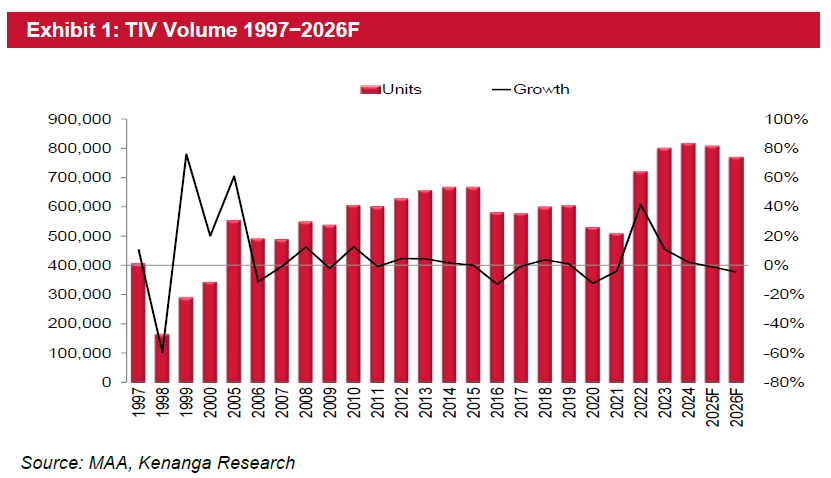

KENANGA projects a total-industry-value (TIV) of 725K units in 2026 (a decrease of 9.9% from their 2025 TIV forecast of 805k units).

Anecdotally, in2015, there was a tax holiday incentive-induced sales which propelled 2015 TIV to a record high at that time of 666k units, and thereafter, in 2016, TIV fell 13% post-GST tax holiday.

“Coincidently, we believe the current situation to be relatively the same as 2025 sales was sustained by the EV complete build up (CBU) tax holiday incentives, and presumed implementation for new OMV excise duty regulation in 2026,” said Kenanga.

Kenanga’s thesis for 2026 TIV encompasses:

(i) New open-market-value (OMV) excise duty regulation which will be implemented gradually starting 2026 (the policy to limit the vehicles price hike is still being developed, on which Kenanga expect the price hike will range in between 10% to 30% based on the localisation rate for each vehicles).

(ii) A rising market share of Chinese automakers vehicles through vehicles production localisation programmes.

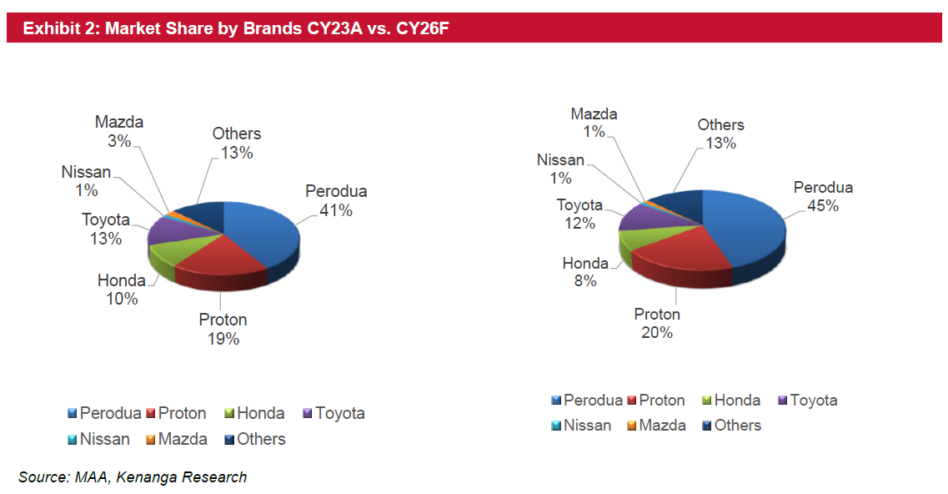

(iii) Sustained demand in the affordable segment with national marques remaining as the market leader at estimated market share of 65% for 2026 TIV compared to non-nationals marques’ target focus of mostly in the RM100k-and-above vehicles segment.

(iv) The new hire purchase loan policies starting 2026 are designed to create a fairer lending environment for consumers, which may boost confidence in hire purchase loans over the long term.

(v) a stable labour market (Kenanga’s economic research team forecast unemployment rate of 3% in 2026 vs. 3% in 2025).

(vi) attractive new launches that is Proton e.Mas 7 Phev, Perodua Myvi (new DNGA), Mazda CX-5 (new generation), Xpeng MO 3 sedan and BYD Shark PHEV 4×4.

In general, the industry’s earnings visibility is still good, backed by a booking backlog of 130k units as at end-November 2025.

More than half of the backlog is made up of new models, alluding to the appeal of new models to car buyers.

This trend is likely to persist in 2026, given the strong line-up of new launches. Kenanga expects gradual transition to BEVs which currently enjoys tax exemption up until 2027 for locally-assembled complete knockdowns.

“Looking further, we also have a nuanced view of EV adoption eventually picking up and gasoline demand will eventually peak, but we do not think that will happen in the next five years due to infrastructure challenges,” said Kenanga.

This new petrol subsidy mechanism could make the transition even slower than earlier expected as the middle- and lower-income group now have less incentive to switch from ICE to EV for the time being.

Recall that, the new registration for BEVs leapt from 274 units in 2021 to over 3,400 units in 2022, 13,301 units in 2023, and 21,789 units in 2024, or 3% of TIV.

In the latest announcement, the BEV registration for Jan-Nov 2025 is at 36,690 units far surpassed 2024 numbers, which mostly driven by CBU models. Malaysia aims for electric vehicles (EVs) to represent 20% of new vehicle sales by 2030, with longer-term vision extends to 80% by 2050 (including hybrids vehicles).

Government is currently focused on building out the EV ecosystem, including establishing 10,000 public charging points (no updated timeline target yet from the earlier by 2025, despite the current build-to-date lagging behind with just tad above 50% of the target) with current number of proposed charging stations currently at 4,477 (5,149 built-to-date) and providing tax incentives to stimulate adoption and local production. —Dec 23, 2025

Main image: The Star