FOLLOWING the Regulatory Period 4 (2025-2027) announcement, we believe major key themes, that is the grid infrastructure upgrade cycle, domestic renewables capacity ramp-up, and experienced independent power producers (IPPs) bridging the supply gap will continue to play out amidst the implementation of NETR.

The renewable energy (RE) subsector introduction offers investors with clearer access to opportunities, while RE companies could benefit from increased visibility and funding potential for sustainable development.

“We believe the base tariff 45.62 sen/kWh which will be implemented starting 2H25 would have factored in an average 3-year demand growth of 4-5%,” said RHB in the recent Malaysia Sector Update Report.

The contingent capital expenditure (capex), in RHB’s view, will be entitled for the same regulatory return of 7.3% and to be included into RAB.

The 3- year planned contingent capex is mainly to cater for potential additional demand (such as data centres) and energy transition-related projects.

The list of projects under contingent capex has been pre-approved by the Energy Commission (EC) and will be implemented once the trigger occurs.

“We see an upside of 5-7% to our net regulatory returns if the full capex numbers are being pencilled in,” said RHB.

“We see an upside of 5-7% to our net regulatory returns if the full capex numbers are being pencilled in,” said RHB.

This somewhat demonstrates that TNB is able to capitalise on the potential upside if electricity demand comes in stronger than what has been imputed in base tariffs.

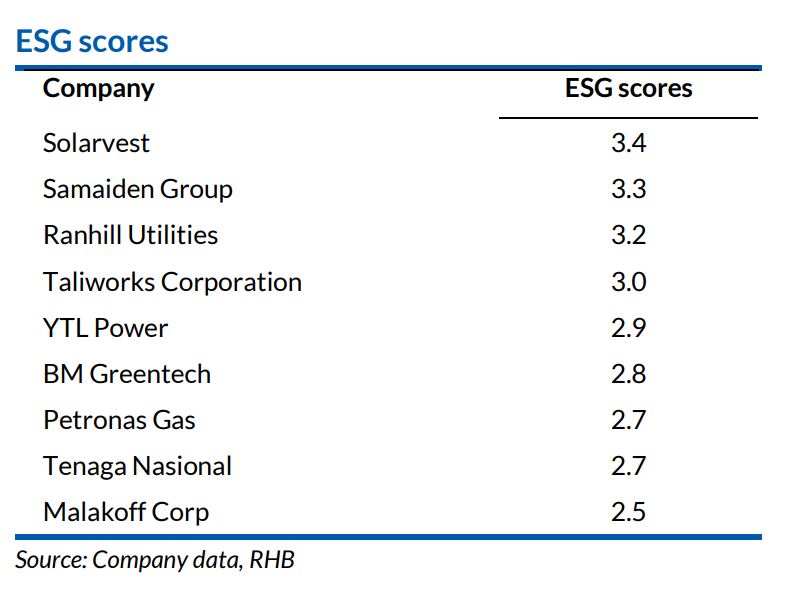

Bursa Malaysia has launched a new subsector, reclassifying 13 companies effective 13 Jan 2025 – highlighting the growing prominence of RE.

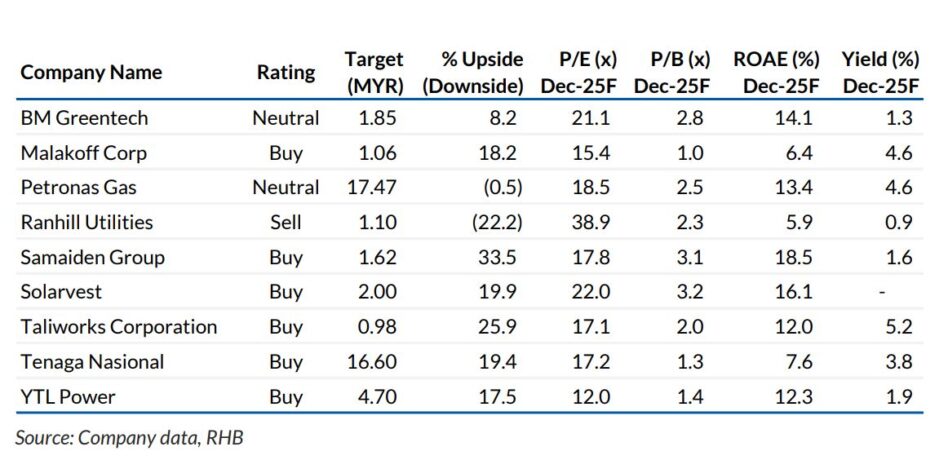

Excluding Cypark, which is an outlier with a price-earnings (P/E) ratio of 86x due to its turnaround expectations, the financial year 2025 P/E for the group ranges between 10-23x.

Mega First Corporation’s (MFCB) low valuation reflects its asset owner focus.

Solar EPCC players are valued at a premium due to Malaysia’s RE growth plans targeting a 70% mix by 2050.

Share prices for the companies under the sub sector have mostly shown strong three-year returns, driven by sector recovery post Large Scale Solar 4 (LSS4) overhang and initiatives like National Energy Transition Roadmap (NETR), Corporate Green Power Programme (CGPP), and Large Scale Solar 5 (LSS5).

Shortlisted bidders were notified on 23 Dec 2024, and companies have since begun announcing their awarded quotas, with more announcements anticipated.

EPCC contracts, estimated at MYR7 bil, are expected to be awarded in the second half of 2025, providing a strong pipeline of opportunities for solar contractors.

This will ensure orderbook replenishment following the expected completion of most CGPP projects by the end of 2025. —Jan 14, 2025

Main image: New Straits Times