KELINGTON Group’s (KGB) quarter three 2025 (3Q25) results were broadly in line with quarterly profit after tax and minority interest (PATMI) at a new high from further NPM uplift.

“We see a sequentially stronger 4Q25 on improved billings,” said RHB.

Earnings prospects are well supported by the robust outstanding orderbook and sizable MYR4.5 bil tenderbook, driving a 2025-27 compounded annual growth rate of 14%.

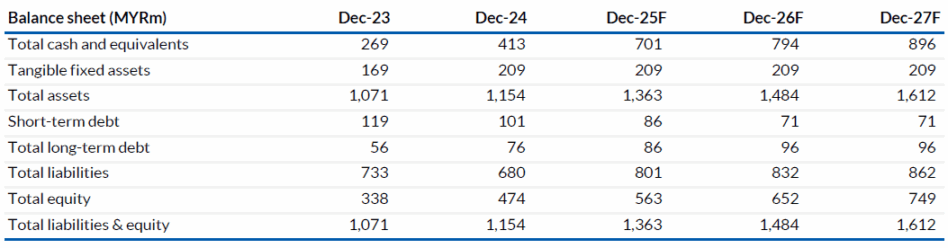

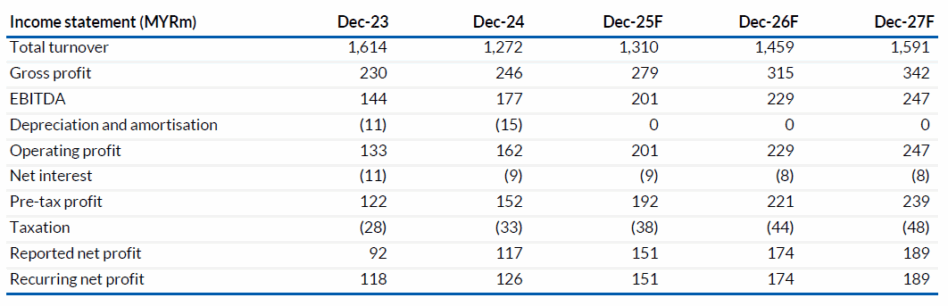

3Q25 core earnings of MYR44.5 mil brought 9M25 core earnings to MYR98.7 mil, at 66% of RHB’s forecast (consensus: 67%), within historical run-rates with a stronger 4Q25 in the offing.

Advanced engineering remained the dominant segment with weaker Malaysia (-22%) and China (-23%) revenues partially offset by stronger Singapore revenue (+22%).

Industrial gas revenue fell 21% on lower specialty gas sales, mitigated in part by steady liquid carbon dioxide (LCO2) demand.

“We gather the size of the tender for the second German fab (a JV with Taiwan’s largest foundry) is likely to come in lower as a portion of the job has been farmed out by its principal,” said RHB.

This should be offset by a potential ramp-up in its India tenderbook with “offset manufacturing” processes adopted.

RHB expects KGB to sign the JV agreement with Worldwide Energy Development (WED) and SKS Coachbuilders (SKS) for the development of a 2MW green H2O production hub by month-end/December.

Construction of the hub should take 6-9 months, with the initial production of 200 cum/hour taken up by SKS, which is slated to deploy its fleet of fuel cell buses.

“We view the recent share price weakness as a healthy correction following the strong year-to-date rally,” said RHB.

At the current level, the stock trades are backed by a record tenderbook, solid earnings delivery, and the longer term earnings upside from its carbon capture and utilisation business which the market has yet to price in. —Nov 25, 2025

Main image: Kelington