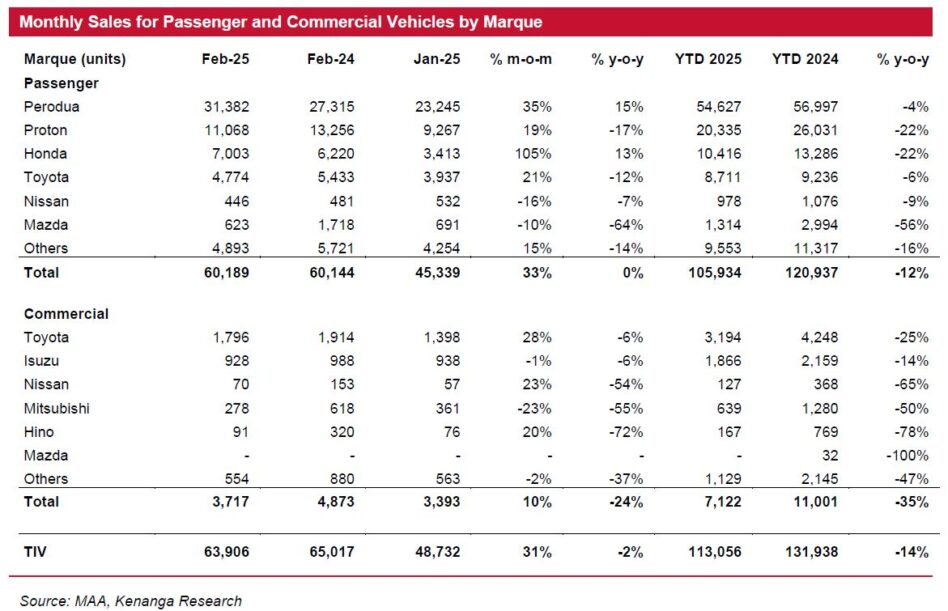

TOTAL Industry Volume (TIV) soared 31% month-on-month (MoM) on longer working month and pre-buying spree before Hari Raya Aidilfitri holidays.

But it dropped 2% year-on-year (YoY) mainly on a significant decline in commercial segment sales due to diesel subsidy rationalisation starting in June 2024 which affected the sales of lifestyle pick-up truck segment.

“Looking ahead, we believe March 2025 TIV will be higher than February 2025 TIV on major festive promotional sales before the expected scheduled plant maintenance shutdown during the Hari Raya Aidilfitri holidays,” said Kenanga Research (Kenanga) in the recent Sector Update Report.

National marques gained further ground reaping the market share from the non-national marques, especially Perodua, backed by strong sustained demand in the affordable segment, attractive new launches, and a downtrading trend by mid-market buyers.

A two-speed automotive market locally will persist into the calendar year 2025 (CY25). It will be business as usual for the affordable segment as its target customers, the B40 and lower tier M40 groups, will be spared the impact of the impending RON95 subsidy rationalisation and could also potentially benefit from the introduction of the progressive wage model.

Towards the premium segment, its target customers, the upper tier M40 and T15 groups may hold back from buying new cars, down-trade to smaller cars or switch to hybrids and EVs to cut their fuel bills upon the introduction of fuel subsidy rationalisation.

In general, the industry’s earnings visibility is still good, backed by a booking backlog of 130K units as at end-February 2025.

More than half of the backlog is made up of new models, alluding to the appeal of new models to car buyers.

This trend is likely to persist throughout CY25 given a strong line-up of new launches.

Vehicle sales will also be supported by new BEVs that enjoy SST exemption and other EV facilities incentives up until CY25 for complete build ups and CY27 for complete knockdown.

The new registration for BEVs leapt from 274 units in CY21 to over 3,400 units in CY22, 13,301 units in CY23, and 21,789 units in CY24, or 3% of TIV.

“We expect more favourable incentives from the government which has set a national target for EVs and hybrid vehicles of 20% of TIV by CY30 and 38% by CY40,” said Kenanga.

Meanwhile, the government will speed up the approval for charging stations. The number of proposed charging stations is currently at 4,299 (3,611 built to date) and this should more than double to 10,000 by end-CY25. —Mar 21, 2025

Main image: Asian Insiders