RHB foresees the consumer product sector outlook improving in 2026, premised on favourable fiscal policy, namely the higher SARA handouts which translates to stronger earnings growth whilst the inclusive petrol subsidy rationalisation has removed a major overhang.

Overnight policy rate cuts, stronger MYR, and robust tourist arrivals are also other positive catalysts. The sector will continue providing a defensive shelter by offering earnings visibility amidst the uncertain global macroeconomic outlook thanks to the domestic-centric earnings base and resilient consumption.

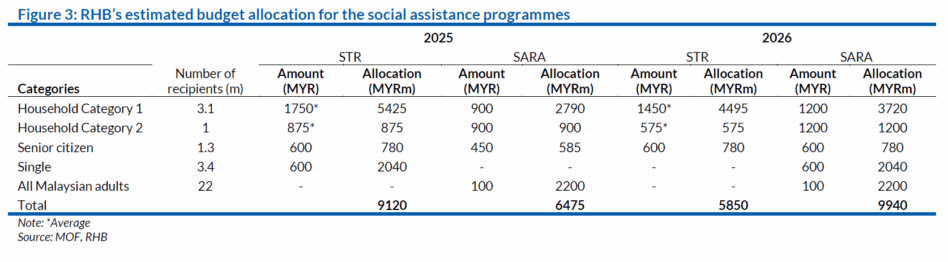

“Although the budget allocation for key social assistance programmes – Rahmah Cash Contribution (STR) and Basic Rahmah Contribution (SARA) has remained at MYR15 bil in Budget 2026, we notice an increased allocation for SARA at the expense of STR,” said RHB.

The shift is positive to the sector by directing more spending onto grocery and daily necessities, hence, effectively translating to better sales volume for large-cap consumer staple companies, particularly Nestle and 99 Speed Mart.

“Our observation suggests both are garnering strong market share under the SARA programme,” said RHB.

The depressed consumer sentiment in quarter two of 2025 (2Q25) should normalise post the US tariff clarity and stimulus packages announced in July. Meanwhile, the initial stage of petrol subsidy rationalisation is positive as all citizens are entitled, on top of a 6 sen/litre reduction in pump price.

This is a major relief to the sector considering the potential inflationary impact if a more exclusive retargeting approach was adopted. Lower interest rates, stronger MYR and tame inflation would be other drivers to support consumer sentiment and spending going forward.

Whilst we acknowledge that the sector’s exposure to tourism is minor, a pickup in tourist arrivals and tourism receipts as a result of a successful Visit Malaysia Year 2026 (VMY2026) campaign will lead to positive multiplier effects, more robust economic activities and consumer spending.

Given the visible catalysts of a higher SARA handout and normalising sentiment toward Nestle brands, we continue to like 99 Speed Mart and Nestle. We highlight Mynews and the brewery duo as our picks under VMY2026.

Moreover, we believe the excise duty hike is already in the price with the valuation and dividend yields looking attractive. Risks to RHB’s recommendations are slower-than-expected economic growth, higher-than-expected inflation and sharp spikes in commodity prices. —Oct 17, 2025

Main image: Grocery Dive