FOR years, Kinergy Advancement Bhd (formerly Kejuruteraan Asastera Bhd) was viewed primarily as an engineering business.

That foundation remains relevant but the group’s FY2025 suggests the more important story has moved elsewhere. It suggests that such overdue framework is ripe for revision.

The group has crossed into energy ownership, infrastructure development and long-tenure revenue structures that its engineering heritage neither predicted nor priced in.

Investors who are still applying an engineering multiple to Kinergy’s earnings may be looking at the right numbers through the wrong lens.

Kinergy’s share price has begun reflecting some of this interest. Recent stock screeners showed the counter trading around 38.5 sen, close to the upper half of its 52-week range of 30.5 sen to 42 sen with a market capitalisation of about RM841 mil.

Even so, the group remains a sub-RM1 bil energy counter at a time when its exposure has expanded from project execution into energy assets and power infrastructure.

FY2025 provides clearer evidence of that shift. The group’s revenue rose 117.4% year-on-year (yoy) to RM478.3 mil, closing in on the half-billion-ringgit mark. Its net earnings stood at RM27.9 mil while earnings per share came in at 1.31 sen.

Value creation journey

The more telling figure lies in the revenue mix. Kinergy’s Sustainable Energy Solutions (SES) segment generated RM328.2 mil in revenue, up 207.5% yoy and accounted for 69% of group revenue compared with 49% in FY2024. Its engineering revenue stood at RM148.7 mil.

Kinergy’s founder and group managing director Datuk Lai Keng Onn acknowledged how the group is today operating with a risk profile that is seemingly different from the day when the group was initially listed in the ACE Market of Bursa Malaysia on Nov 17, 2017.

Editor’s Note: The group then an electrical and mechanical engineering entity was transferred to the Main Market of Bursa Malaysia on Aug 28, 2020.

“The business we’ve entered requires more capital, more patience and more disciplined governance than an engineering contract demands,” revealed Lai who is also Kinergy’s executive deputy chairman.

“We entered this with clear intent – making a deliberate shift beyond a traditional project-delivery model and the limitations of an engineering contract cycle. As this portfolio continues to take shape, SES has now emerged as a significant growth pillar, serving as a key differentiator in the group’s value creation journey.”

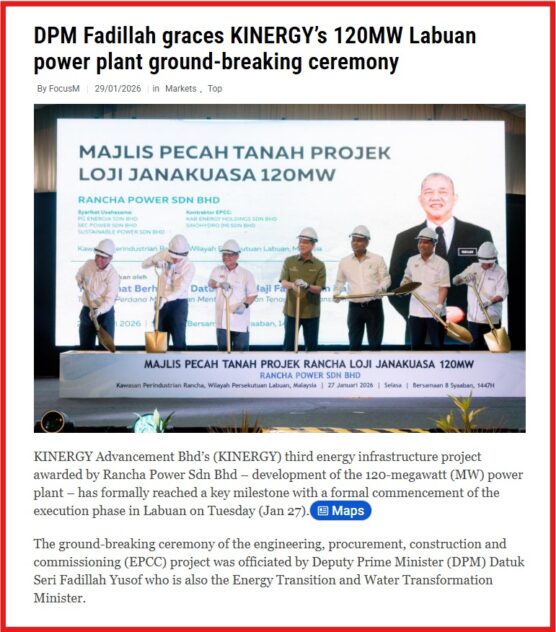

The RM646.32 mil Labuan 120MW gas engine power plant is one example. It is Kinergy’s largest EPCC contract to date and its third major project involving PETRONAS linked entities.

The project supports Labuan and the wider Sabah power system by mitigating electricity supply intermittency through the provision of reliable baseload capacity.

Befitting national agenda

In fact, the key catalyst for the company in 2025 lies in the potential development of the Perlis project.

Kinergy has secured a position as the leading consortium member for the proposed Teknologi Tenaga Perlis Consortium (TTPC) gigawatt-scale gas-fired new development.

This also signals to the market the company’s entry into another strategic position, opening a new avenue for its growth as an independent power producer (IPP).

Scaling an IPP model is not without its capital implications. As Kinergy deepens its asset ownership position, payback horizons lengthen and capital requirements intensify, the reality is such that these are known trade-offs of asset ownership and shareholders are right to hold them in view.

The TTPC acquisition, however, is structured around a starting position that changes the risk calculus. Existing transmission inter-connection, gas supply infrastructure and water facilities mean that the development path begins mid-journey rather than at the ground.

That brownfield foundation does not eliminate execution risk but it meaningfully reduces the timeline and capital intensity of what would otherwise be a full greenfield power project.

Seen in that context, the Perlis project is not simply an IPP ambition of the company. It fits into the national need for firm, dispatchable capacity while Malaysia adds more sustainable energy into the grid.

While other renewables will remain important, the integrity of any power system rests on the availability of stable, always-on capacity – particularly as demand complexity and grid interdependency grow.

SES to propel future ventures

Among renewable sources, not all capacity is equal. Solar dominates Malaysia’s corporate renewable market but it cannot guarantee supply when there are clouds cover the panels. Mini hydropower can.

Run-of-river mini hydro schemes generate consistent electricity from river flow without dams, without reservoirs and without weather dependency, hence able to deliver the baseload reliability that corporate energy users with continuous operations cannot compromise on.

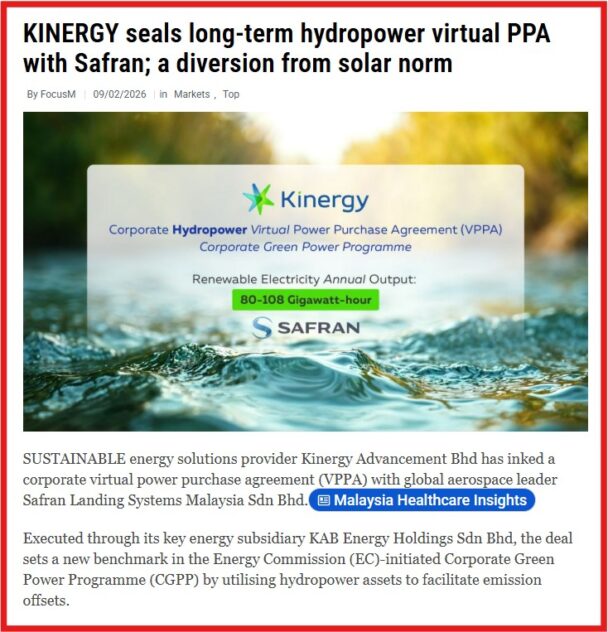

Kinergy’s 21-year virtual power purchase agreement (VPPA) with Safran Landing Systems Malaysia which required hydropower-backed output of 80GWh to 108GWh per year is built on this quality.

With the formalisation of this recent agreement, the group has expanded its SES role in realising national policy aspirations by converting complex energy mechanisms into commercial reality.

Taken together, these developments point to a company in deliberate transition. Kinergy is scaling in phase, accepting capital intensity and margin variability as the known costs of building something more durable than a project pipeline.

The re-positioning is real and it is material. Markets rarely award the full multiple before the model is proven but the evidence is building that the model is working – and it is now waiting for the market to agree.

“Our growth has always been measured against the risk it introduces and the complexity it demands – and we’ve held to that standard even when moving faster would have been easier,” envisages Lai.

The risk we carry today is real and proportionate to what we are building. Certainly, the market takes time to reprice businesses that have genuinely changed category. We understand that.

We’re patient. And we’re confident that the evidence continues to accumulate as our business model becomes clearer overtime – and we believe it is no longer a question of whether but a question of when.

Kinergy ended its FY2025 with a secured order book of RM1.0 bil and an active tender pipeline of RM2.2 bil which together provided the group with a total development pipeline of RM3.2 bil.

At the close of today’s mid-day (May 4) trading break, Kinergy was unchanged at 38 sen with 5.21 million shares traded, thus valuing the company at RM830 mil. – May 4, 2026

Main image credit: Open Access Government