THE banking sector, despite the presence of some headwinds, remains resilient with extremely attractive dividend yields.

MBSB Research believes the sector’s fundamental outlook remains sound, with robust earnings, manageable asset quality,large-scale recoveries, and better loan growth expected in the months ahead.

On Wednesday, the Dewan Rakyat passed the Hire Purchase (Amendment) Bill 2025, aimed at abolishing the use of flat rate and Rule of 78 for fixed-rate hire-purchase loans. The rule of 78 is a loan interest calculation method that benefits lenders by front-loading interest payments.

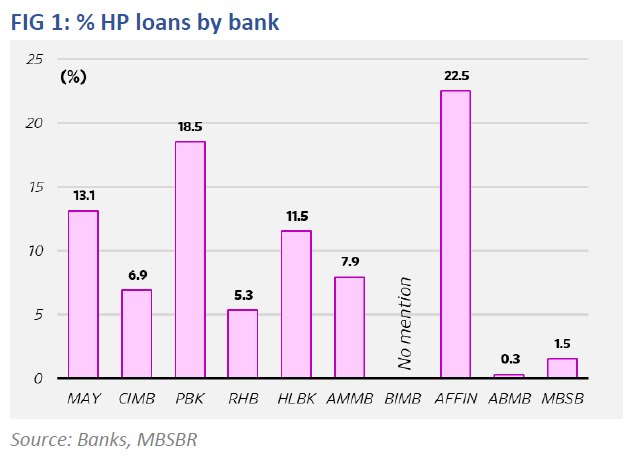

This reduces the borrowers’ savings brought about by early repayments, as the majority of interest payments are already paid within the first few years of the loan. Banks with larger hire-purchase exposure will be hit harder by this exercise, as well as credit service providers with sizeable hire-purchase exposure.

While the new ruling is good for consumers, the impact on banks will be immaterial. At first glance, the lesser interest payments to banks will likely have a negative impact. But early repayments are better for asset quality, due to the higher likelihood of full repayment. Theoretically, it could also speed up the car replacement cycle as consumers are far more likely to trade in their cars only after full loan repayment.

As it stands, roughly 30% of hire purchase borrowers settle their loans early, but only a very small proportion settle the debt before 5 years when interest charges are at the highest. Also, keep in mind that the new ruling applies to new loans, though we do not discount the possibility of banks providing some form of discount/assistance to pre-existing borrowers.

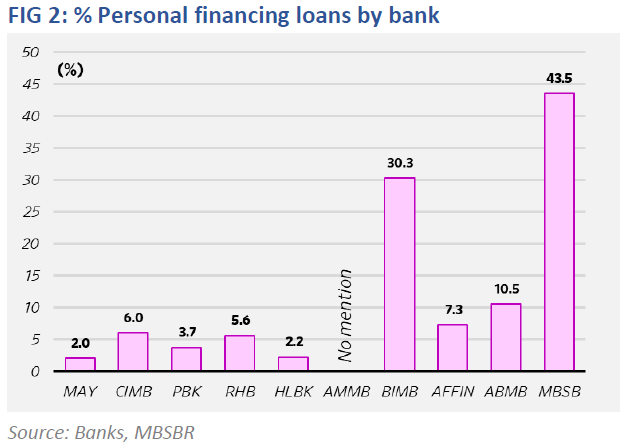

This comes hand-in-hand with Bank Negara Malaysia’s proposal to abolish the Rule of 78 for personal financing products. Aside from banks, credit service providers with sizable personal financing exposure will be impacted.

Top downside risks identified by MBSB include weaker-than-expected gross domestic product growth, which could lead to slower asset growth and asset quality issues.

Also, potential overnight policy rate cuts may compress net interest margin in the short term. Not to forget, asset quality flare-ups, which could lead to instances of heavier provisioning.—Oct 10, 2025

Main image: New Straits Times