AFTER a strong calendar year 2025 (CY25), easier or flatter sector earnings are expected in CY26 but staying healthy.

Larger integrated players are busy diversifying beyond palm oil in search of growth while many non-integrated ones have re-built their balance sheet substantially.

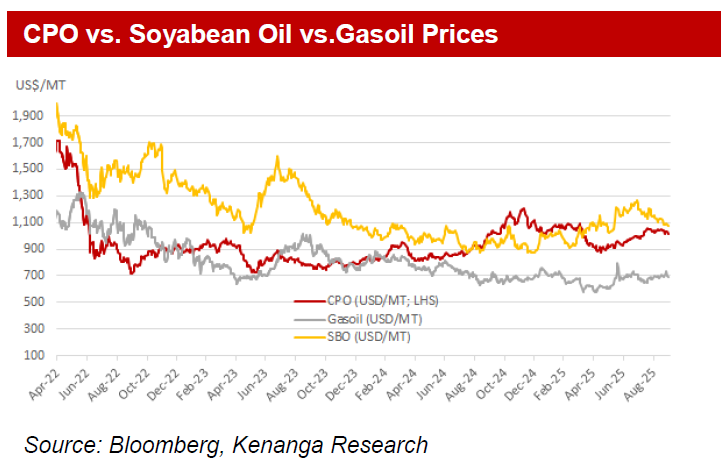

Unusually, the quarter three (3Q) crude palm oil (CPO) price for this year was higher than even 2Q.

Coupled with the usual peak harvesting season, there was plenty of crop to sell at good prices in 3QCY25.

“Given such positive underpinnings, we would not be surprised to see, broadly, a good set of 3QCY25 results for many planters,” said Kenaga Research.

Do note, individual planter earnings hinges on actual realised CPO price, individual estate yields also vary due to terrain, micro-climate and planting materials differences as well as cost variation.

Globally, annual edible oil production is often highest in the third quarter, hence prices tend to moderate then.

However, for this year, 3QCY25 edible prices firmed up 8% quarter-on-quarter (QoQ) as global supply stayed tight while demand held firm.

Not surprisingly, CPO prices also inched up in 3QCY25 to RM4,271 per MT instead of softening. Year-to-date (YTD) July-Sept CY25 CPO price of RM4,350 per MT is also 9% ahead when compared to the same 9-month average of RM4,003 a year ago.

Moreover, if a planter were to then sell their entire 4QCY25 output at current 3-month CPO futures, its full-year CY25 CPO

price may well exceed the already good CPO price achieved last year. With CY26 fast approaching, the debate is now shifting to the sustainability of current price trend.

YTD production of 14.471m MT is also running 4% ahead of the MPOB’s 10-year average Jan−Sept output of 13.963m MT but still in line with Oilworld, USDA, and our expectation of full-year CY25 output of 19.2m MT – 19.4m MT from Malaysia.

Technically, current Sept output is below last month’s output but the dip is very marginal, Sept output is essentially flat, hence the usual production peak in October may still be possible though we expect production to stay flattish.

Rapeseed and sunflower production in CY25 were affected by poor weather in Europe. This should normalise in CY26 along with continual expansion in Latin American soyabean planting.

Together with slower but still recovering palm oil supply, CY26 should see additional 5m-7m MT increase in edible oil supply around the world.

Meanwhile, demand, especially for palm oil will likely hinge on bio-fuel policy. Indonesia is carrying out trials in preparation to raise palm-based bio-diesel blend from current 40% (ie B40) to B50 in 2H CY26 if testing concludes well.

Edible oil prices, including palm oil prices, should thus stay firm in view of flattish YoY inventory moving into CY26.

There is also minimal room to absorb any negative surprises in supply downside, be it poor weather, supply-chain disruption or changing buying patterns due to geo-political tension.

While upstream margins should inch up in 3Q, and possibly 4Q, on robust CPO prices and lower unit cost from higher seasonal output and elevated PK prices, downstream prospects are still clouded by uncertainties over global economic activity and demand.

A robust 3QCY25 and robust CY25 earnings for the plantation sector is taking shape. However, with improving edible oil supply expected in CY26, easier CPO prices are thus likely.

Consequently, sector earnings are expected to moderate, or stay flat moving into CY26. However, current undemanding valuations already reflects this trend.

With no strong upside catalyst in sight, we are keeping our NEUTRAL weight unchanged. —Oct 13, 2025

Main image: UKR Agro Consult