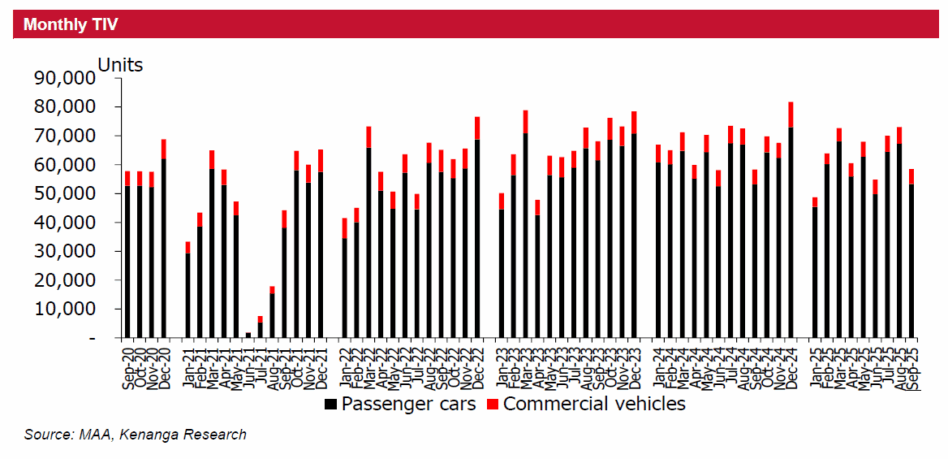

SEPTEMBER total industry volume (TIV) decreased by 20% month-on-month (MoM) due to shorter working days (four public holidays for the month), and scheduled plant maintenance shutdown by Perodua for a week in preparation to boost production volume for the year-end sales.

Meanwhile, TIV came in flat year-on-year (YoY) mainly due to the shifting of new models launched towards the quarter four (4Q) by Perodua and other Japanese marques.

“With the nine months calendar year 2025 (9MCY25) TIV making up 72% of our full-year projection of 805k units (-2% YoY), we consider the number as meeting our expectation,” said Kenanga.

In comparison, 9MCY24 made up 73% of full-year 2024 TIV. Their CY25 TIV projection is a tad above the forecast of 780k (-4.4% YoY) by the Malaysian Automotive Association (MAA).

This is backed by strong sustained demand in the affordable segment, fuel subsidies being expanded to all Malaysians, attractive new launches, and forward buying interest on the deferment of new excise duty regulations and ending of EV imported CBU incentives by end-2025 in which they expect Perodua to benefit the most due to higher localisation rate, and expected launch of Perodua EV local assembly by year-end.

“Looking ahead, we believe October 2025 TIV will be much higher than September 2025 due to longer working days, absence of plant maintenance shutdown and attractive year-end promotional campaign,” said Kenanga.

Moreover, the ending of electric vehicle (EV) imported complete build up (CBU) incentives by year-end is also expected to boost EV sales as EV importers look to clear stocks with huge promotional discounts.

National marques stood their ground, wrestling share from the non-national marques. This was seen in Perodua, backed by strong sustained demand in the affordable segment and attractive new launches.

In the non-national marques, Mazda suffered the most due to slower new launches, being affected by intense competition from Chinese marques.

For the month of September 2025, Chery took 3rd place (7% of non-national TIV share), while BYD fell to 4th place (6% of non-national TIV share) which we believe was due to dilution of the EV market share (Chery sold more ICE vehicles as BYD still focuses on EV) as more EV brands entered the market. Note the iCaur, launched recently in August and Proton e.Mas 7 which maintained its top selling EV position. —Oct 22, 2025

Main image: TRENDS Research & Advisory