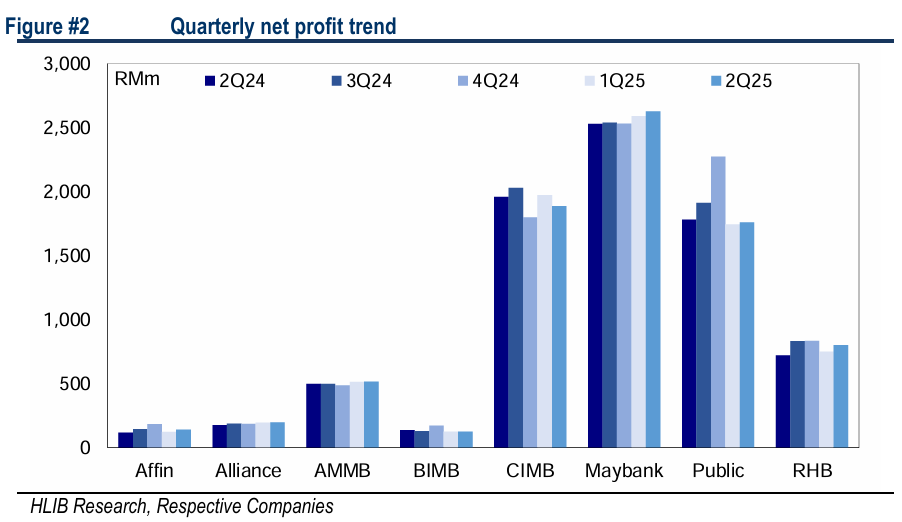

QUARTER two 2025 (2Q25) sector profit came in flat as positive Jaws was largely offset by higher loan loss allowances.

At the top, the expansion was led by non-interest income (NOII), thanks to strong trading-related performance. However, net interest margin (NIM) saw a 2 basis points (bp) downtick.

Notable outperformers were Affin and RHB, while CIMB underperformed.

Again, total income growth was a key driver lifting sector earnings up 2%. That said, the financial performance could have been better if not for the 30% jump in bad loans provision.

Positive outliers were Affin, Alliance, and RHB. However, BIMB saw an 8% bottom-line drop given higher operating expenses (opex), impaired financing allowances, along with finance cost.

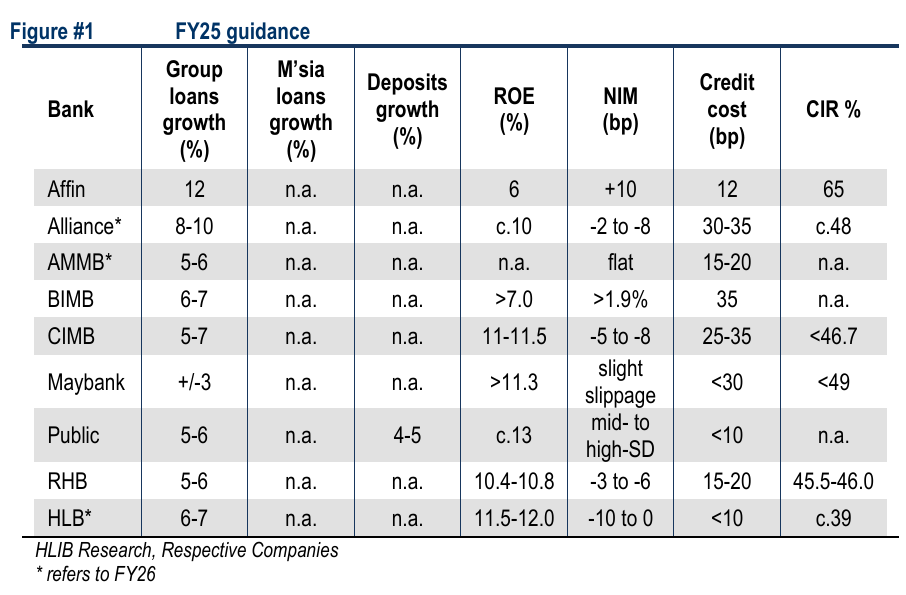

Headline loans growth tapered to +3.4% year-on-year (YoY) due to forex softness, but on an adjusted basis, it would have stayed fairly resilient while deposits gained momentum to +4.7% YoY.

From these two categories, the top 3 quickest growing banks were Affin, Alliance, and BIMB. As for asset quality, GIL ratio rose 4bp sequentially to 1.51% due to larger NPL formation.

We expect NIM to compress in 3Q25 given Jul-25 overnight policy rate cut.

However, banks can look to mitigate the impact through optimising their loan-to-fund ratio and possibly prune some pricey FD. Also, selective lending strategy could help to preserve NIM but loans growth may moderate.

Besides, the built up in fair value through other comprehensive income (FVOCI) reserve provide banks the flexibility to crystalize investment gains, making it an earnings buffer during periods of softness.

As for asset quality, we do not expect any major cracks under our base-case but we stay watchful for potential downside risk; in our view, the gradual improvement in business sentiment should help to sustain credit resilience.

We remain constructive on the banking sector, underpinned by inexpensive valuations, alongside an appealing 5% dividend yield.

Also, KLFIN has underperformed the KLCI, leaving space for catch-up, while its large-cap stature positions it as prime beneficiary of eventual foreign buying from EM rotational play.

Against this backdrop, we view the sector’s risk-reward as favourable and advocate a broad-based accumulation strategy. —Sept 10, 2025

Main image: New Straits Times