THE offshore support vessel (OSV) vessel market continues to face chronic under-investment, as the global fleet ages progressively each year.

According to Clarksons, 80% of the global OSV fleet will be over 20 years old by 2035, indicating that a significant portion of vessels may no longer be in optimal working condition if substantial reinvestment in fleet renewal does not occur.

“We believe shipowners are still having fresh memories of the previous downcycle that began in 2015, when speculative overbuilding led to a prolonged and painful decline in DCR, triggering multiple bankruptcies, particularly among companies with highly leveraged balance sheets,” said Kenanga.

While there are some newbuild activities emerging in the Middle Eastern market, they remain insignificant relative to the global OSV fleet. Most vessel classes including anchor handling tug & supply and others continue to see minimal newbuild activity, with only Platform Supply Vessels (PSVs) experiencing a modest increase in upcoming capacity.

Importantly, the majority of these newbuilds are already chartered, primarily to the Middle East and Chinese markets, meaning none are expected to enter the Asia Pacific market.

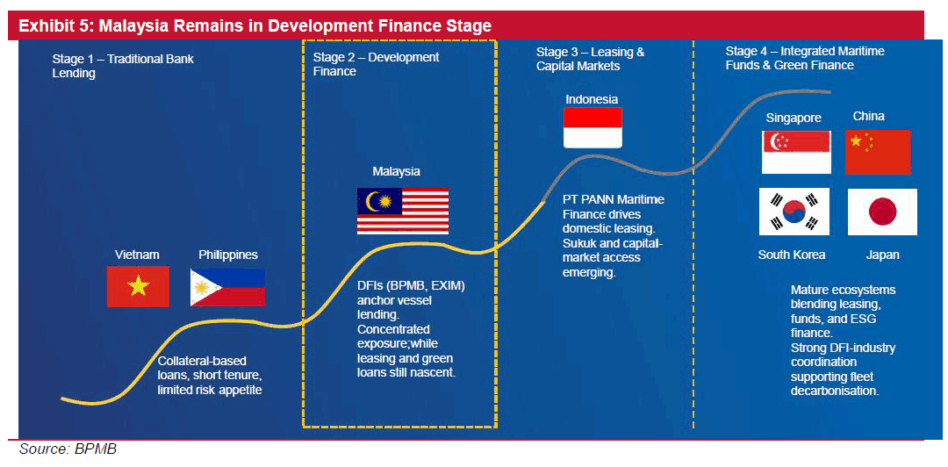

According to BPMP, Singapore is classified as Stage 4 on the vessel financing maturity curve, reflecting a well-developed ecosystem that integrates leasing, project financing, and green/ESG-linked facilities.

This is further supported by strong policy coordination between regulatory authorities and financial institutions, enabling a more dynamic and responsive maritime financing landscape.

In contrast, Malaysia is currently at Stage 2, where vessel financing is still largely driven by development finance institutions, with limited participation from commercial banks.

There is also no dedicated maritime fund or credit guarantee scheme in place, which restricts the breadth of financing options available to local OSV players.

“Given this disparity, we believe Singapore could serve as a useful model for Malaysia’s banking system to emulate, particularly in expanding financing avenues to support fleet renewal programmes for local OSV operators,” said Kenanga.

Strengthening the financing framework will be critical to unlocking long-term growth and ensuring Malaysia remains competitive in the regional maritime ecosystem.

During the event, it was highlighted that the era of easy oil, characterised by lower costs and simpler extraction is over, as Malaysia’s current top three producing basins (Malay, Sarawak, and Kinabalu) alone will not be sufficient to sustain the country’s production target of 2m barrels of oil equivalent (boe) per day by 2035.

According to Petronas, maintaining output from these basins will require the group to venture into five new basins namely the Langkasuka, Penyu, Layang-Layang, Sandakan, and Tawau basins, through expanded seismic studies and future technical evaluation agreements with industry partners.

“Despite the near-term slowdown in upstream activity, we believe that Petronas will need to undertake a structural increase in capex spending to meet its long-term production goals,” said Kenanga.

This bodes well for local service providers, offering greater visibility and long-term certainty in potential contract flows, as it aligns with the broader objective of sustaining Malaysia’s oil and gas income over the coming decades.

Kenanga maintains Neutral on the sector as it is still the early days on OSV potential recovery cycle.

“Given the confluence of a weak crude oil price outlook and the unresolved PETROS–Petronas uncertainty, we expect upstream service activity to remain tepid for the remainder of 2025, while the petrochemical market continues to oscillate near its cyclical bottom,” said Kenanga.

Looking further ahead, however, Kenanga sees ample upside potential, particularly in the OSV segment, which remains in a structural underinvestment cycle, a dynamic that could support higher average DCRs over the longer term. —Nov 17, 2025

Main image: pan-marine.net