GAMUDA’S latest quarterly results underscore the strength of its engineering business, with a record order book and improving earnings offsetting softer property sales.

Its quarter three 2026 net profit rose 12% quarter-on-quarter (QoQ) to RM258.0 mil, despite a marginal 2% uptick in revenue.

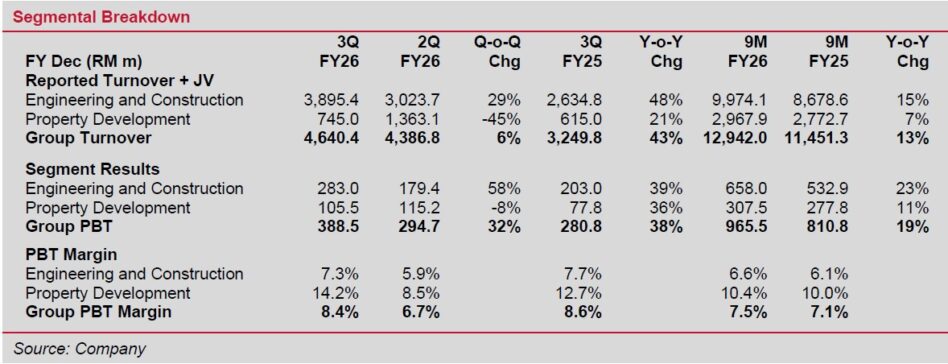

Conversely, Gamuda Land (GL) reported a 45% decline in revenue following exceptionally strong contributions from Vietnamese Quick-turnaround Projects in quarter two 2026.

Nonetheless, GL’s profit before tax margin expanded to 14.2% (from 8.5%), largely due to project recognition timing.

Gamuda Engineering (GE) secured projects worth RM11.7 bil over the past two months alone, lifting its outstanding order book to a record RM52 bil.

Structurally, 75% of these projects are in early mobilization/procurement stages, 16% are commencing main works, and 9% are at peak execution.

This back-ended profile ensures an accelerating revenue ramp-up in the coming quarters, placing the group on track for a new structural earnings growth cycle from 2027 onward.

GL posted 9MFY26 property sales of RM2.1b (down 16% YoY from RM2.5b), primarily due to fewer launches in Vietnam.

Specifically, only one Eaton Park tower was launched this year compared to four towers last year, while key Hanoi launches were pushed into 2027 due to regulatory approval timings.

Consequently, management has revised its 2026 sales target downward to RM4.0 bil (from RM4.5 bil).

For 2027, GL plans a massive RM12.7 bil GDV launch pipeline, heavily anchored by Vietnam (46%), Singapore (29%), and Malaysia (25%).

“We continue to like GAMUDA for its strong positioning in upcoming data centre tenders, its ability to secure overseas projects, and its robust earnings visibility underpinned by a record outstanding order book of RM45.9 bil,” said Kenanga, maintaining Outperform for GAMUDA. —June 26, 2026

Main image: Berita Harian