ENERGY REMAINS an appealing defensive play if tensions in the Middle East drag on and push markets into a risk-off stance.

Large-cap utilities such as Tenaga Nasional Berhad and Petronas Gas Berhad are relatively insulated from external shocks, given their limited exposure to overseas operations, foreign exchange volatility, and fuel cost fluctuations.

Their regulated structures also underpin steady earnings, typically offering dividend yields in the 4–5% range.

YTL Power International could benefit from any uptick in gas prices. Meanwhile, higher energy costs have had little impact on Tenaga Nasional and other power producers, as these are largely passed through to consumers via the Automatic Fuel Adjustment (AFA) mechanism.

Since the AFA was introduced last July, the government has consistently approved rebates, supported by a stronger ringgit against the US dollar and softer gas prices.

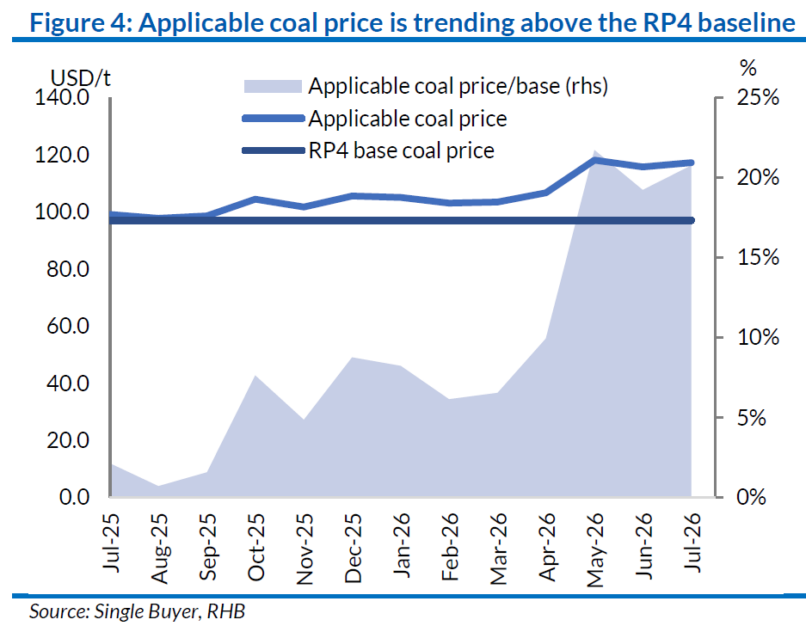

Based on prevailing coal and gas prices, the government is forecasting a 0.08sen AFA surcharge in July (vs the 0.47sen rebate currently).

The adjustment mainly reflects a higher Tier-2 gas price, mitigated by a stronger MYR and lower Tier-1 subsidised gas price.

Nevertheless, the effective tariff impact should be minimal, that is,1% higher vs current prices.

The impact of higher gas prices is minimal on the power sector, as unsubsidised gas (the most correlated to Brent crude) only makes up 9% of total generation fuel costs in Malaysia.

RHB estimates a 8-9% year-on-year earnings growth for TNB in the coming quarter, on a lower tax rate and higher regulated revenue contributions.

“We expect regulated capital expenditure recognition to grow by 10-11% on accelerated contingency project approvals,” said RHB.

RHB foresee YTLP recognising a MYR33 mil share of losses for its stake in Digital Nasional, but this should be mitigated by stronger contributions from its water and data centre businesses.

Meanwhile, Solarvest’s and Samaiden’s earnings should grow, on higher recognition of their solar projects. Elsewhere, the postponement of the implementation of the carbon tax allows more time for corporations to reduce their carbon emissions.

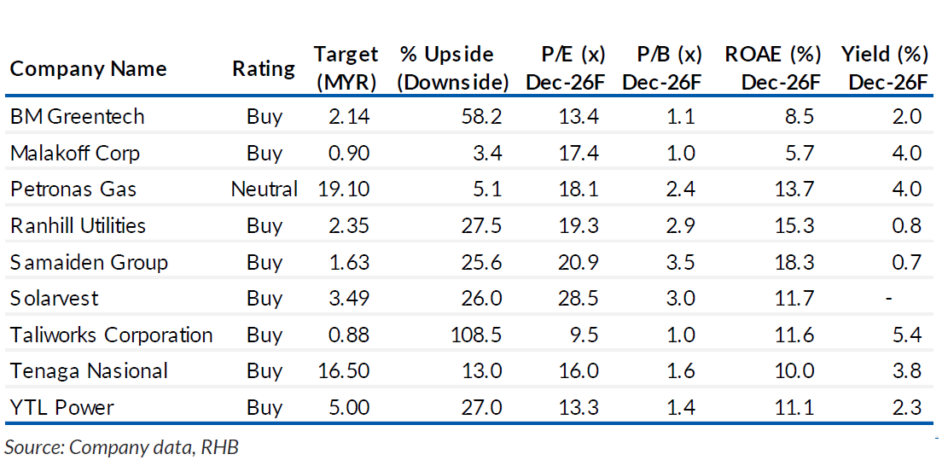

“TNB remains our main Top Pick as it is the prime beneficiary of the National Energy Transition Roadmap (NETR), with the regulated framework providing a stable earnings base,” said RHB.

RHB also likes YTLP and PTG in a risk-off environment. They encourage investors to accumulate Solarvest and Samaiden shares following recent price corrections, as RHB sees a minimal impact from the removal of the export value-added tax rebate on solar players. —Apr 27, 2026

Main image: energyventures.in