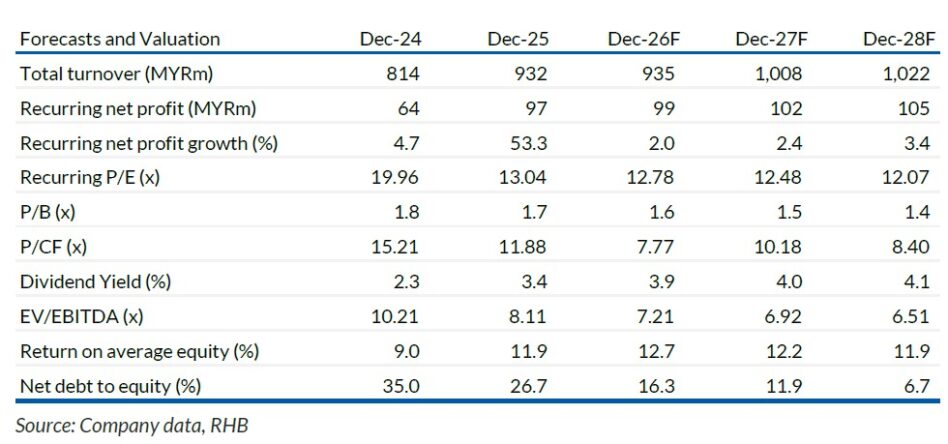

DUPPHARMA BIOTECH’S results beat expectations at 32% and 30% of RHB and consensus’ estimates.

“While we turn more cautious on the margin outlook for future approved products purchase list (APPL) contracts amid rising active pharmaceutical ingredient (API) and operating costs, we believe current valuations remain attractive,” said RHB.

Quarter one 2026 (1Q26) core net profit grew 22% to MYR31.1 mil, despite a 6% year-on-year (YoY) decline in revenue, as the strong consumer healthcare business partially offset weaker public sector sales (recall that the first half of 2025 saw a surge in insulin sales worth MYR30-35 mil).

Gross profit margin (GPM) expanded by 3.7ppts year-on-year (YoY), supported by a stronger MYR, lower API costs, and a more favourable product mix.

“Sequentially, however, margins softened, with local segment GPM remaining above 40%, while exports margins fell to 23.9%,” said RHB.

Lower admin expenses and net finance costs also helped bottomline growth.

RHB expects YoY growth in 2Q26 to be driven by peak demand in the final year of the APPL tender cycle (2024-2026); and resilient margins, supported by a stronger MYR and DBB’s 3-6 month API inventory buffer, which should cushion the impact of gradually rising API prices in the near term.

The MYR65.1 mil insulin contract awarded on 19 Feb should provide a meaningful boost to 2Q26 topline, despite its 3-month duration through 15 May, as its value is comparable to that of a typical 6-month contract.

Health Minister Datuk Seri Dzulkefly Ahmad said medicine prices should remain stable this year as manufacturers continue absorbing higher production and logistics costs from higher fuel prices.

That said, amid the current weak USD environment and rising API and operating costs, we turn more cautious on the pricing dynamics of upcoming APPL contracts, as there may be limited room for cost pass-through if cost pressures intensify post award.

Key downside risks identified by RHB are such as the lower-than-expected sales volumes, USD strengthening against the MYR, and higher-than-expected operating costs. —May 15, 2026

Main image: Dagang News