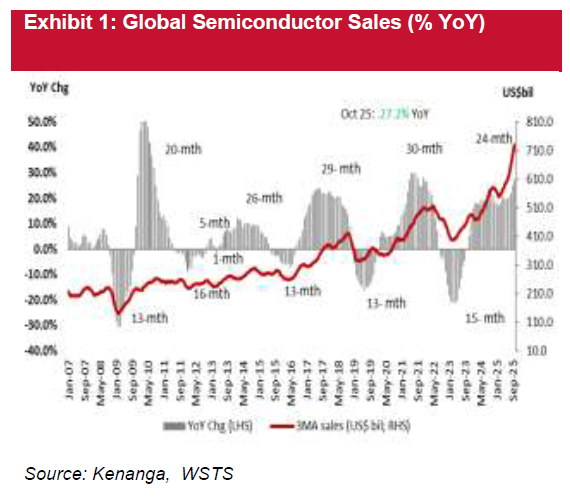

GLOBAL semiconductor cycle still has runway with market nearing USD1t by 2026 led by Logic/Memory.

WSTS lifted its 2025 forecast to +22% YoY (USD772 bil) and expects more than 25% growth in 2026 (USD975 bil), driven by AI-related demand and continued data-centre investment, with Logic and Memory leading again.

This reinforces Kenanga’s overweight view since last quarter where the current 24-month up-cycle could plausibly extend into mid-calendar year 2026 (CY26) or beyond, consistent with historical cycle duration and the structural AI/HPC upgrade cycle.

Front-end (WFE) remains a key anchor for 2026 with capital expenditure cycle looking early rather than late. SEMI projects WFE to rise to USD116 bil in 2025 (+6%) and USD125 bil in 2026 (+8%), led by foundry/logic and an acceleration in memory equipment.

Importantly, tool spend has yet to fully reflect the scale of fab announcements, implying the equipment upturn may have further room to broaden as 2nm/GAA/backside power and HBM/DDR5 transitions progress.

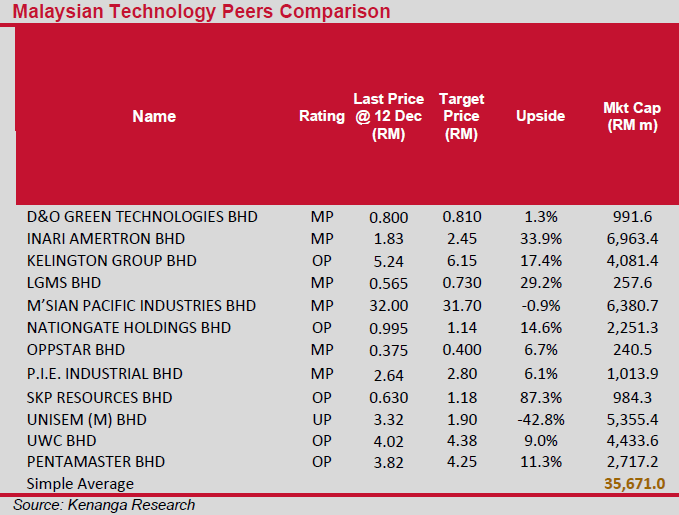

For Malaysia’s front-end ecosystem, this constructive trajectory should translate to better prospects for local beneficiaries where KGB is leveraged to sustain activity in UHP process gas systems, chemical delivery networks and tool hook-ups, while UWC is positioned to gain from rising demand for precision modules and systems integration for wafer-fab tools.

Historically, such cycles support stronger order intake, a deeper tender pipeline, higher utilisation and improved revenue visibility across the segment.

Bloomberg highlights that large, interconnected funding and procurement arrangements can effectively lock in GPU demand and fund outsized capex, further reinforcing Nvidia’s dominance at the centre of the AI build-out.

However, with several players still cash-burning and revenue scaling lagging expenditure, any shortfall in AI adoption or returns could quickly ripple through closely linked counterparties such as cloud providers, hyperscalers, AI labs and semiconductor suppliers, amplifying downside and heightening the risk of valuation de-rating. —Dec 19, 2025

Main image: Open Gov