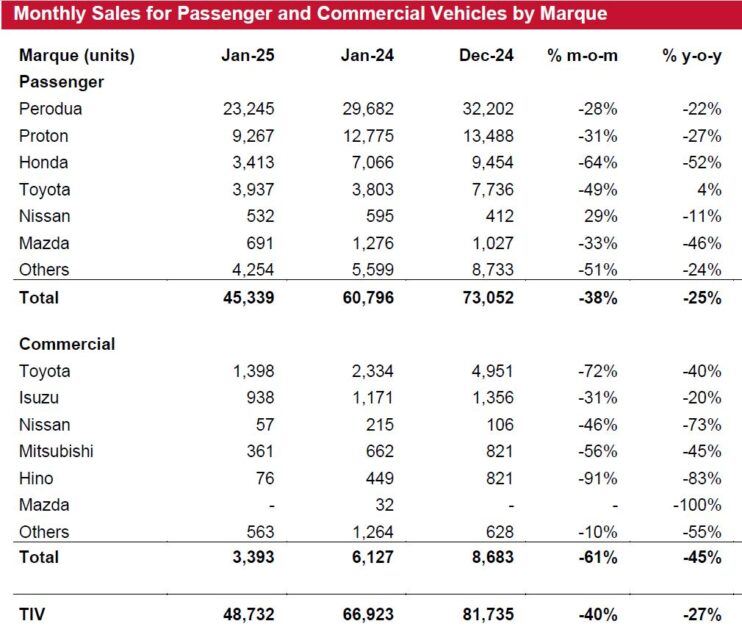

TOTAL industry volume (TIV) plunged 40% month-on-month (MoM) but drop less by 27% year-on-year (YoY) to 48,732 units in January 2025 from extended Chinese New Year holidays.

“Also, there were less discounts offered in quarter one of calendar year (1QCY) while consumers wait for more attractive new launches typically by mid-year 2025,” said Kenanga Research (Kenanga) in the recent Sector Update Report.

Looking ahead, Kenanga believes February 2025 TIV will be significantly higher than January 2025 TIV on a longer working month and pre-buying spree before Hari Raya Aidilfitri holidays.

A two-speed automotive market locally will persist into the calendar year 2025 (CY25).

It will be business as usual for the affordable segment as its target customers, that is the B40 and lower tier M40 groups, will be spared the impact of the impending RON95 subsidy rationalization and could also potentially benefit from the introduction of the progressive wage model.

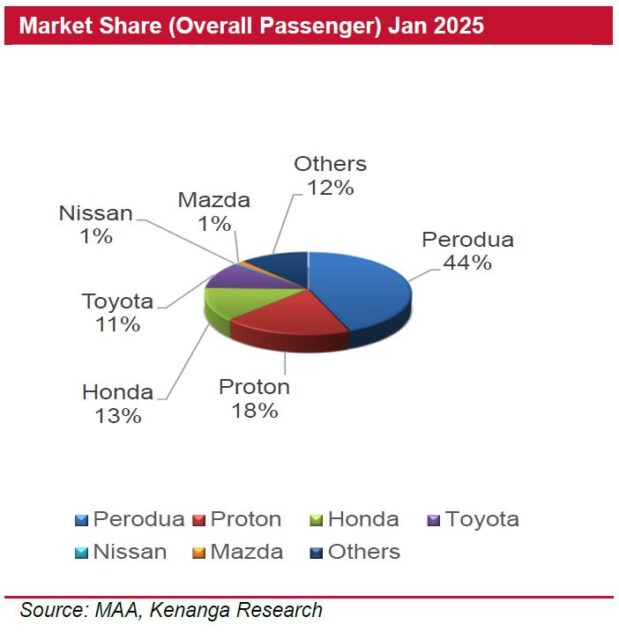

“Our CY25 TIV forecast of 805k units will be driven by the forward buying interest on the deferment of new excise duty regulations to end-2025 of which we expect Perodua to benefit the most at 44% TIV market share with the highest localisation rate as well as attractive new launches, higher household income,” said Kenanga.

Note the government servants’ salary hike in December 2024, and higher minimum wages starting February 2025, and a stable labour market.

However, the same cannot be said for the premium segment as its target customers, that is the upper tier M40 and T15 groups who may hold back from buying new cars, down trade to smaller cars or switch to hybrids and EVs to cut their fuel bills upon the introduction of fuel subsidy rationalisation.

In general, the industry’s earnings visibility is still good, backed by a booking backlog of 80K units as at end-February 2025.

More than half of the backlog is made up of new models, alluding to the appeal of new models to car buyers. This trend is likely to persist throughout CY25 given a strong line-up of new launches.

More battery electric vehicles (BEVs) in the market. Vehicle sales will also be supported by new BEVs that enjoy SST exemption and other EV facilities incentives up until CY25 for complete built ups and CY27 for complete knockdowns.

The new registration for BEVs leapt from 274 units in CY21 to over 3,400 units in CY22, 13,301 units in CY23, and 21,789 units in CY24, or 3% of TIV.

“We expect more favourable incentives from the government which has set a national target for EVs and hybrid vehicles of 20% of TIV by CY30 and 38% by CY40,” said Kenanga.

Meanwhile, the government will speed up the approval for charging stations. The number of proposed charging stations is currently at 4,299 (3,611 built to date) and this should more than double to 10,000 by end-CY25.

Further on, Kenanga anticipates a robust demand for the motorcycles market as its target customers, that is the B40 & M40 groups, will be spared the impact of the impending RON95 subsidy rationalisation.

It is to be priced in a two-tier system in June 2025 whereby the T15 group will be confined to only unsubsidised pricing. —Mar 3, 2025

Main image: Asian Insiders