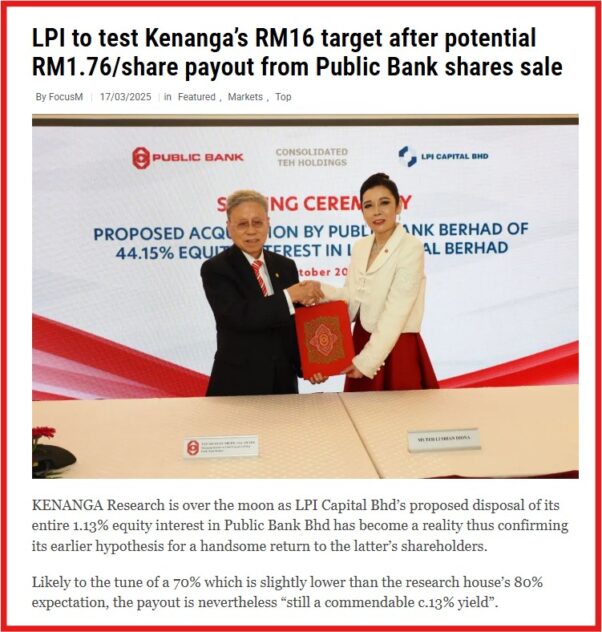

PATIENCE – or rather holding power – of shareholders to the much-anticipated windfall from the assumed 70% distribution of the entire disposal of Public Bank Bhd’s shares is probably what is keeping the share piece of LPI Capital Bhd intact in recent times.

Recall that although the initial regulatory requirement was to divest the Public Bank shares within 12 months of becoming a Public Bank subsidiary – notably Dec 3, 2025 – the general insurer was granted an extension to a new deadline of June 3 this year (with disposal to be executed in multiple tranches via direct business transactions).

Then a second extension was granted at the group’s 65th annual general meeting (AGM) on April 8 when shareholders voted overwhelmingly in favour to the renewal of existing shareholders’ mandate resolution to dispose of its 1.13% stake amounting to 229.29 million Public Bank shares.

Editor’s Note: Approval was granted with 700 shareholders holding 99.9642% shares agreeing to the disposal timeline extension in contrast to 64 shareholders with 0.0358% shareholding.

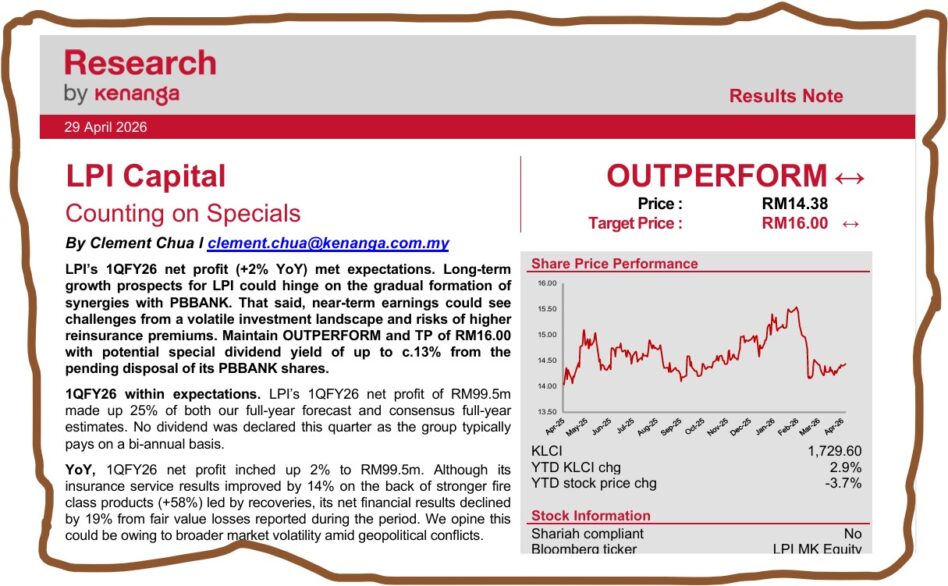

Although the disposal will be indefinitely shelved, Kenanga Research has retained its “outperform” rating on LPI with a target price of RM16.00 on the back of a “potential special dividend yield of up to c.13% from the pending disposal of its Public Bank shares”.

“Assuming a 70% distribution from the entire disposal of its Public Bank shares at the current price point of RM4.78/share, investors could enjoy a special dividend of up RM1.84/share or 12.8% yield,” projected analyst Clement Chua in the research house’s results review of LPI.

“There is no adjustment to our target price based on ESG given the three-star rating as appraised by us.”

Year-on-year (yoy), LPI’s 1Q FY2026 net profit ended March 31, 2026 inched up 2% to RM99.54 mil (1Q FY2025: RM97.98 mil) while its revenue firmed 6.3% to RM547.7 mil (1Q FY2025: RM515.1 mil).

Quarter-on-quarter (qoq), LPI’s 1Q FY2026 net earnings surged by 39% (4Q FY2025: RM71.81 mil) mainly driven by higher investment income from dividends received during the quarter.

Excluding dividend returns, earnings would have still improved by 7%, thanks to lower net claims between its fire and miscellaneous insurance.

Justifying its RM16 target price further, Kenanga Research contended that it represents a 25% premium against the industry average of 2.1x which to its view is fair given “(i) better net margins of 18%-20% (vs peer’s 11%); and (ii) higher dividend returns of 5%-6% (vs peer’s 4%-5%).”

“LPI’s premium valuation may also be supported by its long-term viability from its affiliation with Public Bank with the pending solidifying of synergies,” added Kenanga Research.

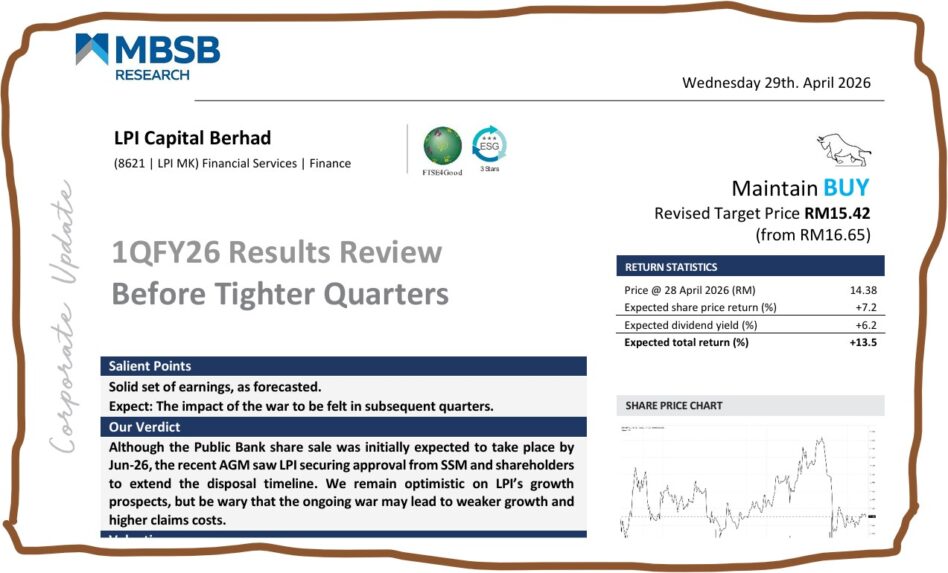

Elsewhere, MBSB Research (formerly MIDF Research) sees “high chance of the special dividend payout in FY2026”.

“At Public Bank’s current price, this could translate to RM783 mil worth of dividends,” opined analyst Samuel Woo. “Collaborative efforts between LPI and Public Bank are expected to kick in by FY2026, translating to higher cost savings and operational efficiency.”

Like Kenanga Research, MBSB Research also maintained its “buy” call on LPI but revised its target price downward to RM15.42 from RM16.65 “to reflect altered earnings prospects and ROE-based valuations”.

At the close of today’s (April 29) mid-day trading break, LPI was unchanged at RM14.38 with 19,700 shares traded, thus valuing the insurer at RM5.73 bil. – April 29, 2026