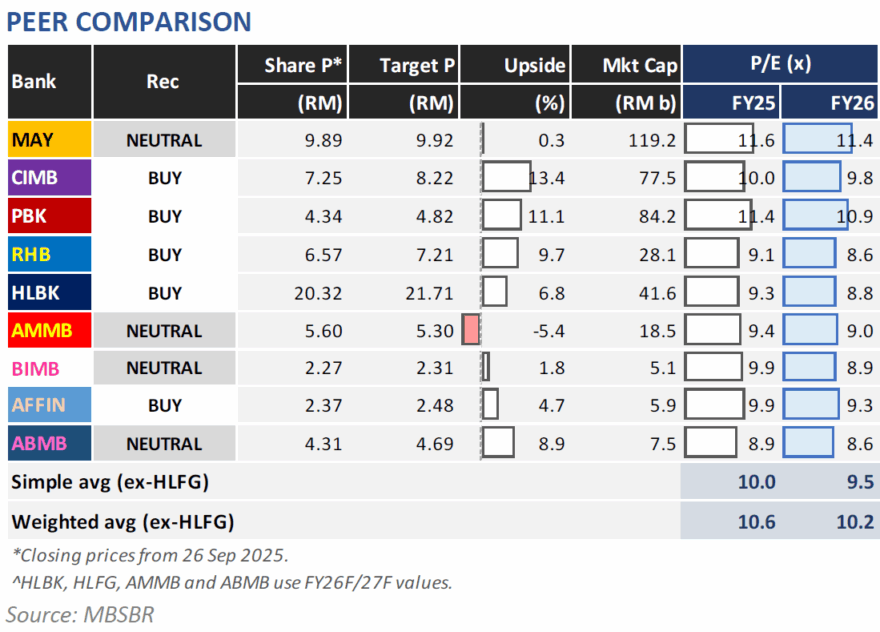

THE banking sector, despite the presence of some headwinds, remains resilient with extremely attractive dividend yields.

“We believe the sector’s fundamental outlook remains sound, with robust earnings, manageable asset quality, large scale recoveries, and better loan growth expected in the months ahead,” said MBSB Research.

Robust earnings, high dividend yields, asset quality stability, and the lack of geopolitical/political issues, especially in light of recent regional events, make the local banks look particularly attractive.

Also, MBSB mentioned that the dividend outlook is bright. Lower loan growth expectations and less skittishness over Basel III implementation lessen worries about capital.

There are hints of higher dividend payouts at year’s end. NOII to act as core topline driver in CY25.

Wealth management, bancassurance, and debt capital markets are common drivers of the fee side. Forex volatility and lowering bond yields bolster these returns.

Liquidity outlook is bright. Most banks boast elevated liquidity ratios, with space for pricier FD release or loan/deposit optimisation.

This can offset Net Interest Margin (NIM) compression in subsequent quarters. Loan growth outlook is not amazing and most banks are expecting mediocre to weak figures here.

Expanding on that, the primary market residential mortgages environment is even more competitive.

Moving forward, industry SME yields are narrowing, while problematic portfolios in several banks may dissuade strong growth in this segment.

MBSB also pointed out the occurrence of a NIM compression, a consequence of the recent OPR cut.

“Be wary that a possible further rate cut in the second half of calendar year 2025 is possible,” said MBSB.

Note that there is a mixed bag on asset quality. Some banks saw a spike this quarter, spooking investors. Others managed this very well.

Regardless, the consensus is that there will be some normalisation in the second half of calendar year 2025, and large recoveries are expected in select banks.

Also, MBSB said there is a mixed bag on provisioning, though upside risk is greater. Most banks have already issued large overlays.

“Hence, we are not expecting too many further incidents of higher provisioning. Concurrently, multiple banks are gearing up for large-scale writebacks, implying a lighter second half of 2025,” said MBSB. —Sept 29, 2025

Main image: The Malaysian Reserve