RHB believes the commercialisation of YTL Power’s first artificial intelligence-data centre (AI-DC) will help to seal more future deals despite income from co-location services remaining minimal.

YTL PowerSeraya’s (PowerSeraya) earnings moderation should be cushioned by improving Wessex Water post a tariff revision.

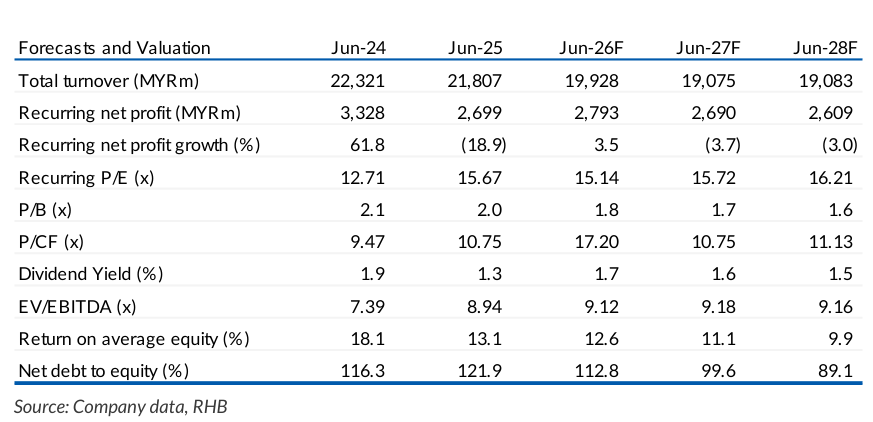

“We see further re-rating catalysts if YTLP is able to secure new domestic gas plant and battery storage projects,” said RHB.

Quarter four financial year 2025 (4QFY25) core profit inched up by 1% quarter-on-quarter (QoQ) to MYR636 mil, backed by stronger PowerSeraya contributions as well as a better Wessex Water performance post a tariff hike.

This was largely offset by widened losses from YTLP’s telecommunications arm, which resulted from lower project billings.

FY25 core earnings were weakened by a 14% year-on-year (YoY) drag due to lower PowerSeraya contributions. This was partially cushioned by improvements in Wessex Water’s performance following a price revision.

PowerSeraya’s earnings normalisation is expected to continue at a lower magnitude given that pool prices have recovered from the recent low in 3QFY25.

YTLP has expressed interest in bidding for the competitive bidding programme for new gas generation capacity and Malaysia’s first gridscale battery projects.

With its track record in operating a domestic power plant, we believe the company stands a good chance of securing new wins. Meanwhile, management guided that a portion of the first 20MW AI-DC is ready to be commercialised next month, which is a slight delay from its previous guidance.

YTLP will continue to engage with potential clients to expand its AI-DC and could take 9-12 months to build new facilities when necessary.

Additionally, we expect Wessex Water’s earnings to improve on the back of higher tariffs.—Aug 22, 2025