THE GLOBAL semiconductor cycle remains firm, with industry sales still accelerating and the market on track to approach US$1t by 2026.

The semiconductor industry is navigating a high-stakes paradox in 2026. While soaring artificial intelligence-driven demand is pushing revenues to unprecedented levels, this boom has its risks.

“The industry seems to have placed all its eggs in the AI basket, which may be fine if the AI boom continues. But the industry should also consider planning for scenarios in which AI demand slows or shrinks,” said Deloitte Center for Technology, Media & Telecommunications regarding the global market.

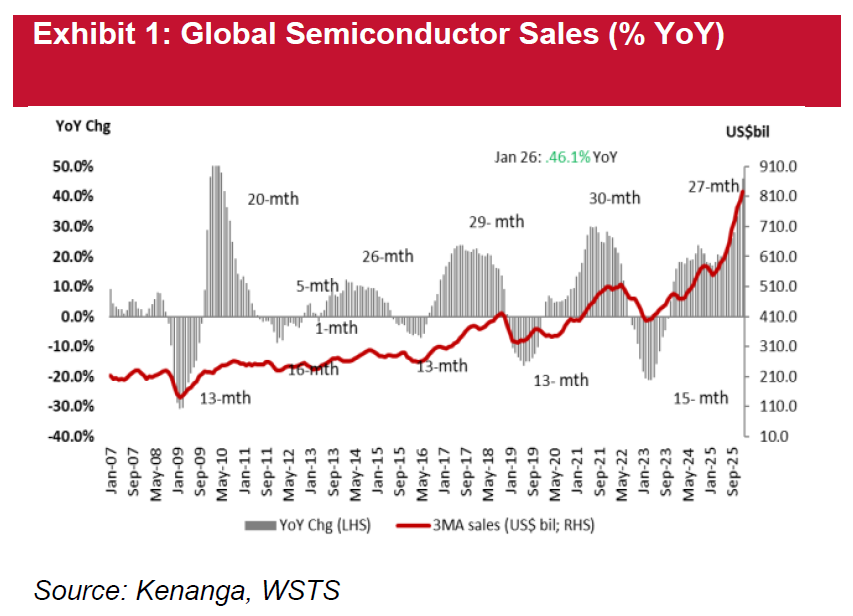

Locally, January 2026 sales rose 3.7% month-on-month (MoM) and 46.1% year-on-year (YoY) to USD83.7 bil, while WSTS expects the market to grow by more than 25% in 2026 to USD975 bil, led by continued strength in Logic and Memory.

Unlike previous cycles, this upturn has been supported by more structural drivers, including AI, HPC, 5G and next-generation device upgrades, which should help extend the cycle, although the benefits are becoming increasingly uneven across the sector.

AI workloads are significantly more memory-intensive, prompting suppliers to prioritize HBM and high-capacity DDR5 for AI servers over conventional DRAM and NAND for smartphones, PCs, vehicles and other consumer devices.

This has created a zero-sum environment, where hyperscalers and AI server customers are absorbing a disproportionate share of industry output, while non-AI end-markets face tighter supply, higher costs and weaker affordability.

IDC has sharply cut its 2026 smartphone shipment forecast, while Gartner now expects global PC shipments to experience a double-digit decline, both citing surging memory costs.

In short, the AI build-out is no longer only lifting demand for AI infrastructure, but is also pushing up input costs across the broader electronics chain, which could squeeze margins, weaken affordability and place structural pressure on lower-end devices.

Against this backdrop, memory is emerging as the clear leader of the next wafer fabrication equipment (WFE) upcycle.

“We expect memory WFE to have grown 13% in 2025 followed by 23% in 2026, before moderating to 9% in 2027, making it the strongest growth segment across semiconductors,” said Kenanga.

This reflects the highly equipment-intensive migration in 3D NAND and DRAM; Kenanga estimates memory will account for roughly 65%–70% of total WFE capital expenditure over 2024–2027.

By comparison, logic spending should recover more gradually, supported by continued migration towards 3nm-class and sub-3nm nodes.

Downgrade the sector rating to NEUTRAL from OVERWEIGHT as external risks have intensified, particularly from global memory tightness, supply-chain fragility and persistent cost pressure across the value chain. —Mar 27, 2026

Main image: pexels.com