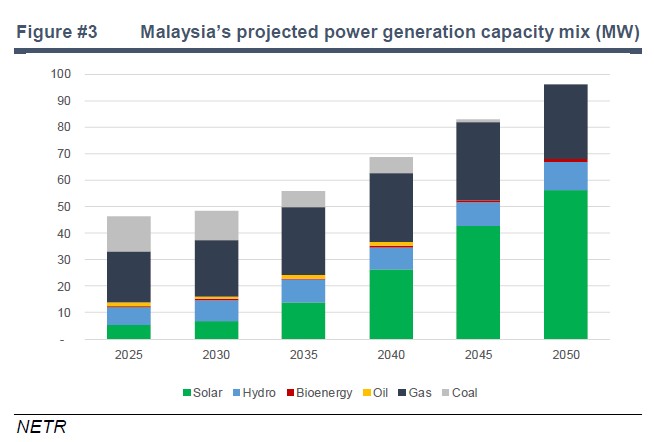

“Looking into the second half of 2026, we believe the RE sector continues to offer the most direct and liquid exposure to the security-driven sustainability theme,” said HLIB.

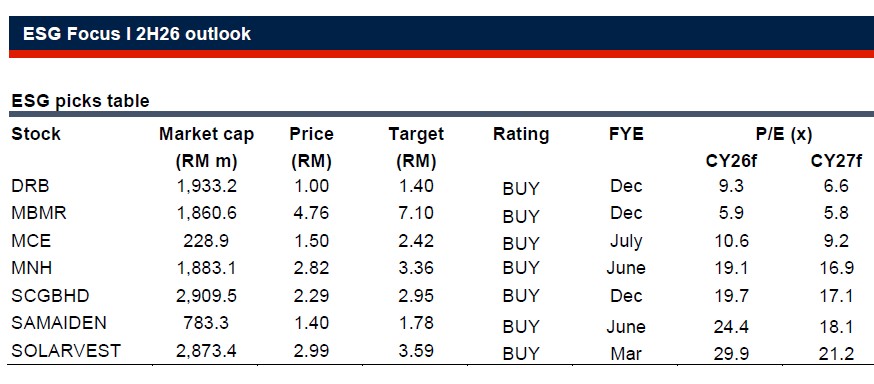

The research house highlighted Samaiden Group and Solarvest Holdings as key beneficiaries, supported by upcoming catalysts including the refinement of the CRESS mechanism and the anticipated rollout of the LSS6 tender.

Beyond traditional solar, HLIB views WTE as an emerging opportunity. The sector benefits from defensive, long-term fundamentals, underpinned by a recurring supply of municipal solid waste, government-backed tipping fee structures, and growing landfill constraints.—July 14, 2026

Main image: mindfulpollinator.com