Eco World Development Group (EcoWorld) delivered a strong first-half performance for FY2026, with core net profit reaching RM285.6 million.

This accounts for approximately 52% of both analysts’ full-year earnings projections and market consensus estimates, placing the group on a solid footing to meet expectations for the financial year.

Compared with the corresponding period last year, core net profit rose 46% after adjusting for sukuk-related payments and one-off disposal gains recognised previously.

The improvement was mainly driven by a significant increase in revenue, which benefited from the recognition of a land sale during the first quarter. Revenue for the six-month period expanded 52% year-on-year.

However, gross profit margin eased to 27.7%, reflecting a less favourable product mix compared with the previous year.

On a quarterly basis, second-quarter revenue declined 41% from the preceding quarter as the earlier land sale contribution was no longer present.

Despite the lower revenue base, profitability remained relatively resilient. Gross margin improved to 31.3% due to stronger product mix and the lower-margin nature of the land sale recognised previously.

As a result, core net profit slipped by a more moderate 17% quarter-on-quarter.

Looking ahead, EcoWorld’s sales momentum remains encouraging. As at May 2026, the group had secured RM3.28 billion in sales, equivalent to 82% of its RM4 billion sales target for FY2026 and ahead of the RM2.99 billion achieved during the same period last year.

Although management has retained its existing sales target, current trends suggest the company is well-positioned to exceed its FY2025 sales achievement of RM4.55 billion. Demand for industrial developments continues to be a key growth driver.

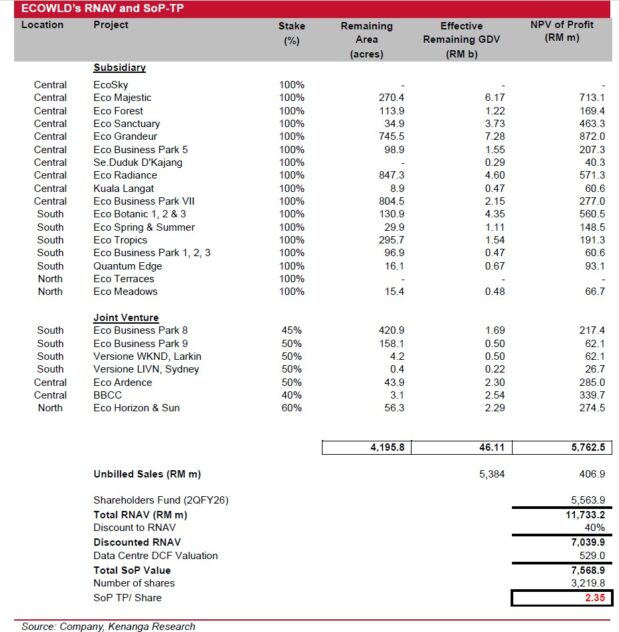

Future growth is expected to be supported by the group’s industrial development pipeline, including Eco Business Park VIII, with an estimated gross development value (GDV) of RM3.75 billion and targeted for launch towards the end of FY2026, followed by Eco Business Park IX, which carries a GDV of RM1 billion and is slated for FY2028.

In the residential segment, EcoWorld is building on the success of its Duduk Series by introducing Versione WKND, a more upscale high-rise development in Iskandar.

The launch comes at an opportune time as affordability concerns and inflationary pressures could weigh on demand for lower-priced housing products.

Meanwhile, construction of the group’s build-to-lease data centre project for Pearl Computing remains on schedule for completion by the end of FY2027.

Revenue contribution is expected to commence in FY2028. The project is underpinned by a 20-year lease agreement valued at RM4.8 billion, translating into recurring annual income of approximately RM240 million.

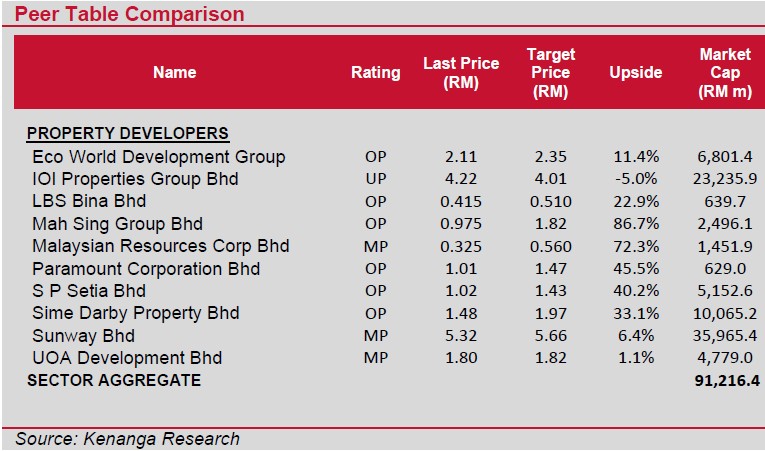

From a valuation perspective, EcoWorld continues to stand out due to its strong brand equity, quality developments, healthy resale values and contemporary product offerings.

The group’s ability to adapt its product mix to changing market conditions also enhances its competitive position.

In addition, the future income stream from the Pearl Computing lease arrangement should strengthen recurring earnings and provide greater resilience against fluctuations in the property cycle.—June 19, 2026

Main image: New Straits Times