AMID THE still-fluid events unfolding in the Middle East conflict, the timing of pivot of the Federal Reserve rate cut has shifted towards the last quarter.

Locally, Kenanga Economists foresee that inflation will inch up for 2026, to 2.1% from 1.9% previously, slightly crimping on returns including from dividends.

“Thus, we take the opportunity to consider dividend counters that are more resilient in this environment,” said Kenanga.

Company dividends could depend more on cashflow strength amid potential supply chain/logistics disruption.

Given that the effective blockade on the Straits of Hormuz is likely to have knock on impact to supply chains, and logistics bottlenecks, firms will likely prioritize working capital needs.

Thus, the willingness to pay dividends would be tied in with cashflow strength, in addition to maintaining comfortable gearing levels, rather than purely profits.

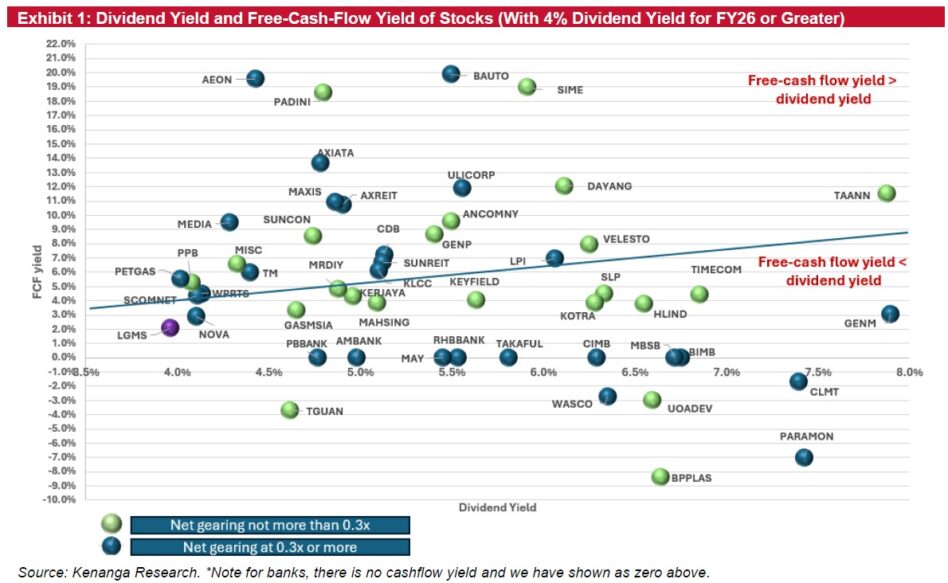

“To begin our screening, we base our universe with stocks that are capable to meet a 4% dividend yield, which filters out most of the higher growth sectors such as technology, and renewable energy,” said Kenanga.

Kenanga counts MRDIY and PADINI as fitting the criteria with respect to cashflow strength, and also relatively lowly geared balanced sheets (though low stock trading liquidity in the latter could be a consideration for some).

“Within the industrials/construction space, we like SUNCON,” said Kenanga.

While BAUTO possesses a more elevated gearing, and we are mindful of temporary potential shipment delays, these are in our view overshadowed by the encouraging sales from CBU MAZDA models, which in turn preserves good dividend visibility.

Within the Telco space, TIMECOM formally adopting an improved dividend payout policy will keep interest high.

Patience would be rewarded for banks. Their picks for dividend resilience include CIMB and PBBANK – the former given its stated intention to reward shareholders and the latter for higher potential payout from improved CET1 ratio come July, where they estimate the potential benefit could be up to 4% in yield terms.

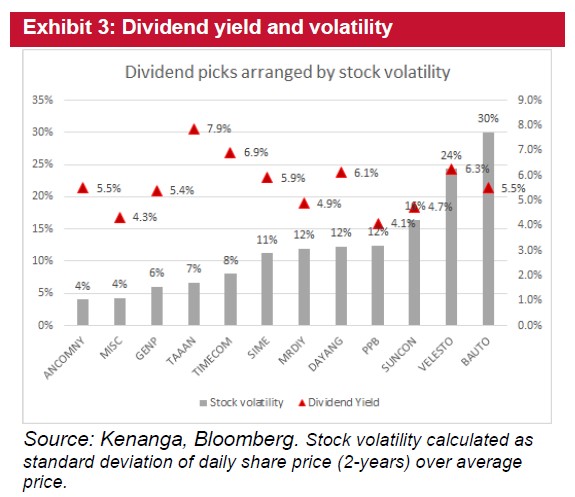

Plantation and oil and gas sectors tick the boxes though these are the more volatile sectors.

“Plantation and oil and gas firms have been previously highlighted by us as potential beneficiary from the middle east conflict,” said Kenanga.

For oil and gas firms, crude oil prices potentially staying sustainably elevated provides a fillip to capital expenditure.

In the interim, some of these companies generate strong cashflow and thanks to solid balance sheets and names such as DAYANG, VELESTO and MISC fit Kenanga’s dividend recommendations. —Mar 24, 2026

Main image: livemint.com