HAVING weathered through economic volatility and much challenges to funding cost in 2025, Maybank Investment Bank (MIB) expects 2026 to be an operationally more conducive year for the sector, with projected aggregate operating profit and net profit growth of 4.7%/5.0% respectively.

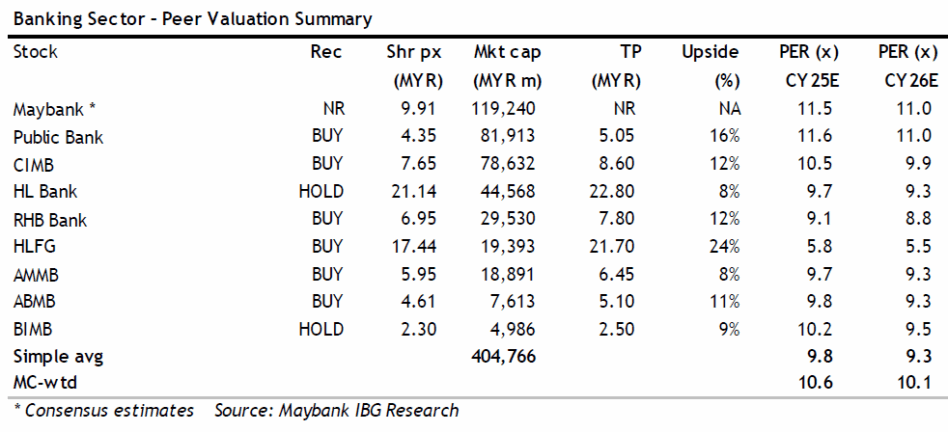

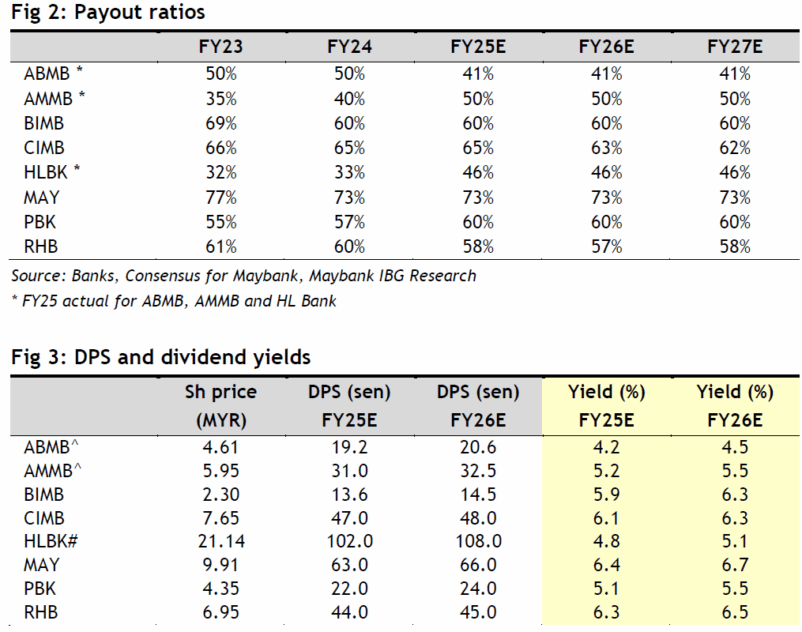

Dividend yields are decent at more than 5% for most banks, while valuations are still undemanding.

Domestic economic growth of 4.5% in 2026 supports industry loan growth of ~5%, while in the absence of further rate cuts and with easing liquidity pressure, net interest margin (NIM) is expected to be stable.

Asset quality remains impeccable, supportive of benign credit costs while management overlays provide a buffer.

“We expect an improved operating environment for CIMB’s operations amid lower NIM pressure in Singapore and a stable economic outlook in Malaysia and Indonesia,” said MIB.

Moreover, with ongoing capital returns, MIB expects special dividends to sustain dividend yields at more than 6%.

AMMB’s focus on proactive funding cost management and business banking operations should contribute to growth momentum, as it strives for higher dividend payouts.

“We expect improved earnings momentum into 2026 ABMB on lower credit costs, and project a 3-year net profit compounded annual growth rate of 7% on robust loan growth and more stable margins,” said MIB.

Asset quality has been on an improving trend and while there are pockets of stress, for instance in the retail SME segment, asset quality has generally been stable.

Absolute impaired loans contracted -3.8% year-on-year (YoY) for the 22nd consecutive month in Oct 2025 and on a year to date basis, impaired loans rose a marginal 0.3%.

“On the consumer front, we see some stress in the passenger car and credit card segments, where absolute impaired loans rose 16% YoY and 9% YoY respectively end-Oct 2025,” said MIB.

Nevertheless, the industry’s gross impaired loans (GIL) ratio remains relatively benign at 1.39% end-Sep 2025. This compares to a pre-COVID ratio of 1.51% end-Dec 2019.

The key issues plaguing the operating environment for banks in 2025 included:

a) Economic uncertainty on the global front in the earlier part of the year.

b) Fierce deposit competition coupled with a 25bp cut in the overnight policy rate in July 2025, which led to NIM compression during the year.

“Into 2026, we are more constructive on the sector, which we have upgraded to Positive from Neutral,” said MIB. —Dec 2, 2025

Main image: BusinessToday