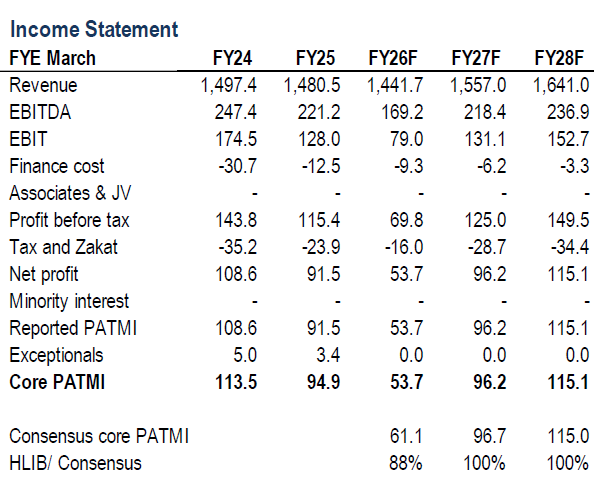

THE quarter three financial year 2026 (3QFY26) core profit after tax (PAT) for SAM Engineering & Equipment (SAMEE) came in at RM12.4 mil or -66% year-on-year (YoY), tracking at just 61%/64% of Hong Leong Investment Bank (HLIB) and consensus full-year forecasts.

The Equipment segment again underperformed already-muted expectations and remained a drag on overall results, with additional pressure coming from forex headwinds.

Non-core adjustments in the nine months of financial year 2026 (9MFY26) include fair value loss on derivatives (+RM1.3 mil) and forex gains (-RM2.6 mil).

3QFY26 revenue dipped 1% quarter-on-quarter (QoQ) to RM360 mil, as a 4% decline in Equipment sales was partly offset by a 4% increase in Aerospace.

Overall, 9MFY26 revenue slipped 2% YoY to RM1.09 bil, while core PAT fell more sharply by 43% YoY to RM39.5 mil. The earnings contraction was driven by an unfavourable mix shift and forex headwinds.

Aerospace segment momentum remains clear, underpinned by higher aircraft deliveries expected in 2026. Optimistically, margin expansion should follow once the ongoing relocation of Singapore-to-Thailand operations is completed.

As per its previous update, the new BB2 plant is currently in qualification and is on track for full production in quarter one of calendar year 2026 (1QCY26).

SAMEE previously highlighted several initiatives expected to ramp up in FY27, including:

i) adding two new non-US front-end (FE) customers.

ii) recovery in the HDD business.

iii) securing high-power system-level test equipment.

“In our view, these developments remain nascent and will likely take some time to translate into earnings.,” said HLIB. Equipment segment weakness is largely in line with guidance from SAMEE’s US-based FE customer, which expects softer sales through the first half of calendar year 2026 (1HCY26) due to tighter US export controls on China, followed by a recovery in 2HCY26.

“That said, we think there could be risks that SAMEE may be disproportionately impacted by the weaker China sales in the near term and may not capture the upside from robust WFE spending globally,” said HLIB.

This will be a key focus heading into SAMEE’s analyst briefing on 12 Feb, together with its key US customer results later that day.

SAMEE’s medium-to-long-term growth is underpinned by customer diversification, ongoing capacity expansion in Thailand, and progress in securing long-term aerospace and FE opportunities.

Nonetheless, near-term earnings are likely to remain muted due to flattish FE equipment demand, transitional costs in the aerospace segment, and margin pressure from a weaker USD. —Feb 11, 2025

Main image: SAM Engineering