IN an effort to reduce inflationary pressures, Bank Negara Malaysia (BNM) on Thursday (Sept 8) increased its overnight policy rate (OPR) by 25 basis points from 2.25% to 2.5%.

The ceiling and floor rates of the corridor of the OPR correspondingly increased to 2.75% and 2.25%, respectively.

Since then, a number of local banks, including Bank Muamalat, Alliance Bank, Maybank and CIMB Bank, said they would raise their standardised base rate, base lending rate, base financing rate, Islamic base rate and fixed return account i-Board rate accordingly.

FocusM takes a look at what the OPR hike entails and how the people will be affected by the move, based on BNM’s Frequently Answered Questions (FAQ) on the matter.

What is OPR?

The OPR is BNM’s policy interest rate that influences, among others, banks’ lending and financing rates as well as deposit rates.

These interest rates inform the public how much the cost of a loan with them will be and the returns for deposits. They are applicable for both conventional and Islamic finance products.

To achieve monetary stability, BNM’s Monetary Policy Committee (MPC) sets monetary policy to keep inflation low and stable while supporting economic growth. The central bank does this by changing the OPR.

What happens when the OPR is changed?

Changes in the OPR affect economic activity and overall price level changes, typically by influencing interest rates in the economy.

When BNM increases the OPR, higher interest rates on savings and loans will influence people to save more and spend less. For example, when the demand for goods and services in the economy is more than the supply available, prices will keep rising; people will pay more to buy what they want.

A higher OPR will help to slow demand down. This brings demand more in line with supply and prices would increase more slowly.

The reverse happens when the OPR is reduced; lower interest rates on loans and savings will get people to save less and spend more. This spurs economic activity and avoids a situation of falling price levels due to weak demand, which will hurt the economy.

Why have interest rates gone up when the cost of living is rising?

BNM cut the OPR from 3% to the lowest level in history, at 1.75%, during the COVID-19 crisis in 2020. The lower interest rates aimed at cushioning the impact of the pandemic when the economy was not healthy and in recession, and made loans cheaper to spur spending.

However, if BNM keeps the OPR too low for too long when the economy is steadily recovering, it could cause too much spending and borrowing, which pushes prices up.

Today, the economy is no longer in crisis. As such, BNM started adjusting the OPR gradually since the health of the economy improved.

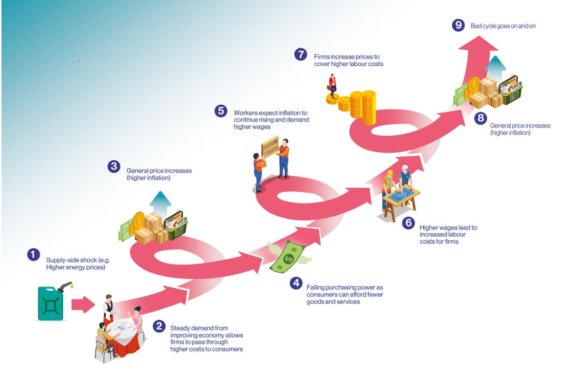

BNM also wants to avoid the case where prices keep rising at a fast pace for many items. This is worse when higher prices lead to higher wages, which then leads to higher prices again. Higher interest rates help to break this cycle:

How will higher interest rates affect me?

Higher interest rates are intended to encourage people to borrow less and save more. Generally, you will see this take effect in two ways, through your loans and savings.

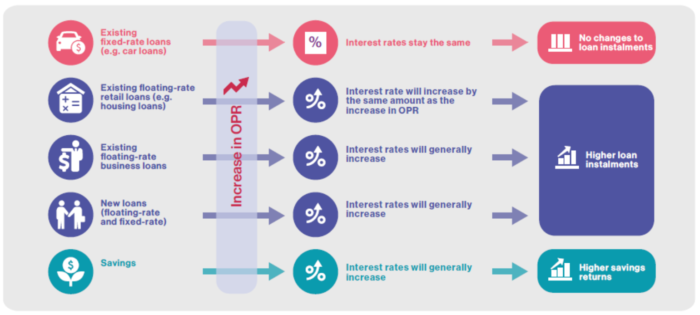

If you have a loan, the effect depends on the type of loan that you have. According to BNM, fixed-rate loans will be unaffected; the amount you pay to your bank will remain exactly the same. Typically, this applies to car loans.

If you have a floating-rate loan, however, your borrowing costs will increase. This means your monthly instalment will be higher. Typically, this will affect housing loans and some personal loans.

For individual borrowers, the interest rate on your loan will increase by the exact same rate as the increase in the OPR. For example, if the OPR is increased by 25 basis points, the interest rate on your housing loan, if previously at 3.5%, will also increase to 3.75%.

Your loan instalment will increase with the higher interest rate and your bank will inform you accordingly. You will receive a notification from your bank spelling out how your repayment amount will change. This will clearly outline your latest interest rate, new repayment amount and when it will take effect so that you can prepare accordingly.

If you are planning on taking out a new loan, borrowings could also become more expensive for you if interest rates are higher.

It is important to understand how a change in interest rates could affect your ability to pay. BNM recommends using a home loan calculator to work out your new monthly instalments, such as this one.

What if I can’t afford the increases to my loan?

Generally speaking, monetary policy is intended to affect the economy as a whole. This is what makes it effective to keep the economy healthy.

BNM said borrowers should be aware that repayments for floating-rate loans will change if the OPR changes and consider whether they can afford the loan if the interest rates were to increase.

Having said that, if you are an existing borrower with fixed-rate loans, BNM said you will not face higher interest rates for the loans you currently have.

Even so, BNM acknowledges that an increase in interest rates may be more difficult to handle for some.

If you are having trouble repaying your monthly loan instalments, the best thing you can do is get in touch with your banks or the Credit Counselling and Debt Management Agency (AADK) as soon as possible to learn about the support options available. – Sept 10, 2022

Main photo credit: Malay Mail