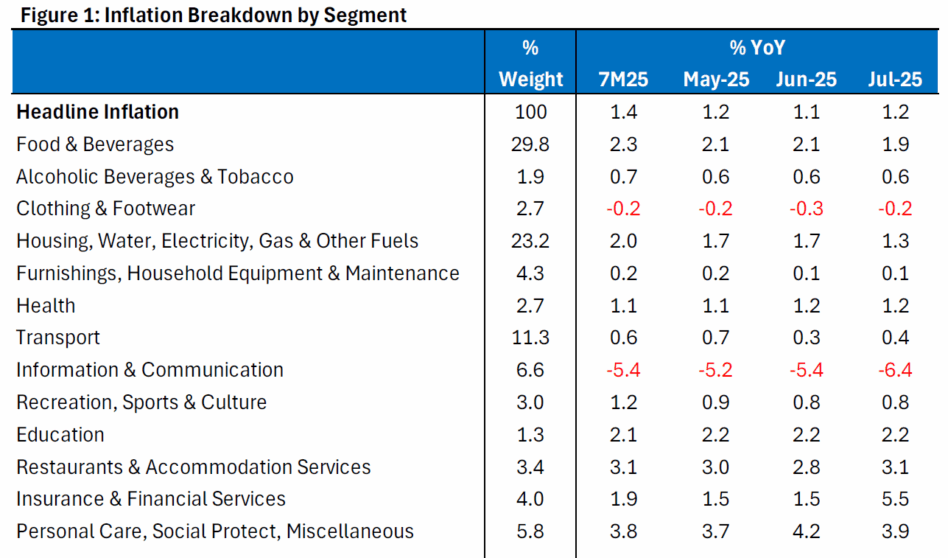

MALAYSIA’s headline inflation edged up to +1.2% year-on-year (YoY) in July 2025, in line with Bloomberg consensus. Core inflation was unchanged at +1.8% for the third straight month.

Among the key components, transport cost inched up (+0.4%) amid a smaller decline in pump prices. The general downtrend in Brent prices this year should continue to cap transport costs ahead.

Meanwhile, food prices eased to +1.9%, driven by softer “food away from home.”

Policy effects were evident in July, with two components standing out, namely higher insurance premiums and lower electricity bills.

Insurance & financial services inflation jumped to +5.5% YoY, led by higher health insurance.

The surge reflects Bank Negara Malaysia’s mandate for insurers to stagger medical premium hikes over 2024–2026, capped at 10% annually for most policyholders.

While this rule smooths the burden on households, consumer price index still records each tranche of repricing as a step-up when it occurs, explaining July’s jump.

Importantly, the overall impact remains limited given health insurance’s 1.3% weight.

In contrast, electricity costs fell 3.9% YoY, reflecting the restructuring of electricity tariffs.

The biannual Imbalance Cost Pass-through (ICPT) has been replaced with the new Automatic Fuel Adjustment (AFA) mechanism, which adopts monthly rate adjustment to better reflect commodity price fluctuations.

With coal and natural gas making up the bulk of generation costs, the recent decline in both fuels has translated into lower tariffs.

The government has indicated that around 85% of TNB customers would benefit from lower bills beginning July.

The latest print shows little immediate inflationary pressure from the SST expansion in July. The muted outcome reflects exemptions on essential goods.

Nonetheless, we expect SST-related pass-through to gradually materialise in discretionary segments, with a contained contribution of around 15 basis points to the second half of 2025 (2H25) inflation.

Beyond SST, the RM1,700 minimum wage extension to all employers from August could raise costs pressures, particularly for micro firms with less than five workers previously exempted.

The larger risk lies in the rationalisation of RON95 fuel subsidies. While the roll-out has been delayed, with details expected by end-September, the government has indicated a phased implementation, which should moderate the near-term inflationary impact.

On the external front, the outlook remains mixed. The potential US product-specific tariffs, including on semiconductors, could push up final goods prices.

At the same time, softer global demand and potential trade diversion may exert disinflationary pressure. Brent crude has slipped 9.2% to USD67.8 per barrel, reflecting softer global demand.

We expect the lower crude oil price to keep imported inflation pressures in check in the near term.

We maintain our projection for inflation to average +2.3% YoY in 2H25 , bringing the full-year 2025 inflation to +1.9%.

The muted July print and delay in RON95 subsidy rationalisation tilt risks to the downside.

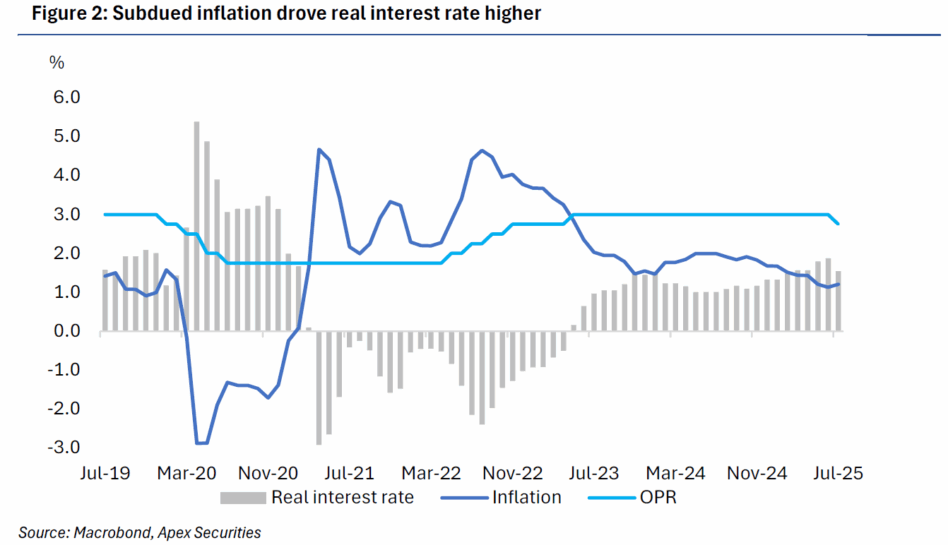

With inflation subdued and real interest rate (Jul: +1.5%) still above the pre-pandemic average (2015–2019: +1.2%), Bank Negara Malaysia has room to ease should growth falters.

Our base case is for the overnight policy rate to stay at 2.75% through 2025, though another pre-emptive 25 basis points cut cannot be ruled out. —Aug 25, 2025

Main image: currencytransfer.com