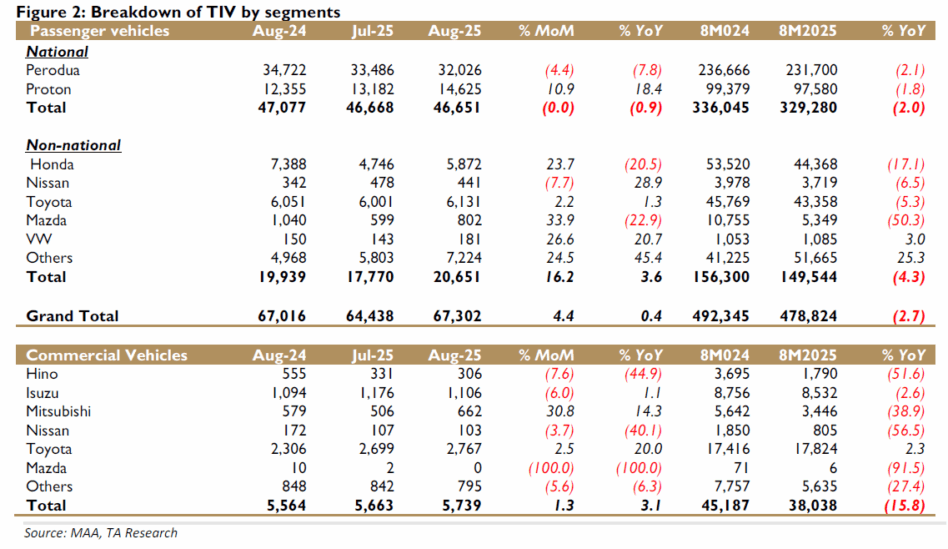

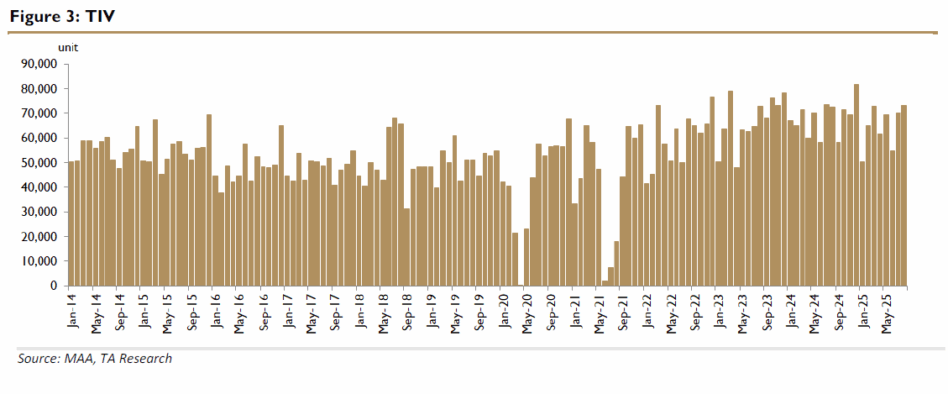

ACCORDING to the Malaysian Automotive Association (MAA), the total industry volume (TIV) for Aug 2025 stood at 73.0k units, up 4.2% month-on-month (MoM) from 70.1k units in Jul 2025.

The stronger performance was attributed to higher stock availability from July’s robust production of 71.4k units, aggressive promotions during the Merdeka celebration month, and the sales impact from new model launches.

Passenger vehicle sales rose 4.4% MoM, while commercial vehicle sales inched up 1.3%. On a year-on-year (YoY) basis, Aug 2025 TIV was broadly flat at +0.6%, with passenger sales up 0.4% and commercial sales up 3.1%.

For the eight months of 2025 (8M2025), cumulative TIV fell 3.8% YoY to 516.9k units, weighed by softer passenger and commercial segments.

Looking ahead, MAA expects sales momentum in Sep 2025 to consolidate, impacted by fewer working days due to four public holidays and a “wait-and-see” stance ahead of the 2026 National Budget announcement, including details on petrol subsidy rationalisation.

“In our view, planned plant shutdowns by major industry players could further weigh on Sep TIV,” said TA Securities.

In Aug 2025, total national passenger vehicle sales were largely stable at 46.7k units, almost flat compared to July 2025, but slightly down 0.9% YoY.

Perodua declined 4.4% MoM (32.0k units), mainly due to lower demand and inventory adjustments following strong sales in prior months.

Proton, on the other hand, rose 10.9% MoM to 14.6k units, supported by strong demand for the X50 and Saga, nationwide promotions, and growing EV sales.

Year-to-date , total TIV stands at 329.3k units, reflecting overall cautious market sentiment despite Proton’s strong monthly performance.

Non-national passenger vehicles rose 16.2% MoM to 20.7k units in August, supported by Honda (+23.7% MoM), Mazda (+33.9% MoM), VW (+26.6% MoM), and others (+24.5% MoM), while Nissan dipped slightly (-7.7% MoM).

On a YoY basis, non-national sales increased 3.6%, led by VW (+20.7%) and Others (+45.4%), partially offset by weaker performance from Honda (-20.5%) and Mazda (-22.9%). YTD, non-national sales totalled 149.5k units (-4.3% YoY).

Correspondingly, we downgrade our sector rating to underweight from neutral, driven by a lack of near-term catalysts to reverse the current overpriced valuation.

Intense price competition is expected to pressure margins, suggesting that market share gains by any brands are likely achieved at the expense of profitability.

Our 2025 TIV forecast remains at 750k units, representing an 8.2% YoY decline, underscoring the cautious outlook for the automotive sector. —Sept 22, 2025

Main image: Auto World Journal