MBSB Research earnings estimates for Malayan Cement remain unchanged as the group’s cumulative financial year 2025 (FY25) results were within expectations.

“Malayan Cement is among our top picks for the construction sector, given its position as the main direct beneficiary of the sector’s upcycle,” said MBSB.

Demand is expected to be underpinned by a robust pipeline of civil and private projects, including warehouses, data centres, and residential developments, while the anticipated rollout of MRT3 is set to provide an additional multi-year catalyst.

The upcoming Johor-Singapore Special Economic Zone (JS-SEZ) is also expected to unlock new growth opportunities, particularly for supporting industries.

Furthermore, the group is well-placed to capitalise on export demand through its strategically located Langkawi plant, reinforcing utilisation rates and earnings visibility.

On the civil side, projects such as the Penang LRT and airport expansions are expected to add to the momentum, while other infrastructure developments under Budget 2025 and 13MP, including roads, schools, and hospitals, should continue to drive demand.

With improving job flows anticipated from the second half of calendar year 2025 (2HCY25) and into CY26, Malayan Cement stands to benefit directly, with its strong market leadership and pricing power reinforcing our positive view on its earnings trajectory and long-term prospects.

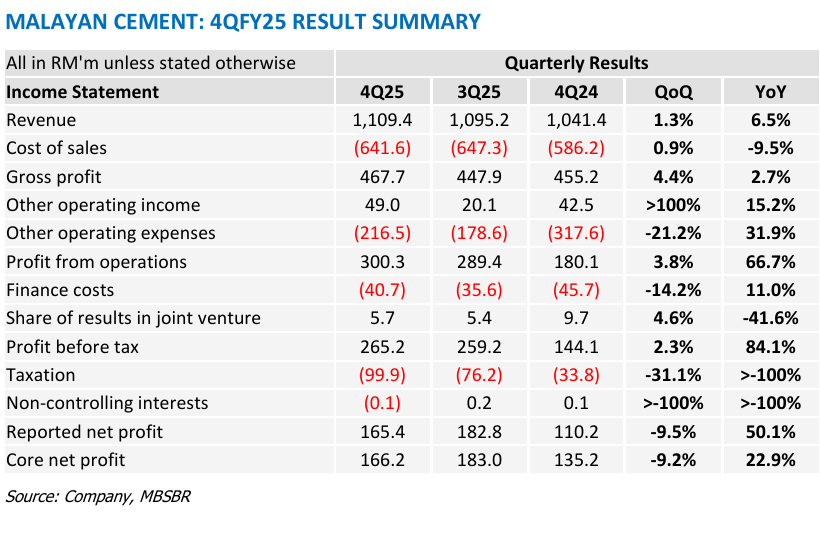

Malayan Cement recorded a core net profit of RM166.2 mil in quarter four financial year 2025 (4QFY25), surging +22.9 year-on-year (yoy) from the previous year’s corresponding quarter.

For the cumulative FY25, the group’s core net profit grew +29.9% yoy to RM649.7 mil, coming in within ours and street’s expectations, making up 102.3% and 104.9% of full-year estimates respectively.

This was mainly attributable to higher revenue contribution from the aggregates and concrete segment as well as increased cement exports. The quarter saw a +2.26%yoy increase in revenue from cement to RM887.9 mil with operating profit growing +69.4% yoy to RM280.3 mil, attributable to improved operational efficiency and strengthened margins.

For the cumulative FY25, while revenue fell -3.95%yoy to RM3.63 bil, its operating profit grew +31.0%yoy to RM995.7 mil. The increase in bottom line was also due to continuous efficiency upgrades, including investments in operational efficiencies and ESG-driven improvements.

However, management highlighted that segment sales volume declined by approximately -2.0% during the quarter, largely due to the absence of major project rollouts. On the cost side, coal and electricity prices remained broadly stable, with coal registering a slight decline, which in turn supported margin efficiencies as well. —Aug 22, 2025

Main image: YTL Cement