DESPITE EXPECTATIONS of weaker upstream earnings both quarter-on-quarter (QoQ) and year-on-year (YoY) in the upcoming results season beginning May 7, 2026, overall performances are still expected to come largely in line with our forecasts, aided by firmer crude palm oil (CPO) prices.

Plantation companies are likely to report softer upstream earnings in 1Q26 on a sequential basis, mainly due to seasonally lower harvesting activity and weaker palm product prices during the quarter, said Hong Leong Investment Bank.

On the downstream side, results are expected to show improvement compared with the previous quarter.

This should be supported by a smaller gap in export taxes and levies between Malaysia and Indonesia, alongside lower palm kernel (PK) prices, although operators continue to face margin pressure from persistent industry overcapacity.

Compared with the same period last year, upstream earnings are also projected to decline, weighed down by softer palm product prices and rising production costs, particularly from higher fertiliser expenses, despite mixed fresh fruit bunch (FFB) production trends.

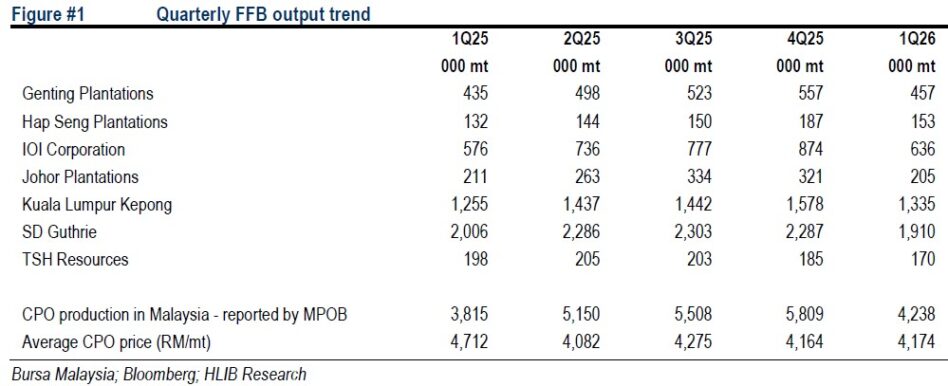

Although Malaysia recorded a solid 11.1% rise in FFB output, production performance across listed planters remained uneven, with three out of the seven companies under our coverage posting YoY declines.

We attribute this largely to unfavourable weather conditions in certain parts of Indonesia, which affected harvesting operations and disrupted crop transportation for plantation groups with exposure there.

Meanwhile, downstream operations are likely to post better YoY results, thanks to the narrower export tax and levy differential between Malaysia and Indonesia, as well as lower PK prices, even as structural industry challenges remain.

We maintain an Overweight call on the plantation sector, supported by near-term strength in CPO prices, which continues to benefit from elevated crude oil prices.

That said, we believe the current positive cycle could be concentrated in the near term, with medium-term downside risks stemming from potential supply adjustments in competing vegetable oil markets.

For investors seeking targeted exposure, we continue to favour pure upstream plantation players that have already secured fertiliser costs for the year, offering stronger earnings visibility and margin protection, including JPG and SDG. —May 5, 2026

Main image: WWF