A HEIGHTENED risk of a strong El Nino is beginning to take shape. Although the boost from energy-related demand has eased in recent months, the growing possibility of a severe El Nino episode could become a fresh driver for crude palm oil (CPO) prices by tightening supply, reinforcing MBSB’s Positive outlook on the plantation sector.

This assessment is supported by the latest forecast from Met Malaysia, which projects that El Nino conditions could develop as early as July 2026 and extend into the early months of 2027.

The weather phenomenon is also expected to have an uneven impact across the country, with East Malaysia likely to experience more significant changes in rainfall patterns than Peninsular Malaysia.

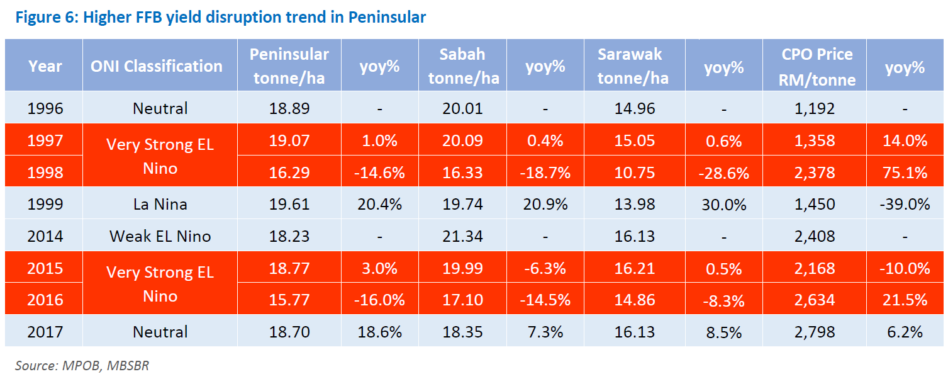

During the 1997/98 event, rainfall in Sabah and Sarawak declined by approximately -34% year-on-year (yoy) and -24% yoy respectively, compared to a smaller decline of around -15% yoy in Peninsular Malaysia.

However, in the latest episode of 2015/16, Sarawak seems less affected with turnaround +10% yoy rainfall increased.

As palm oil is largely a rain-fed crop, any prolonged deviation in rainfall intensity and distribution could affect crop development, pollination efficiency and fruit formation, ultimately influencing fresh fruit bunch (FFB) yields.

Should the anticipated 2026/27 very strong El Nino mirror the 1997/98 and 2015/16 episodes, national FFB yields could decline by approximately 12%-22% yoy, based on historical observations.

Notably, peninsular Malaysia appears increasingly vulnerable. This reiterates MBSB’s Buy call on eastern planters.

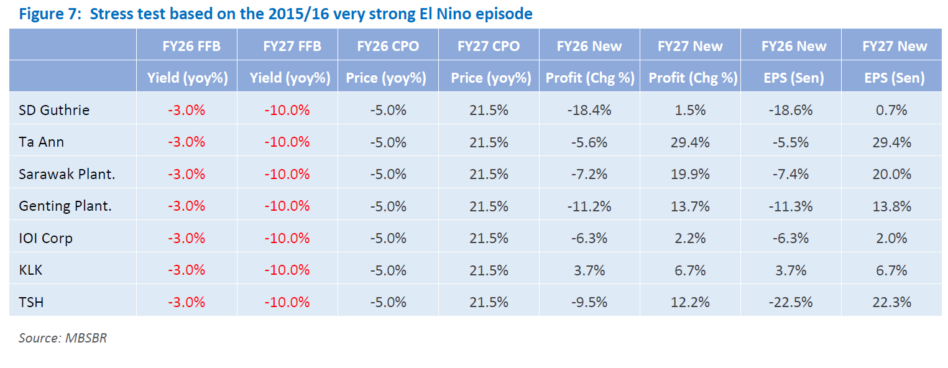

Under this scenario, the most notable beneficiaries are Ta Ann and Sarawak Plant, given their higher operational leverage to CPO prices and geographical advantage.

Both companies are expected to record the strongest earnings recovery in 2027 as the sharp improvement in CPO prices more than offsets weaker crop production.

Genting Plantations and TSH also demonstrate meaningful earnings upside, supported by their predominantly upstream earnings exposure.

In contrast, integrated players such as IOI Corp and SD Guthrie exhibit a more muted earnings response due to the cushioning effect from their downstream operations.

Meanwhile, KLK emerges as the most defensive name under the stress test, with its diversified earnings base allowing it to remain resilient despite lower FFB yields. —June 29, 2026

Main image: MUSIM MAS