THE rollout of the sixth cycle of the Large Scale Solar (LSS6) programme is expected in the near future and could provide a significant boost to order books for solar engineering, procurement, construction and commissioning (EPCC) companies.

If the programme is launched in the third quarter of 2026 as anticipated, contract awards are likely to follow in early 2027, in line with the typical six-month tender process observed in previous cycles.

Industry sources suggest that LSS6 will require the integration of battery energy storage systems (BESS), adding around 2GW of storage capacity.

“We estimate this could create approximately RM8 bil worth of EPCC opportunities,” said Kenanga.

The inclusion of BESS, which is expected to account for 40% to 50% of the project’s additional costs, could also lift contract values to roughly double those seen in earlier LSS rounds.

Although the larger contract sizes are expected to attract more competitors into the market, companies with established expertise and stronger financial positions are likely to have a distinct advantage.

“In our view, leading incumbents such as SLVEST and SAMAIDEN remain well placed to capture a sizeable share of the upcoming projects, supported by their proven execution capabilities in utility-scale solar developments and healthy balance sheets,” said Kenanga.

The Corporate Renewable Energy Supply Scheme (CRESS) remains the key to medium-term replenishment opportunities for utility-scale solar players, namely SLVEST, SAMAIDEN and SUNVIEW.

Near-term contract conversions will be concentrated among ultra-high voltage (UHV) consumers, specifically hyperscale data centers seeking to hedge against escalating utility overheads under the revised TNB tariff structure while fulfilling corporate decarbonization mandates.

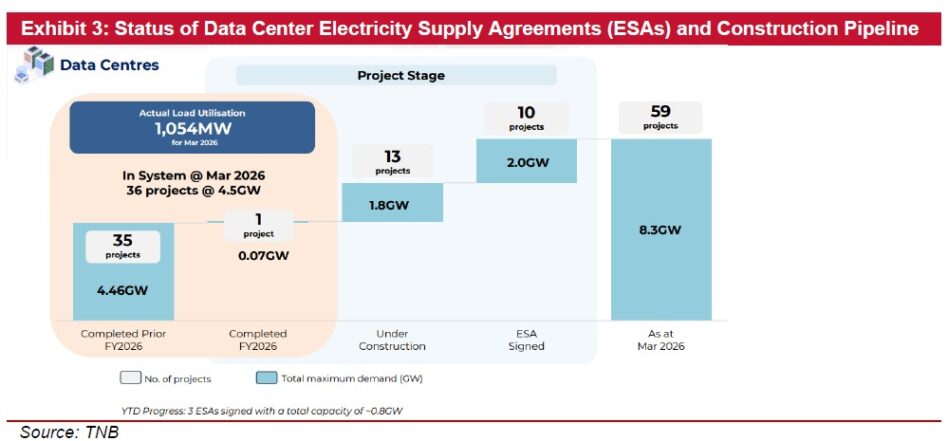

The massive pipeline of 8.3GW in signed Electricity Supply Agreements (ESAs) as of March 2026 highlights Peninsular Malaysia’s continuous data center (DC) growth. Rooftop solar installers are likely to see earnings improvement in the second half of 2026, driven by the government’s rollout of the Suria Home rebate program.

Under this scheme, domestic consumers installing residential solar assets are eligible for a cash rebate of RM600 per kWac, capped at a maximum of RM3,000 per household.

Channel checks indicate these cash rebates will improve residential payback periods by 0.5 to 1.0 years depending on system size, which is expected to support near-term earnings visibility for rooftop-focused players such as VERDANT, PEKAT, and BMGREEN.

“We note that the Suria incentive cap has been reduced from RM4,000 under Solaris to RM3,000, highlighting a clear policy shift toward self-consumption aligned with active residential energization and reducing reliance on export-driven economics,” said Kenanga.

With Malaysia’s residential solar penetration still in the single digits, this underpenetrated market continues to offer visible opportunities for a sustained multi-year upcycle.

Kenanga continues to favour SAMAIDEN as our top pick within the solar infrastructure space.

The research house favours SAMAIDEN because its strategic pre-procurement of c.500MW out of an 800MW total panel pipeline, which has been successfully delivered in Malaysia and is currently undergoing progressive site installation, effectively insulates its margins from the initial China VAT export shock.

SAMAIDEN remains well positioned to scale its LSS5+ market share from the current 5% closer to its 12% historical share achieved under the previous LSS5 cycle.

Backed by a strong balance sheet, the Group also remains well positioned to capture a meaningful share of the upcoming CRESS multi-gigawatt rollout, placing these upcoming contract wins well within their near-term execution capabilities.—June 30, 2026

Main image: Canva